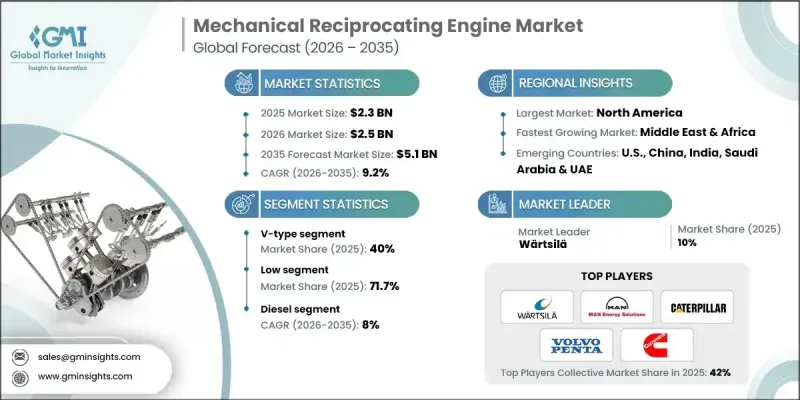

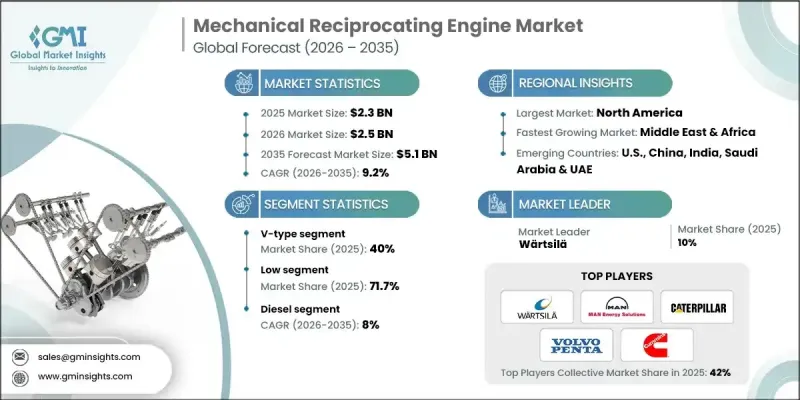

세계의 기계식 왕복 엔진 시장은 2025년에 23억 달러로 평가되었으며, 2035년까지 CAGR 9.2%로 성장하여 51억 달러에 달할 것으로 예측됩니다.

시장 확대는 산업 인프라의 지속적인 발전과 정부 기관 및 민간 부문 참여자 모두의 자본 투자 증가에 의해 뒷받침되고 있습니다. 이러한 투자는 생산능력 확대, 시설 현대화, 산업 다각화에 기여하고 있으며, 이러한 투자가 결합되어 여러 최종 사용 분야에 걸쳐 지속적인 수요를 창출하고 있습니다. 기계식 왕복 엔진은 입증된 신뢰성과 적응성으로 인해 전 세계 동력 및 운동 시스템에서 중요한 역할을 하고 있습니다. 이 엔진은 실린더 내 피스톤의 직선 운동을 연속적인 작동 사이클을 통해 회전 운동으로 변환하여 광범위한 작동 조건에서 안정적인 동력을 공급합니다. 농촌 전기화에 대한 관심 증가, 지원적인 규제 프레임워크, 백업 및 비상 전원 공급 장치의 필요성에 대한 인식이 높아지면서 시장 성장을 촉진하고 있습니다. 정부 주도의 전력 접근성 정책은 수요를 더욱 강화하고 있습니다. 성숙한 기술임에도 불구하고, 이 분야는 연속 운전 환경과 간헐적 운전 환경 모두에서 신뢰할 수 있는 기계 동력에 대한 요구가 높아짐에 따라 효율 개선과 배출가스 최적화를 통해 계속 진화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035 |

| 개시 금액 | 23억 달러 |

| 예측 금액 | 51억 달러 |

| CAGR | 9.2% |

직렬 엔진 구성 부문은 2035년까지 14억 달러에 달할 것으로 예상됩니다. 이 부문의 성장은 간단한 구조적 레이아웃, 신뢰할 수 있는 성능 및 유지보수의 용이성에 기인합니다. 직렬 실린더 배열의 엔진은 안정적인 출력, 높은 작동 효율, 긴 수명을 제공하므로 비용 관리, 내구성 및 유지보수 편의성이 필수적인 용도에 이상적입니다. 다양한 산업 및 모빌리티 관련 애플리케이션에 폭넓게 적용할 수 있다는 점이 안정적인 수요를 뒷받침하고 있습니다.

저속 기계식 왕복 엔진 부문은 2025년 71.7%의 점유율을 차지하며 2035년까지 35억 달러에 달할 것으로 예상됩니다. 이 부문은 장기간 안정적인 성능이 요구되는 고부하 발전 및 추진 시스템에 대한 의존도가 증가함에 따라 수혜를 받고 있습니다. 이 엔진은 연료 효율성, 기계적 견고성, 가혹한 부하 조건에서의 연속 운전 능력으로 높은 평가를 받고 있으며, 에너지 집약적인 산업 응용 분야에서 우선적으로 선택되고 있습니다.

미국 기계식 왕복 엔진 시장은 2025년 8억 2,620만 달러 규모로 74%의 점유율을 차지할 것으로 예상됩니다. 이 나라 시장의 강점은 발전, 선박 운항, 산업 장비 분야에서 신뢰성과 효율성이 높은 엔진에 대한 지속적인 수요에 힘입은 바 큽니다. 엔진 기술의 지속적인 발전, 규제 요건 준수, 배기가스 성능에 대한 관심 증가로 도입이 촉진되고 장기적인 시장 안정성이 강화되고 있습니다.

The Global Mechanical Reciprocating Engine Market was valued at USD 2.3 billion in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 5.1 billion by 2035.

Market expansion is supported by the continued development of industrial infrastructure and rising capital investment from both government bodies and private sector participants. These investments are contributing to capacity expansion, facility modernization, and broader industrial diversification, which together are creating sustained demand across multiple end-use sectors. Mechanical reciprocating engines continue to play a critical role within global power and motion systems due to their proven reliability and adaptability. These engines operate by converting linear piston movement within cylinders into rotational mechanical output through sequential operating cycles, delivering dependable power across a wide range of operating conditions. Increasing focus on rural electrification, supportive regulatory frameworks, and heightened awareness of backup and emergency power requirements are reinforcing market growth. Government-led power access initiatives are further strengthening demand. Despite being a mature technology, the segment continues to evolve through efficiency improvements and emissions optimization, driven by rising requirements for dependable mechanical power in both continuous and intermittent operating environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.3 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 9.2% |

The inline engine configuration segment is projected to reach USD 1.4 billion by 2035. Growth in this segment is attributed to its simple structural layout, dependable performance, and ease of servicing. Engines with a linear cylinder arrangement provide stable output, operational efficiency, and long service life, making them well-suited for applications where cost control, durability, and maintenance simplicity are essential. Their broad applicability across multiple industrial and mobility-related uses continues to support steady demand.

The low-speed mechanical reciprocating engines segment accounted for 71.7% share in 2025 and is expected to reach USD 3.5 billion by 2035. This segment is benefiting from increasing reliance on heavy-duty power generation and propulsion systems that require consistent performance over extended operating periods. These engines are favored for their fuel efficiency, mechanical robustness, and ability to operate continuously under demanding load conditions, making them a preferred choice for energy-intensive industrial applications.

United States Mechanical Reciprocating Engine Market held 74% share, generating USD 826.2 million in 2025. Market strength in the country is driven by sustained demand for reliable and efficient engines across power generation, marine operations, and industrial equipment usage. Continued advancements in engine technology, adherence to regulatory requirements, and an increased focus on emissions performance are supporting adoption and reinforcing long-term market stability.

Key companies operating in the Global Mechanical Reciprocating Engine Market include Caterpillar, Cummins, Wartsila, MAN Energy Solutions, Mitsubishi Heavy Industries, Rolls-Royce, Siemens Energy, Kawasaki Heavy Industries, AB Volvo Penta, KUBOTA Corporation, Perkins Engines Company, Deutz AG, Fairbanks Morse Defense, GE Vernova, Doosan Corporation, Motorenfabrik Hatz, Escorts Kubota, JC Bamford Excavators, Lister Petter, and Rehlko. Companies active in the mechanical reciprocating engine market are strengthening their competitive position through technology enhancement, portfolio diversification, and strategic geographic expansion. Leading manufacturers are investing in improved fuel efficiency, emissions reduction technologies, and advanced control systems to meet evolving regulatory and customer requirements. Many players are expanding service networks and aftermarket support to improve lifecycle value and customer retention. Strategic partnerships with industrial operators and infrastructure developers are enabling tailored engine solutions for specific applications.