세계의 디비닐 벤젠 시장은 2025년에 7,710만 달러로 평가되었으며, 2035년까지 CAGR 5.9%로 성장하여 1억 3,700만 달러에 달할 것으로 예측됩니다.

시장 확대는 특히 이온교환수지 및 크로마토그래피 수지 응용 분야에서 고성능 가교 폴리머 시스템에 대한 수요 증가에 의해 뒷받침되고 있습니다. 도시 물 인프라에 대한 지속적인 투자와 수질 및 배수 규제 강화로 인해 내구성과 화학적 안정성이 뛰어난 수지 소재에 대한 수요가 증가하고 있습니다. 이러한 추세는 아시아, 유럽, 북미 등 주요 지역에서 디비닐벤젠에 대한 수요를 강화하고 있습니다. 2022년 이후 구조적 무결성 개선이 요구되는 엔지니어링 플라스틱, 특수수지, 코팅, 접착제 등 첨단 제조 분야에서도 소비가 증가하고 있습니다. 지역별 생산능력 확대, 특히 아시아 지역에서의 증가는 DVB계 수지의 유럽 및 미국 시장으로의 수출 확대를 뒷받침하고 있습니다. 최종사용자는 수지의 성능, 내구성, 내화학성 향상을 위해 저함량 등급에서 DVB 63, DVB 80과 같은 고함량 등급으로, 점차 고디비닐벤젠 농도의 제품으로 전환하고 있습니다. 이러한 추세는 정제 및 분리 응용 분야에서 높은 가교 밀도 요구 사항을 충족시키기 위해 제품 포트폴리오를 조정하는 수지 제조업체들에 의해 더욱 강화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 7,710만 달러 |

| 예측 금액 | 1억 3,700만 달러 |

| CAGR | 5.9% |

이온교환수지 부문은 2025년 45.43%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 5.4%로 성장할 것으로 예측됩니다. 수요 증가는 환경 규제 강화, 산업 처리 능력 확대, 고순도 분리 시스템 사용 증가에 의해 주도되고 있습니다. DVB 가교 수지는 긴 수명, 구조적 안정성, 규제된 운전 조건에서 안정적인 성능으로 인해 수요가 증가하고 있습니다. 이 부문은 단기적인 경기변동보다는 규제 대응에 따른 안정적 수요의 수혜를 받고 있습니다.

미국 디비닐벤젠 시장은 특수 화학 및 수지 제조의 견고한 기반과 지자체 및 산업 인프라의 지속적인 업데이트에 힘입어 2025년 1,460만 달러 규모에 달할 것으로 예상됩니다. 정화 및 처리 시스템에 대한 지속적인 투자가 국내 디비닐벤젠 소비량의 지속적인 성장에 기여하고 있습니다.

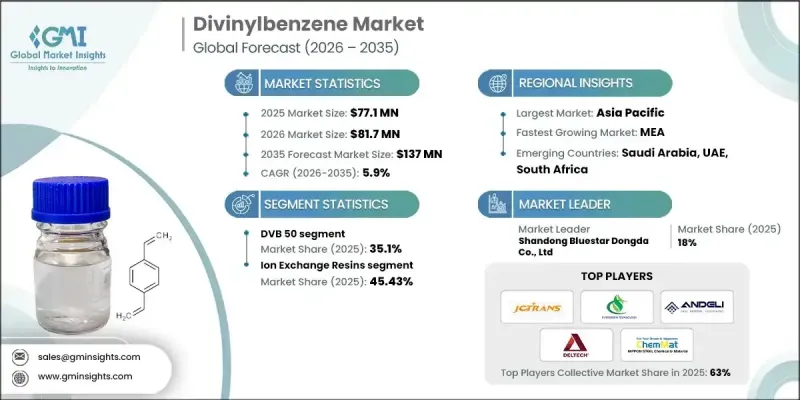

The Global Divinylbenzene Market was valued at USD 77.1 million in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 137 million by 2035.

Market expansion is supported by rising demand for high-performance crosslinked polymer systems, particularly within ion-exchange and chromatographic resin applications. Ongoing investments in urban water infrastructure, combined with tighter water quality and discharge regulations, are increasing the need for durable and chemically stable resin materials. This trend is strengthening demand for divinylbenzene across key regions, including Asia, Europe, and North America. Since 2022, consumption has also increased across advanced manufacturing sectors where engineered plastics, specialty resins, coatings, and adhesives require enhanced structural integrity. Growth in regional production capacity, especially in Asia, has supported rising exports of DVB-based resins to Western markets. End users are increasingly shifting toward higher divinylbenzene concentrations, moving from lower-content grades to DVB 63 and DVB 80, to achieve improved resin performance, durability, and chemical resistance. This shift is being reinforced by resin manufacturers that are aligning product portfolios with higher crosslink density requirements across purification and separation applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $77.1 Million |

| Forecast Value | $137 Million |

| CAGR | 5.9% |

The ion-exchange resins segment accounted for 45.43% share in 2025 and is expected to grow at a CAGR of 5.4% from 2026 to 2035. Demand growth is being driven by stricter environmental compliance requirements, expansion of industrial processing capacity, and increasing use of high-purity separation systems. DVB-crosslinked resins are gaining preference due to their long service life, structural stability, and consistent performance under regulated operating conditions. This segment benefits from steady, compliance-driven demand rather than short-term cyclical fluctuations.

U.S. Divinylbenzene Market reached USD 14.6 million in 2025, supported by a strong base of specialty chemical and resin manufacturing and continued upgrades in municipal and industrial infrastructure. Sustained investment in purification and processing systems is contributing to consistent growth in domestic divinylbenzene consumption.

Key companies operating in the Global Divinylbenzene Market include Dupont, Nippon Steel Chemical & Material Co., Ltd., Shandong Bluestar Dongda Co., Ltd, Jiangsu Evergreen New Material Technology Co., Ltd, Deltech Corporation LLC, Jiangsu Andeli New Material Technology Co., Ltd., Jiangsu Danhua, Sigma Aldrich, TCI Chemicals, Alfa Aesar, ABCR GmbH, Clearsynth, Angene International Limited, Alfa Chemistry, and AA Blocks. Companies in the Global Divinylbenzene Market are strengthening their market position by expanding production capacity and upgrading manufacturing processes to support higher-purity and higher-DVB-content grades. Manufacturers are investing in formulation optimization to improve crosslink efficiency, durability, and end-use performance. Strategic partnerships with resin producers and downstream processors are helping secure long-term supply agreements and stable demand. Firms are also focusing on regional expansion to support export growth and reduce logistics dependency. Continuous investment in research and quality control is enabling suppliers to meet evolving regulatory standards while maintaining consistent product performance, supporting sustained competitiveness in global specialty chemical markets.