자동차용 전면 윈드실드 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Automotive Front Windshield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936551

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

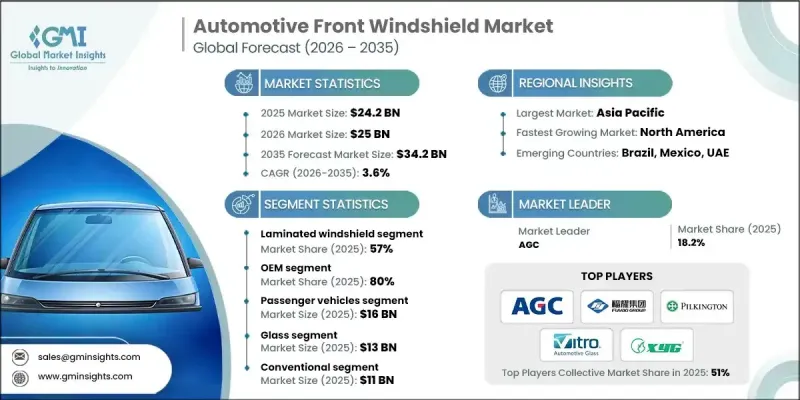

세계의 자동차용 전면 윈드실드 시장은 2025년에 242억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.6%로 성장할 전망이며, 342억 달러에 이를 것으로 예측됩니다.

세계의 자동차 생산 대수 증가, 엄격화하는 차량 안전 기준, ADAS(선진 운전 지원 시스템)의 급속한 보급에 의해 시장은 꾸준한 확대를 계속하고 있습니다. 자동차 제조업체는 운전자의 시인성 향상, 탑승자 보호 강화, 차내 소음 저감, 단열성 향상을 우선 과제로 하여 선진적인 윈드실드 솔루션의 도입을 가속화하고 있습니다. 전면 윈드실드는 더 이상 수동 부품이 아니며 현대 차량 안전 및 자동화 기능에 필수적인 센서, 카메라 및 디스플레이 시스템을 지원하도록 설계되었습니다. 전기차 및 고급차의 생산 확대는 경량화, 음향 최적화, 기술 통합을 실현한 전면 윈드실드에 대한 수요를 더욱 밀어 올리고 있습니다. 제조업체 및 공급업체는 안전과 편안함, 디지털 호환성을 결합한 다기능 설계에 주력하면서 세계 각국의 자동차 시장에서 규제 및 성능 요건의 진화에 대응하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

242억 달러

예측 금액

342억 달러

CAGR

3.6%

전면 윈드실드 기술의 지속적인 혁신으로 내구성, 기능성, 승객의 편안함이 향상되고 기존 디자인이 재구성되었습니다. 고도의 적응 유리 구조, 열 반사 및 광 반사 코팅, 차음 중간막, 디스플레이 대응 표면에 의해 내충격성의 향상, 차내 소음의 저감, 원활한 시스템 통합이 실현되고 있습니다. 강화유리 및 첨단 폴리머층의 채용으로 광학 투명도 향상, 서비스 수명 연장, 중량 최적화가 가능하며, 제조업체는 안전 규제 및 효율 목표에 대한 적합을 도모하면서 차세대 차량 아키텍처를 지원하고 있습니다.

적층 전면 윈드실드 부문은 2025년에 57%의 점유율을 차지했으며, 2026-2035년 CAGR 4%로 성장이 전망되고 있습니다. 이는 안전성, 구조적 무결성, 첨단 차량 시스템과의 호환성에 필수적인 역할을 하기 때문입니다. 다층 구조에 의해 방음 필름, 단열 코팅, 센서 통합이 가능해져, 승용차 및 상용차 양쪽에 있어서 적층 전면 윈드실드가 최적의 솔루션이 되고 있습니다.

OEM 부문은 2025년에 80%의 점유율을 차지하였고, 2026-2035년 CAGR 3.8%를 나타낼 것으로 예측됩니다. OEM 마운팅 전면 윈드실드이 시장을 독점하고 있는 이유는 정밀한 착용감, 원활한 시스템 통합, 일관된 품질 관리, 세계 안전 요건 준수를 보장하기 위해서입니다. 자동차 제조업체는 고급 전면 윈드실드 기술을 지원하고 규제 및 성능 기준을 충족하기 위해 OEM 솔루션에 의존합니다.

중국의 자동차용 전면 윈드실드 시장은 2025년에 41%의 점유율을 차지했으며, 39억 달러의 규모가 되었습니다. 이 나라는 높은 자동차 생산량, 첨단 전면 윈드실드 기술의 적극적인 도입, 자동차 공급망 전반의 긴밀한 협력으로 지역 수요를 이끌고 있습니다. 지원되는 산업 정책, 대규모 생산 능력, 통합된 공급업체 네트워크는 국내 차량 플랫폼 전반에 걸쳐 기술적으로 첨단 전면 윈드실드의 도입을 가속화하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

증가하는 자동차 생산 대수

엄격한 안전 규제

첨단 기술의 통합

전기차 및 프리미엄 차량의 성장

업계의 잠재적 위험 및 과제

고비용의 제조 공정

복잡한 설치 및 교정

시장 기회

스마트 전면 윈드실드의 도입 동향

신흥 시장 확대

자동차 안전 규제에 대한 주목 증가

코팅 및 중간막 기술의 진보

성장 가능성 분석

규제 상황

북미

미국-NHTSA, DOT 및 AI 안전규제

캐나다-교통부(Transport Canada), CMVSS 205

유럽

독일-BMDV, UNECE R43 자동차용 안전 유리

프랑스-운수성, 안전 유리 기준

영국-운수성, 건설 및 사용 규제

이탈리아-인프라 및 운수성, 차량 유리 규제

아시아태평양

중국-공업 정보화부(MIIT), GB 자동차 안전 유리 기준

일본-국토 교통성, JIS 자동차 안전 유리 규격

한국-국토교통성(MOLIT), 한국안전유리규제

인도-도로 운수성(MoRTH), 자동차 검사국(AIS), 자동차 차량 규제 위원회(CMVR)의 자동차용 유리 규격

라틴아메리카

브라질-DENATRAN, CONTRAN 자동차용 유리 규격

멕시코-통신 운수성, 차량 안전 규제

중동 및 아프리카

아랍에미리트(UAE)-도로 교통청(RTA), 전기 및 통신 규제청(ESMA)에 의한 차량 안전 및 유리 기준

사우디아라비아-통신 운수부, SASO 차량 규제

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

가격 동향

지역별

제품별

생산 통계

생산 거점

소비 거점

수출과 수입

비용 내역 분석

특허 분석

지속가능성 및 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경 배려형 이니셔티브

탄소발자국에 관한 고려 사항

이용 사례 시나리오

OEM 조달 및 구매 동향

전면 유리 공급업체의 선정 기준

장기 공급 계약 및 스팟 조달

OEM 가격 압력 및 현지화 요청

ADAS 및 센서 통합의 경제성

카메라 기반 ADAS 캘리브레이션의 비용 영향

HUD, LiDAR, 우량 및 광센서 통합의 복잡성

애프터마켓에서의 교환 및 재조정의 경제성 비교

애프터마켓에서 교환의 경제성

보험 주도의 교환 사이클

가격 차이 : OEM 대 애프터마켓 유리

모바일 설치 서비스 제공업체의 역할

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 제품별(2022-2035년)

적층 전면 윈드실드

강화 유리제 전면 윈드실드

스마트 및 선진 전면 윈드실드

제6장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

해치백 자동차

세단

SUV

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

제7장 시장 추계 및 예측 : 기술별(2022-2035년)

기존

가열식

음향

헤드업 디스플레이(HUD) 탑재

제8장 시장 추계 및 예측 : 재료별(2022-2035년)

유리

폴리머 중간층

코팅 및 필름

기타

제9장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

OEM

애프터마켓

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

싱가포르

한국

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카(MEA)

아랍에미리트(UAE)

남아프리카

사우디아라비아

제11장 기업 프로파일

세계 기업

AGC

Fuyao Glass Industry

Guardian Industries

NSG(Pilkington)

Pilkington Automotive

PPG Industries

Saint-Gobain Sekurit

Vitro Automotive Glass

Xinyi Glass

지역 기업

Asahi India Glass Limited(AIS)

Benson Automotive Glass

Cardinal Automotive Glass

Glasslam Europe

Olimpia Auto Glass

Samvardhana Motherson Automotive Glass

Shanghai Yaohua Pilkington Glass

Sisecam Automotive

Soliver

Trakya Cam Automotive

신흥 기업

AGP

Kibing

Nippon Electric Glass

PGW Auto Glass

Xinyi Overseas Automotive Glass Units

AJY

영문 목차

영문목차

The Global Automotive Front Windshield Market was valued at USD 24.2 billion in 2025 and is estimated to grow at a CAGR of 3.6% to reach USD 34.2 billion by 2035.

The market is experiencing consistent expansion driven by rising global vehicle production, increasingly strict vehicle safety standards, and the rapid integration of advanced driver-assistance technologies. Automakers are prioritizing enhanced driver visibility, improved passenger protection, reduced cabin noise, and better thermal insulation, which is accelerating the adoption of advanced front windshield solutions. Windshields are no longer passive components and are engineered to support sensors, cameras, and display systems that are essential for modern vehicle safety and automation features. Growth in electric and premium vehicle production is further boosting demand for lightweight, acoustically optimized, and technologically integrated windshields. Manufacturers and suppliers are increasingly focusing on multifunctional designs that combine safety, comfort, and digital compatibility while meeting evolving regulatory and performance expectations across global automotive markets.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$24.2 Billion

Forecast Value

$34.2 Billion

CAGR

3.6%

Ongoing innovations in windshield technology are reshaping traditional designs by improving durability, functionality, and passenger comfort. Advanced laminated glass structures, thermal and light-reflective coatings, sound-dampening interlayers, and display-ready surfaces are enhancing impact resistance, reducing interior noise, and supporting seamless system integration. The use of strengthened glass and advanced polymer layers is enabling better optical clarity, longer service life, and weight optimization, helping manufacturers align with safety regulations and efficiency targets while supporting next-generation vehicle architectures.

The laminated windshields segment accounted for 57% share in 2025 and is expected to grow at a CAGR of 4% from 2026 to 2035. This segment leads due to its essential role in safety performance, structural integrity, and compatibility with advanced vehicle systems. Multi-layer construction allows for the incorporation of sound-control films, thermal coatings, and sensor integration, making laminated windshields the preferred solution for both passenger and commercial vehicles.

The OEM segment represented 80% share in 2025 and is forecast to grow at a CAGR of 3.8% during 2026-2035. OEM-installed windshields dominate the market because they ensure precise fitment, seamless system integration, consistent quality control, and compliance with global safety requirements. Vehicle manufacturers rely on OEM solutions to support advanced windshield technologies and meet regulatory and performance standards.

China Automotive Front Windshield Market held 41% share in 2025, generating USD 3.9 billion. The country leads regional demand due to high vehicle manufacturing volumes, strong adoption of advanced windshield technologies, and close collaboration across the automotive supply chain. Supportive industrial policies, large-scale production capabilities, and integrated supplier networks continue to accelerate the deployment of technologically advanced front windshields across domestic vehicle platforms.

Key companies operating in the Global Automotive Front Windshield Market include Saint-Gobain Sekurit, Fuyao Glass Industry, AGC, Xinyi Glass, Guardian Industries, Vitro Automotive Glass, NSG Group (Pilkington), Pilkington Automotive, PPG Industries, and Sekurit Saint-Gobain Automotive Glass. Companies in the Automotive Front Windshield Market are strengthening their market position by investing in advanced glass processing technologies and multifunctional windshield solutions. Manufacturers are expanding R&D efforts to support ADAS compatibility, acoustic performance, and thermal efficiency while reducing weight. Strategic partnerships with automakers and Tier 1 suppliers are enabling early integration of new technologies into vehicle platforms. Firms are also increasing production capacity in key automotive regions to improve supply reliability and cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Vehicle

2.2.4 Technology

2.2.5 Material

2.2.6 Sales Channel

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising Vehicle Production

3.2.1.2 Stringent Safety Regulations

3.2.1.3 Advanced Technology Integration

3.2.1.4 Electric & Premium Vehicle Growth

3.2.2 Industry pitfalls and challenges

3.2.2.1 High Manufacturing Costs

3.2.2.2 Complex Installation & Calibration

3.2.3 Market opportunities

3.2.3.1 Smart Windshield Adoption

3.2.3.2 Expansion of Emerging Markets

3.2.3.3 Increasing focus on vehicle safety regulations

3.2.3.4 Advancements in coating and interlayer technologies

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S.: NHTSA, DOT, and AI Safety Regulations