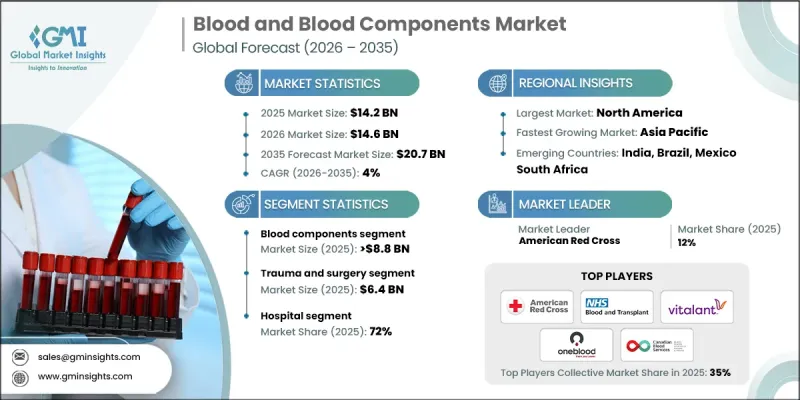

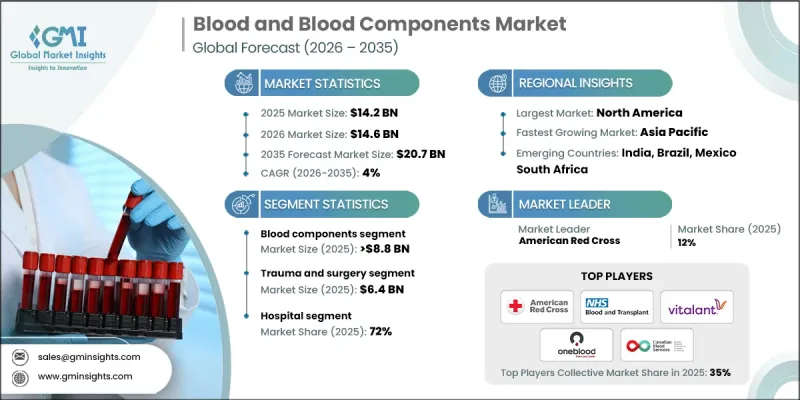

세계의 혈액 및 혈액 성분 시장은 2025년에 142억 달러로 평가되었으며, 2035년까지 CAGR 4%로 성장하여 207억 달러에 달할 것으로 예측됩니다.

전 세계 수술 건수 증가, 장기 질환의 유병률 증가, 광범위한 임상 치료에서 혈장 기반 요법의 사용 확대 등으로 인해 혈장 기반 치료제 시장은 꾸준히 성장하고 있습니다. 채혈기관의 지속적인 인식개선 활동과 헌혈 캠페인이 안정적인 혈액 수급을 뒷받침하고 있습니다. 수혈 요법에 필요한 적혈구, 혈장, 혈소판 등 혈액 및 혈액 성분은 수혈 요법에 필요한 혈액에 대한 중단 없는 접근을 보장한다는 점에서 현대 의료 시스템에서 없어서는 안 될 필수적인 존재입니다. 이 제품들은 응급 의료, 외과적 개입, 종양 치료, 혈액 관련 질환의 장기 관리 등 다양한 분야에서 널리 사용되고 있습니다. 시장은 제품의 무결성과 환자의 안전을 유지하기 위해 엄격한 품질 및 안전 기준 하에 운영되고 있습니다. 채혈 방법, 성분 분리, 검사, 보관, 물류에 대한 지속적인 기술 혁신을 통해 효율성을 높이고, 전 세계 의료 시스템의 수요 증가에 대응하고 있습니다. 업계는 신뢰성, 추적성, 규제 준수에 중점을 두고 계속 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 142억 달러 |

| 예측 금액 | 207억 달러 |

| CAGR | 4% |

혈액 성분 부문은 2025년 88억 달러의 수익을 창출했습니다. 이 부문에는 적혈구, 혈장, 혈소판, 백혈구가 포함되며, 각각 전문적인 치료 역할을 수행합니다. 적혈구는 헤모글로빈 수치가 저하된 환자의 산소 공급 회복에 필수적인 기능을 가지고 있어 높은 수요가 지속되고 있습니다. 전 세계적으로 혈액 관련 질환에 대한 부담은 성분 기반 치료제의 지속적인 사용을 뒷받침하고 있으며, 이 부문을 핵심 수익원으로 삼고 있습니다.

병원 부문은 2025년 72%의 점유율을 차지했습니다. 의료 시설은 응급 의료, 외과 수술, 종양학 서비스, 만성질환 치료 관리에서 중심적인 역할을 수행하기 때문에 혈액 및 혈액 성분의 주요 소비처로 남아 있습니다. 복잡한 의료 개입의 증가, 외상 사례의 증가, 고급 치료 프로토콜의 보급과 함께 병원의 안정적인 수요를 지속적으로 창출하여 최종사용자로서의 우위를 강화하고 있습니다.

북미 혈액 및 혈액 성분 시장은 2025년 39.8%의 점유율을 차지했습니다. 이 지역은 잘 구축된 의료 인프라, 높은 헌혈 참여율, 그리고 다양한 임상 응용 분야에서 수혈 요법의 적극적인 활용이라는 장점을 가지고 있습니다. 선진적인 의료 관행, 효율적인 혈액 관리 시스템, 탄탄한 제도적 기반이 지역 시장에서의 선도적 지위를 유지하고 있습니다.

The Global Blood and Blood Components Market was valued at USD 14.2 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 20.7 billion by 2035.

The market is experiencing steady growth due to the rising number of surgical procedures worldwide, the increasing prevalence of long-term medical conditions, and the expanding use of plasma-based therapies across a wide range of clinical treatments. Continuous awareness initiatives and donation drives conducted by blood collection organizations are supporting a stable supply pipeline. Blood and blood components remain essential to modern healthcare systems, as they ensure uninterrupted access to red blood cells, plasma, and platelets required for transfusion-based therapies. These products are widely used across emergency care, surgical interventions, oncology treatments, and the long-term management of blood-related disorders. The market operates under strict quality and safety frameworks to maintain product integrity and patient safety. Ongoing innovation in blood collection methods, component separation, testing, storage, and logistics is improving efficiency and meeting the rising demands of global healthcare systems. The industry continues to evolve with a strong focus on reliability, traceability, and regulatory compliance.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.2 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 4% |

The blood components segment generated USD 8.8 billion in 2025. This segment includes red blood cells, plasma, platelets, and white blood cells, each fulfilling specialized therapeutic roles. Red blood cells remain in high demand due to their essential function in restoring oxygen delivery in patients with reduced hemoglobin levels. The global burden of blood-related conditions continues to support sustained utilization of component-based therapies, making this segment a core revenue contributor.

The hospitals segment accounted for 72% share in 2025. Healthcare facilities remain the primary consumers of blood and blood components due to their central role in managing emergency care, surgical procedures, oncology services, and chronic disease treatment. The growing volume of complex medical interventions, combined with increasing trauma cases and advanced treatment protocols, continues to drive consistent demand from hospitals, reinforcing their dominance as end users.

North America Blood and Blood Components Market held a 39.8% share in 2025. The region benefits from a well-established healthcare infrastructure, strong donor participation, and high utilization of transfusion therapies across multiple clinical applications. Advanced medical practices, efficient blood management systems, and strong institutional frameworks continue to support regional market leadership.

Key organizations operating in the Global Blood and Blood Components Market include Vitalant, Canada Blood Services, American Red Cross, OneBlood, NHS Blood and Transplant, ImpactLife, America's Blood Centers, Versiti, Bloodworks Northwest, Carter BloodCare, Indian Red Cross Society, Associazione Volontari Italiani del Sangue, Northern Ireland Blood Transfusion Service, Scottish National Blood Transfusion Service, and the Welsh Blood Service. Companies in the blood and blood components market are strengthening their market position by expanding donor networks, improving collection efficiency, and investing in advanced processing and storage technologies. Organizations are focusing on digital donor engagement platforms to improve donor retention and streamline appointment scheduling. Strategic collaborations with hospitals and healthcare systems are enhancing supply reliability and demand forecasting.