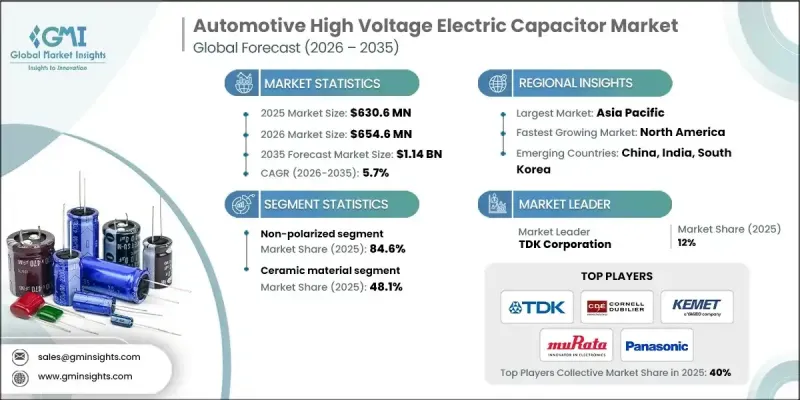

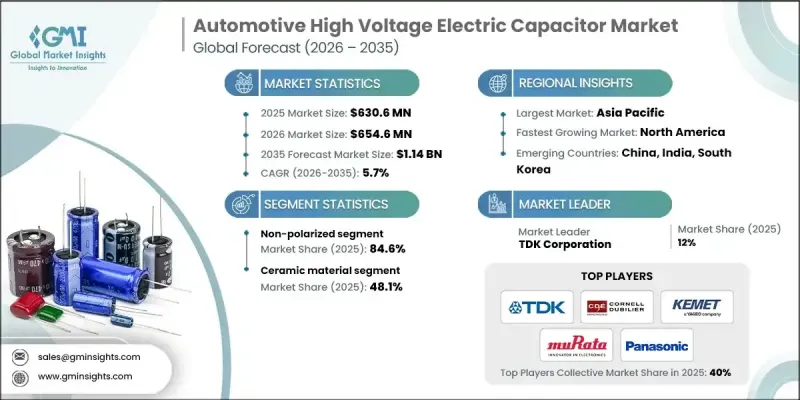

세계의 자동차용 고전압 전기 커패시터 시장은 2025년 6억 3,060만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.7%로 성장할 전망이며, 11억 4,000만 달러에 이를 것으로 예측됩니다.

800 볼트 차량 아키텍처로의 전환으로 시장은 강한 기세를 보이고 있습니다. 이를 통해 보다 빠른 충전, 케이블 무게 감소 및 소정 전력의 전류 감소가 가능합니다. 자동차 제조업체는 효율성 및 성능을 향상시키기 위해 구동 시스템을 약 400V에서 800V로 업그레이드하고 있습니다. 이 전압 상승은 인버터와 차재 충전기에 대한 전기적 부하를 증가시켜 전력 안정성, 낮은 ESR/ESL 성능, 높은 리플 전류 내성, 열 신뢰성을 확보하는 고품질 DC 링크 커패시터의 중요성을 높여줍니다. SiC 기반 인버터를 채용함으로써 스위칭 주파수 범위가 확대되고, 보다 엄격한 인덕턴스 제어, 첨단 자기 복구 필름, 가혹한 자동차 듀티 사이클 하에서 견고한 내구성을 갖춘 커패시터 설계가 요구되고 있습니다. 듀얼 모터 전륜 구동과 양방향 전력 시스템의 보급에 따라 이러한 커패시터는 EMI 억제, 회생 브레이크 및 전력 품질 유지에 매우 중요합니다. 공공 DC 급속 충전 인프라 증가는 피크 전력 수요를 더욱 높여 HV 커패시터에 무겁게 하는 전기적 및 열적 부하를 강하게 하기 때문에 내구성이 뛰어난 설계의 필요성이 강조되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 시 가치 | 6억 3,060만 달러 |

| 예측 금액 | 11억 4,000만 달러 |

| CAGR | 5.7% |

비분극성 커패시터 부문은 2025년에 84.6%의 점유율을 차지하였으며, 2035년까지 연평균 복합 성장률(CAGR) 5.6%를 나타낼 것으로 예측됩니다. 비분극성 DC 링크 커패시터는 EV 구동용 인버터 및 DC/DC 컨버터에서 고주파 디커플링의 기반 기술입니다. SiC 및 GaN 스위치의 보급에 따라 낮은 ESR/ESL, 높은 리플 전류 용량, 고속 스위칭 조건 하에서의 뛰어난 자기 복구성이 요구되고 있습니다. 제조업체 각사는 800-920V 시스템용으로 설계된 모듈형 DC 링크 필름 커패시터를 투입하고 있습니다. 이들은 인덕턴스를 줄이고 병렬 연결을 단순화하며 자동차의 듀티 사이클 하에서 열 성능을 향상시키면서 컴팩트한 레이아웃을 실현합니다. 이러한 솔루션은 다양한 작동 환경 및 조건 하에서 성능, 신뢰성 및 효율성이 매우 중요한 고전압 EV 플랫폼에서 점점 더 중요해지고 있습니다.

알루미늄 전해 커패시터와 하이브리드 폴리머 전해 커패시터를 포함한 극성 전해 커패시터 분야는 2035년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. 고전압 자동차 용도에서 이러한 커패시터는 DC 버스 상의 대용량 에너지 저장 장치로서 기능하여 고전력 정류에 의한 저주파 리플의 효율적인 처리 및 초급속 충전 및 인버터 전력 레벨의 상승에 따른 전압 과도 현상의 버퍼링을 실현합니다. 그 재채용은 대용량 에너지 저장, 고용량 밀도, 리플 전류 내성이 요구되는 용도를 지원하고 비극성 DC 링크 필름 커패시터의 성능을 보완합니다.

미국의 자동차용 고전압 전기 커패시터 시장은 2025년에 75%의 점유율을 차지했으며, 8,910만 달러의 규모가 되었습니다. 이 지역의 성장은 고출력 충전 회랑의 급속한 확대, 플릿 전동화, DC 버스 전압 요건의 상승에 의해 견인되고 있으며, 차재 커패시터는 보다 가혹한 전기적 및 열적 프로파일에 대한 내성이 요구되고 있습니다. 연방 정부의 이니셔티브, 자금 지원 프로그램 및 표준화 노력으로 EV 인프라의 상호 운용성, 신뢰성 및 성능 요구 사항이 확립되고 있으며 간접적으로 커패시터 사양을 형성하고 있습니다. 이를 통해 보다 높은 리플 내성, 낮은 ESL/ESR, 그리고 견고한 열 및 습도 바이어스 성능이 요구되고 있습니다. 소비자의 EV 채용 확대 및 전동화 이니셔티브에 대한 정부 지원이 시장 성장을 더욱 뒷받침하고 있습니다.

The Global Automotive High Voltage Electric Capacitor Market was valued at USD 630.6 million in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 1.14 billion by 2035.

The market is witnessing strong momentum due to the shift toward 800-volt vehicle architectures, which are enabling faster charging, reduced cable weight, and lower current for a given power. Automakers are upgrading traction systems from ~400 V to 800 V to enhance efficiency and performance. This voltage escalation increases electrical stress on inverters and onboard chargers, making high-quality DC link capacitors critical for power stability, low ESR/ESL performance, high ripple current tolerance, and thermal reliability. Adoption of SiC-based inverters is widening switching frequency ranges, necessitating capacitor designs with tighter inductance control, advanced self-healing films, and robust endurance under harsh automotive duty cycles. With dual-motor all-wheel-drive and bidirectional power systems becoming more common, these capacitors are also crucial for EMI suppression, regenerative braking, and maintaining power quality. Rising public DC fast charging infrastructure further drives peak power requirements, imposing heavier electrical and thermal loads on HV capacitors, underscoring the need for durable designs.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $630.6 Million |

| Forecast Value | $1.14 Billion |

| CAGR | 5.7% |

The non-polarized capacitor segment accounted for 84.6% share in 2025 and is expected to grow at a CAGR of 5.6% through 2035. Non-polarized DC link capacitors are the backbone of high-frequency decoupling in EV traction inverters and DC/DC converters. The widespread adoption of SiC and GaN switches demands low ESR/ESL, high ripple current capacity, and superior self-healing under fast switching conditions. Manufacturers are launching modular DC link film capacitors designed for 800-920 V systems, which reduce inductance, simplify parallelization, and allow compact layouts while improving thermal performance under automotive duty cycles. These solutions are increasingly essential in high-voltage EV platforms where performance, reliability, and efficiency are critical under varying operational and environmental conditions.

The polarized electrolytic capacitors segment, including aluminum and hybrid polymer types, is forecast to grow at a CAGR of 5% by 2035. In HV automotive applications, these capacitors serve as bulk energy reservoirs on DC buses, efficiently handling low-frequency ripple from high-power rectification and buffering voltage transients associated with ultra-fast charging and rising inverter power levels. Their renewed adoption supports applications where large energy storage, high capacitance density, and tolerance to ripple currents are required, complementing the performance of non-polarized DC link film capacitors.

U.S. Automotive High Voltage Electric Capacitor Market held 75% share in 2025, generating USD 89.1 million. Growth in this region is driven by rapid expansion of high-power charging corridors, fleet electrification, and rising DC bus voltage requirements, which push onboard capacitors to withstand harsher electrical and thermal profiles. Federal initiatives, funding programs, and standardization efforts are establishing interoperability, reliability, and performance expectations for EV infrastructure, indirectly shaping capacitor specifications to meet higher ripple endurance, lower ESL/ESR, and robust thermal and humidity bias performance. Increasing consumer adoption of EVs and government support for electrification initiatives further reinforce market growth.

Key players in the Global Automotive High Voltage Electric Capacitor Market include Vishay Intertechnology, Murata Manufacturing, Nichicon Corporation, TDK, Yageo Group, Panasonic, RUBYCON Corporation, Aloe Capacitors, Austin Electrical Enclosures & Capacitors, Cornell Dubilier, United Chemi-Con, Elna, Havells, Kemet, Kyocera AVX, Lelon Electronics, Schneider Electric, and Siemens. Companies in the Automotive High Voltage Electric Capacitor Market are pursuing strategies to strengthen their market presence by investing in R&D to develop capacitors with higher thermal endurance, lower ESR/ESL, and improved ripple current tolerance suitable for 800-920 V systems. Firms are expanding production capacities and forming partnerships with automakers and power electronics suppliers to ensure integration in next-generation EV platforms. Modular capacitor design and scalable solutions enable faster adoption across diverse EV architectures. Strategic acquisitions and collaborations are also being leveraged to access advanced materials, self-healing film technology, and SiC/GaN inverter expertise.