Acrylate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936618

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

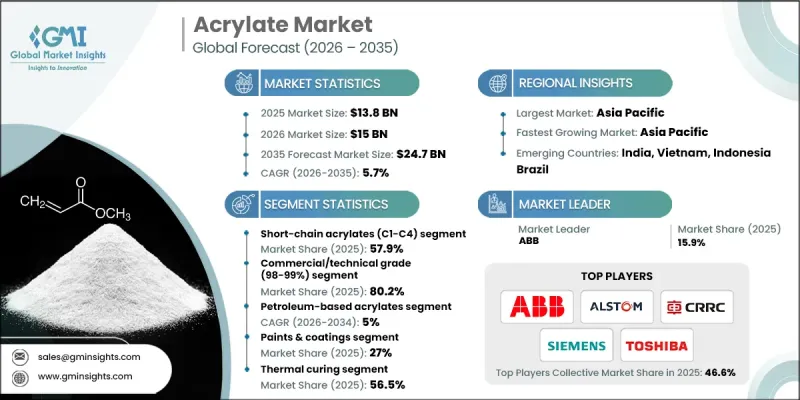

세계의 아크릴레이트 시장은 2025년에 138억 달러로 평가되었으며, 2035년까지 CAGR 5.7%로 성장하여 247억 달러에 달할 것으로 예측됩니다.

아크릴레이트는 제한된 용도의 화학제품 카테고리에서 현대의 다양한 산업 공정을 뒷받침하는 기초 소재로 진화해 왔습니다. 다용도성, 내구성, 성능 특성으로 인해 여러 제조 생태계에서 필수적인 존재가 되었습니다. 최근 생산업체들은 강화되는 환경 규제 및 규제 요건에 대응하면서 효율성을 향상시킬 수 있는 차세대 배합 개발에 집중하고 있습니다. 제조 방법의 지속적인 개선을 통해 제조업체는 성능 최적화와 지속가능성 목표를 동시에 달성하여 아크릴레이트를 첨단 재료 과학의 중요한 구성요소로 자리매김하고 있습니다. 시장은 혁신 중심의 제품 차별화와 친환경 제조 방식에 대한 관심이 높아지면서 다양한 산업 밸류체인에서 안정적인 수요의 혜택을 누리고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035

개시 금액

138억 달러

예측 금액

247억 달러

CAGR

5.7%

지속가능성은 아크릴 산업에 영향을 미치는 결정적인 힘이 되었습니다. 배출량 제한을 위한 규제 압력으로 인해 친환경 배합으로의 전환이 가속화되고 있습니다. 각 제조사들은 기계적 강도, 내구성, 장기적인 성능을 유지하면서 규제 기준을 충족하는 솔루션을 개발하기 위해 적극적인 연구개발 투자를 하고 있습니다. 이러한 혁신은 보다 광범위한 세계 탈탄소화 목표에 기여하고, 지속가능한 산업 혁신에 있어 아크릴레이트의 역할을 강화하는 데 기여하고 있습니다. 환경 컴플라이언스가 경쟁 차별화 요소로 떠오르면서, 친환경 아크릴 솔루션의 채택은 전 세계 시장 전반에 걸쳐 지속적으로 증가하고 있습니다.

순도 98-99%의 상업용 및 기술 등급 아크릴레이트는 2025년 80.2%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 4.8%의 성장률을 기록할 것으로 전망됩니다. 이 등급은 비용 효율성, 적응성, 균형 잡힌 성능 특성으로 인해 여전히 널리 선호되고 있습니다. 다양한 용도로 사용되며, 여러 최종 사용 부문에서 대량 소비를 지원합니다. 한편, 고순도 등급은 우수한 균일성, 신뢰성, 기능적 성능이 요구되는 용도에 지속적으로 활용되어 전문 산업 분야의 안정적인 수요를 뒷받침하고 있습니다.

열경화 부문은 2025년 56.5%의 점유율을 차지했으며, 2035년까지 연평균 4.7%의 성장률을 보일 것으로 예상됩니다. 이 경화 방법은 접착 강도와 장기 내구성을 향상시키는 능력으로 인해 산업 규모의 운영에서 여전히 선호되는 선택입니다. 제조업체들이 더 빠른 처리시간과 에너지 효율 향상을 추구하면서 대체 경화 기술이 주목받고 있습니다. 성능 정밀도와 내화학성이 필수적인 전문 산업 분야에서도 고급 경화 방법은 점점 더 중요해지고 있습니다.

북미 아크릴레이트 시장은 2025년 19.6%의 점유율을 차지할 것으로 예상되며, 이는 성숙하고 전략적으로 중요한 지역으로서의 지위를 반영합니다. 이 시장은 첨단 제조 인프라, 안정적인 산업 수요, 지속가능한 재료 사용을 촉진하는 강력한 규제 프레임워크에 의해 뒷받침되고 있습니다. 지속적인 기술 혁신과 환경 기준 준수가 이 지역의 성장을 지속시키고, 세계 경쟁 환경에서 북미의 우위를 계속 강화해 나가고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추정 및 예측 : 제품 유형별, 2022-2035

제6장 시장 추정 및 예측 : 등급별, 2022-2035

제7장 시장 추정 및 예측 : 원료별, 2022-2035

제8장 시장 추정 및 예측 : 용도별, 2022-2035

제9장 시장 추정 및 예측 : 경화 기술별, 2022-2035

제10장 시장 추정 및 예측 : 유통 채널별, 2022-2035

제11장 시장 추정 및 예측 : 지역별, 2022-2035

제12장 기업 개요

KSM

영문 목차

영문목차

The Global Acrylate Market was valued at USD 13.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 24.7 billion by 2035.

Acrylates have evolved from a narrowly used chemical category into a foundational material supporting a wide range of modern industrial processes. Their versatility, durability, and performance characteristics make them indispensable across multiple manufacturing ecosystems. Over time, producers have shifted their focus toward developing next-generation formulations that deliver enhanced efficiency while aligning with tightening environmental and regulatory expectations. Continuous improvements in production methods have allowed manufacturers to balance performance optimization with sustainability goals, positioning acrylates as a critical component in advanced material science. The market continues to benefit from consistent demand across diverse industrial value chains, supported by innovation-driven product differentiation and increasing emphasis on environmentally responsible manufacturing practices.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$13.8 Billion

Forecast Value

$24.7 Billion

CAGR

5.7%

Sustainability has become a defining force influencing the acrylate industry. Regulatory pressure aimed at limiting emissions has accelerated the transition toward environmentally compatible formulations. Manufacturers are actively investing in research to develop solutions that meet regulatory thresholds while maintaining mechanical strength, durability, and long-term performance. These innovations contribute to broader global decarbonization objectives and reinforce the role of acrylates in sustainable industrial transformation. As environmental compliance becomes a competitive differentiator, the adoption of greener acrylate solutions continues to gain momentum across global markets.

The commercial and technical grade acrylates with purity levels of 98-99% accounted for 80.2% share in 2025 and are forecast to grow at a CAGR of 4.8% from 2026 to 2035. These grades remain widely preferred due to their cost efficiency, adaptability, and balanced performance characteristics. Their broad usability supports high-volume consumption across multiple end-use segments. In contrast, higher-purity variants continue to serve applications requiring superior consistency, reliability, and functional performance, supporting steady demand from specialized industrial segments.

The thermal curing segment held 56.5% share in 2025 and is expected to grow at a CAGR of 4.7% through 2035. This curing method remains a preferred option for industrial-scale operations due to its ability to enhance bonding strength and long-term durability. Alternative curing technologies are gaining traction as manufacturers seek faster processing times and improved energy efficiency. Advanced curing methods are also finding increasing relevance in specialized industrial applications where performance precision and chemical resistance are essential.

North America Acrylate Market accounted for a 19.6% share in 2025, reflecting its status as a mature and strategically significant region. The market is supported by advanced manufacturing infrastructure, stable industrial demand, and strong regulatory frameworks promoting sustainable material use. Ongoing innovation and compliance with environmental standards continue to sustain regional growth and reinforce North America's competitive position in the global landscape.

Key companies operating in the Global Acrylate Market include Arkema Group, BASF SE, LG Chem Ltd, The Dow Chemical Company, Formosa Plastics Corporation, Nippon Shokubai Co Ltd, Sasol Limited, Allnex Group, Sartomer, Toagosei Co Ltd, Jiangsu Jurong Chemical Co Ltd, and Osaka Organic Chemical Industry Ltd. These players maintain strong market positions through continuous innovation, capacity expansion, and diversified product portfolios To strengthen their foothold, acrylate manufacturers are prioritizing strategic investments in research and development to create high-performance and environmentally compliant formulations. Many companies are expanding production capacities and optimizing supply chains to ensure cost efficiency and consistent product availability. Strategic partnerships, acquisitions, and collaborations are commonly used to enhance technological capabilities and expand geographic reach. Firms are also focusing on portfolio diversification to address evolving customer requirements while improving sustainability credentials.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product type

2.2.3 Grade

2.2.4 Feedstock

2.2.5 Application

2.2.6 Curing technology

2.2.7 Distribution channel

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing demand from paints & coatings industry

3.2.1.2 Expanding superabsorbent polymer applications in hygiene products

3.2.1.3 Rising adoption in adhesives & sealants

3.2.2 Industry pitfalls and challenges

3.2.2.1 Volatility in raw material (propylene) prices

3.2.2.2 Stringent environmental regulations

3.2.3 Market opportunities

3.2.3.1 Bio-based acrylates development & commercialization

3.2.3.2 Growth in electric vehicle battery binders

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By Product type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Short-Chain Acrylates (C1-C4)

5.2.1 Methyl Acrylate (MA)

5.2.2 Ethyl Acrylate (EA)

5.2.3 Butyl Acrylate (BA)

5.2.4 iso-Butyl Acrylate (iBA)

5.3 Medium-Chain Acrylates (C6-C10)

5.3.1 2-Ethylhexyl Acrylate (2-EHA)

5.3.2 2-Octyl Acrylate

5.3.3 iso-Decyl Acrylate (iDA)

5.4 Long-Chain Acrylates (C12-C22)

5.4.1 Lauryl Acrylate (C12)

5.4.2 Stearyl Acrylate (C18)

5.4.3 Behenyl Acrylate (C22)

Chapter 6 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Commercial/technical grade (98-99%)

6.3 High purity grade (>99%)

6.4 Ultra-pure grade (>99.5%)

Chapter 7 Market Estimates and Forecast, By Feedstock, 2022-2035 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Petroleum-based acrylates

7.3 Bio-based acrylates

7.4 Glycerol-derived (acrolein route)

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

8.1 Key trends

8.2 Adhesives & sealants

8.2.1 Pressure-sensitive adhesives (PSA)

8.2.2 Hot melt adhesives

8.2.3 Structural adhesives

8.2.4 Water-based adhesives

8.2.5 Sealants

8.3 Paints & coatings

8.3.1 Architectural coatings

8.3.2 Industrial coatings

8.3.3 Automotive coatings

8.3.4 Wood coatings

8.3.5 Coil coatings

8.3.6 Marine coatings

8.3.7 Signage coatings

8.3.8 Specialty coatings

8.4 Superabsorbent polymers (sap)

8.5 Textiles & nonwovens

8.5.1 Textile finishing

8.5.2 Performance textiles

8.5.3 Nonwoven binders

8.5.4 Carpet backing

8.6 Plastics & polymers

8.6.1 Impact modifiers

8.6.2 Processing aids

8.6.3 Acrylic sheets (PMMA)

8.6.4 Acrylic resins

8.7 Paper & paperboard

8.8 Personal care & cosmetics

8.8.1 Hair care

8.8.2 Skin care

8.8.3 Color cosmetics

8.9 Construction materials

8.9.1 Concrete additives

8.9.2 Caulks & sealants

8.9.3 Waterproofing membranes

8.9.4 Tile adhesives

8.9.5 Grouts & mortars

8.10 Electronics & electrical

8.10.1 Li-ion battery cathode binders

8.10.2 Semiconductor coatings

8.10.3 Display technologies

8.10.4 Connector assembly adhesives

8.10.5 Encapsulation materials

8.11 Medical & healthcare

8.11.1 Medical device coatings

8.11.2 Dental materials

8.11.3 Wound care adhesives

8.11.4 Drug delivery systems

8.12 Others

Chapter 9 Market Estimates and Forecast, By Curing Technology, 2022-2035 (USD Billion) (Kilo Tons)

9.1 Key trends

9.2 Thermal curing

9.3 Uv curing

9.4 Electron-beam (EB) curing

9.5 Moisture curing

9.6 Ambient/room temperature curing

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

10.1 Key trends

10.2 Direct Sales

10.3 Distributors & Resellers

10.4 Online Platforms

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)