자동차용 V2X(Vehicle-to-Everything) 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)

Automotive Vehicle-to-Everything (V2X) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1959561

리서치사:Global Market Insights Inc.

발행일:2026년 02월

페이지 정보:영문 270 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

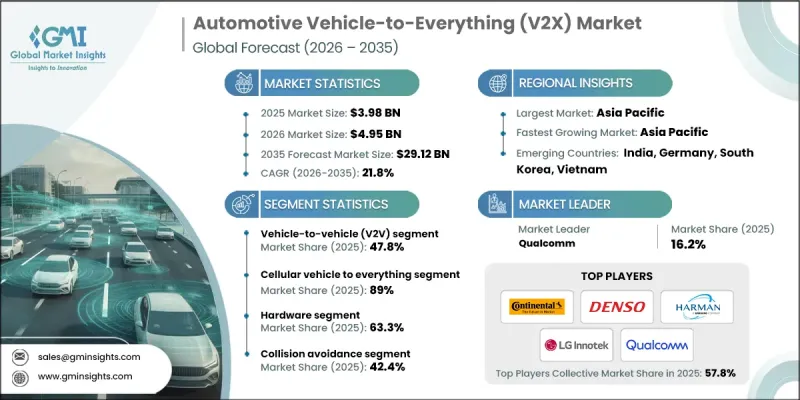

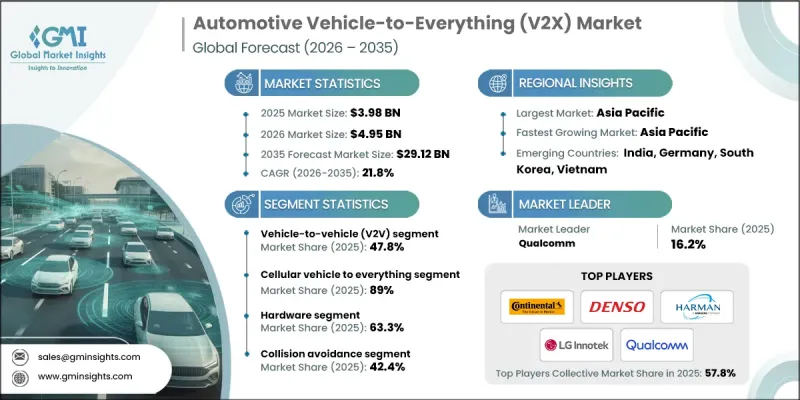

세계의 자동차용 V2X(Vehicle-to-Everything) 시장은 2025년에 39억 8,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR)21.8%로 성장하여 291억 2,000만 달러에 이를 것으로 예측됩니다.

도로 안전에 대한 관심이 높아지고 차량 자동화로의 전환이 가속화되면서 차량용 V2X 통신 기술의 채택이 크게 증가하고 있습니다. 세계 각국 정부는 교통 흐름 관리와 긴급 대응 효율을 높이기 위해 지능형 교통 인프라 및 디지털 요금 징수 시스템을 도입하고 있습니다. 주요 경제권의 공공 기관들은 전략적 모빌리티 회랑을 따라 지능형 교통 시스템 도입을 추진하고 있으며, 연결된 교차로에서 교통 체증이 현저하게 감소하는 것으로 입증되고 있습니다. 커넥티드카 및 전기자동차의 보급 확대는 V2X 생태계 전반을 더욱 강화시키고 있습니다. 초저지연 통신 표준의 발전으로 V2X 솔루션의 상업적 타당성이 향상되고 있습니다. 5세대 이동통신 시스템(5G)은 엔드투엔드 지연을 10밀리초 미만으로 줄여 충돌 회피, 차량 대열 주행, 혼합 교통 환경에서의 협력적 자율주행을 위한 실시간 의사결정을 가능하게 합니다. 동시에 커넥티드 차량이 시간당 25기가바이트 이상의 데이터를 생성함에 따라 사이버 보안과 데이터 거버넌스가 중요한 우선순위가 되고 있으며, 자동차 제조업체와 규제 당국은 공공 도로 네트워크에서 신뢰할 수 있는 통신을 보장하기 위해 강력한 신원 인증, 암호화 프로토콜, 보안 액세스 제어 시스템을 구현하고 있습니다. 보안 액세스 제어 시스템 구현을 추진하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

39억 8,000만 달러

예측 금액

291억 2,000만 달러

CAGR

21.8%

차량 간 통신(V2V) 부문은 2025년 47.8%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 20.8%의 성장률을 보일 것으로 전망됩니다. V2V 통신은 속도, 위치, 제동 동작에 대한 정보를 포함하여 차량 간의 직접적인 데이터 교환을 가능하게 합니다. 안전 당국은 커넥티드 안전 기술을 광범위하게 도입하면 여러 차량이 관련된 사고의 상당 부분을 예방할 수 있을 것으로 추정하고 있으며, 승용차 및 상용차 플랫폼 전반에 걸쳐 OEM의 광범위한 통합을 촉진하고 있습니다. 차량-인프라 간 통신(V2I)은 차량과 도로 시스템 간의 상호 작용을 가능하게 하고, 교통의 최적화와 협력적 모빌리티 관리를 지원함으로써 이 생태계를 더욱 강화합니다.

셀룰러 V2X 부문은 2025년 89%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 복합 성장률(CAGR) 22.7%로 성장할 것으로 전망됩니다. 셀룰러 V2X 아키텍처는 차량, 인프라, 네트워크 사업자, 클라우드 플랫폼을 연계하는 통합 통신 프레임워크를 제공합니다. 이 연결성은 지속적인 소프트웨어 업데이트, 원격 진단, 단계적 차량 자동화 기능을 지원합니다. 셀룰러 V2X는 차량, 보행자, 도로변 시스템, 백엔드 네트워크를 하나의 통신 생태계에 통합하여 개인 차량, 상용차, 대중교통 시스템 간의 상호 운용성을 강화하고 확장 가능한 배포를 가속화합니다.

중국 자동차 V2X(Vehicle-to-Everything) 시장은 63.8%의 점유율을 차지하며, 2025년에는 12억 달러 규모에 달할 것으로 예측됩니다. 강력한 국가 차원의 조정, 대규모 지능화 교통 이니셔티브, 통합된 스마트시티 전략으로 중국은 V2X 도입의 중요한 환경으로 자리매김하고 있습니다. 국내 완성차 업체들은 통신사 및 디지털 서비스 제공업체와 협력하여 프로토콜 표준화와 도시 및 고속도로 인프라를 가로지르는 전국적인 연결성 확대를 추진하고 있으며, 차량 플랫폼 전체에 V2X 기능을 탑재하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 유형별, 2022-2035

제6장 시장 추산 및 예측 : 기술별, 2022-2035

제7장 시장 추산 및 예측 : 컴포넌트별, 2022-2035

제8장 시장 추산 및 예측 : 용도별, 2022-2035

제9장 시장 추산 및 예측 : 전개 형태별, 2022-2035

제10장 시장 추산 및 예측 : 차량별, 2022-2035

제11장 시장 추산 및 예측 : 지역별, 2022-2035

제12장 기업 개요

LSH

영문 목차

영문목차

The Global Automotive Vehicle-to-Everything (V2X) Market was valued at USD 3.98 billion in 2025 and is estimated to grow at a CAGR of 21.8% to reach USD 29.12 billion by 2035.

Rising concerns surrounding road safety and the accelerating shift toward vehicle automation are significantly driving the adoption of automotive V2X communication technologies. Governments worldwide are implementing intelligent transportation infrastructure and digital tolling frameworks to enhance traffic flow management and emergency response efficiency. Public authorities across major economies are promoting cooperative intelligent transport deployments along strategic mobility corridors, demonstrating measurable reductions in congestion at connected intersections. The growing penetration of connected and electric vehicles is further strengthening the overall V2X ecosystem. Advancements in ultra-low latency communication standards are improving the commercial viability of V2X solutions, with fifth-generation cellular networks capable of delivering end-to-end latency below 10 milliseconds to enable real-time decision-making for collision avoidance, vehicle platooning, and coordinated autonomous driving in mixed traffic environments. At the same time, cybersecurity and data governance have become critical priorities as connected vehicles generate more than 25 gigabytes of data per hour, prompting OEMs and regulators to implement robust identity authentication, encryption protocols, and secure access control systems to ensure trusted communication across public road networks.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$3.98 Billion

Forecast Value

$29.12 Billion

CAGR

21.8%

The vehicle-to-vehicle segment accounted for 47.8% share in 2025 and is expected to grow at a CAGR of 20.8% from 2026 to 2035. V2V communication enables direct data exchange between vehicles, including information related to speed, position, and braking behavior. Safety authorities estimate that a substantial share of multi-vehicle accidents could be prevented through widespread deployment of connected safety technologies, encouraging broader OEM integration across passenger and commercial vehicle platforms. Vehicle-to-infrastructure communication further enhances this ecosystem by enabling interaction between vehicles and roadway systems, supporting traffic optimization and coordinated mobility management.

The cellular vehicle-to-everything segment held 89% share in 2025 and is forecast to grow at a CAGR of 22.7% through 2035. Cellular V2X architecture delivers an integrated communication framework linking vehicles, infrastructure, network operators, and cloud platforms. This connectivity supports continuous software updates, remote diagnostics, and progressive vehicle automation capabilities. By unifying vehicles, pedestrians, roadside systems, and backend networks within a single communication ecosystem, cellular V2X enhances interoperability across private vehicles, commercial fleets, and public transportation systems, accelerating scalable deployment.

China Automotive Vehicle-to-Everything (V2X) Market held 63.8% share, generating USD 1.2 billion in 2025. Strong national coordination, large-scale intelligent transportation initiatives, and integrated smart city strategies have positioned China as a key environment for V2X deployment. Domestic automakers are embedding V2X functionality across vehicle platforms while collaborating with telecom operators and digital service providers to standardize protocols and expand nationwide connectivity across urban and highway infrastructure.

Key companies operating in the Global Automotive Vehicle-to-Everything (V2X) Market include Qualcomm, NXP, Continental, Bosch, Denso, Harman, Nokia, LG Innotek, and AT&T. Companies in the automotive vehicle-to-everything market are strengthening their competitive position through strategic telecom partnerships, advanced chipset development, and software-driven innovation. Leading players are investing heavily in 5G and next-generation connectivity solutions to enhance latency performance and scalability. Collaboration with automotive OEMs enables early integration of V2X modules into new vehicle platforms. Firms are also prioritizing cybersecurity frameworks, secure credential management systems, and over-the-air update capabilities to meet evolving regulatory standards.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality Commitments

1.2.1 GMI AI policy & data integrity commitment

1.2.1.1 Source consistency protocol

1.3 Research Trail & Confidence Scoring

1.3.1 Research Trail Components

1.3.2 Scoring Components

1.4 Data Collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.5.1.1 Sources, by region

1.6 Base estimates and calculations

1.6.1 Base year calculation for any one approach

1.7 Forecast model

1.7.1 Quantified market impact analysis

1.7.1.1 Mathematical impact of growth parameters on forecast

1.8 Research transparency addendum

1.8.1 Source attribution framework

1.8.2 Quality assurance metrics

1.8.3 Our commitment to trust

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Technology

2.2.4 Component

2.2.5 Application

2.2.6 Deployment

2.2.7 Vehicle

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising road safety regulations

3.2.1.2 Growth of connected and autonomous vehicles

3.2.1.3 Expansion of smart city programs

3.2.1.4 Deployment of fifth generation networks

3.2.2 Industry pitfalls and challenges

3.2.2.1 High infrastructure deployment cost

3.2.2.2 Interoperability and standardization issues

3.2.3 Market opportunities

3.2.3.1 Integration with autonomous driving systems

3.2.3.2 Expansion of vehicle to infrastructure projects

3.2.3.3 Growth in electric and connected vehicle fleets

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 United States connected vehicle and intelligent transportation regulations

3.4.1.2 Federal communications and spectrum allocation guidelines

3.4.1.3 Vehicle safety and connected mobility standards

3.4.1.4 Canada cooperative intelligent transport system regulations

3.4.2 Europe

3.4.2.1 European Union cooperative intelligent transport system framework

3.4.2.2 ETSI and CEN communication standards for V2X

3.4.2.3 Country level connected vehicle compliance requirements

3.4.2.4 Data protection and cybersecurity rules for connected mobility

3.4.3 Asia Pacific

3.4.3.1 China intelligent connected vehicle regulations

3.4.3.2 India connected transport and automotive communication standards

3.4.3.3 Japan cooperative driving and vehicle communication guidelines

3.4.3.4 South Korea smart mobility and V2X compliance

3.4.3.5 ASEAN regional connected transport frameworks

3.4.4 Latin America

3.4.4.1 Brazil intelligent transport and connected vehicle regulations

3.4.4.2 Argentina automotive communication compliance

3.4.4.3 Mexico connected mobility and transport digitization policies