SDV as a Service(SDVaaS) 플랫폼 시장 : 시장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

SDV-as-a-Service (SDVaaS) Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1936510

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

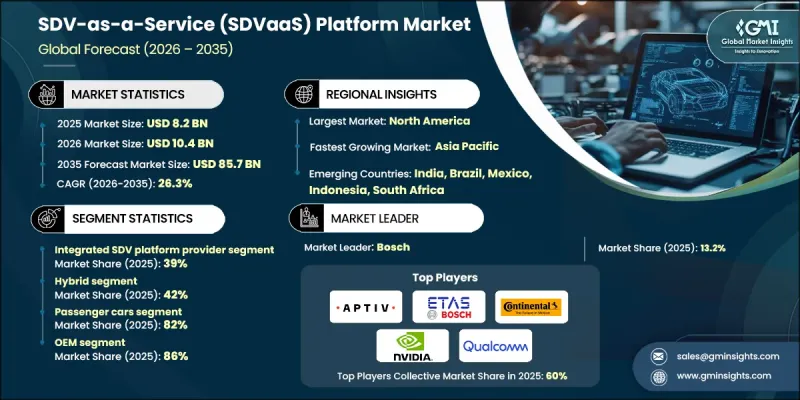

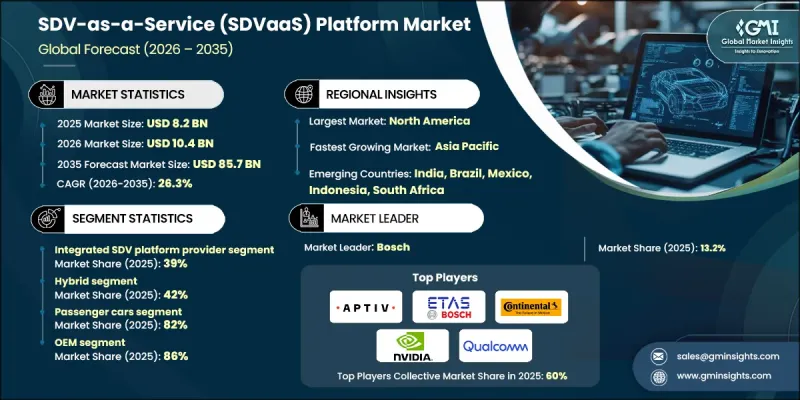

세계의 SDVaaS 플랫폼 시장은 2025년에 82억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 26.3%로 성장할 전망이며, 857억 달러에 이를 것으로 예측됩니다.

시장 성장은 스마트폰 차량 경험에 대한 소비자 수요 증가, 빈번한 소프트웨어 강화, 고도로 개인화된 이동성 기능과 직접 관련이 있습니다. 자동차 제조업체는 구매 후 차량을 진화시키기 위해 무선 업데이트(OTA), 디지털 기능 활성화, 구독 서비스를 지원하는 클라우드 지원 소프트웨어 플랫폼을 채택하여 적극적으로 대응하고 있습니다. 차량은 정적 기계가 아닌 소프트웨어 정의 제품으로 작용하는 경향이 강해져 소유 라이프사이클 전반에 걸쳐 지속적인 가치 창출을 가능하게 합니다. 이 혁신은 수익 모델을 재구성하고 고객 참여를 강화하며 판매 후 수익 기회를 확대합니다. OEM 제조업체는 SDVaaS 플랫폼을 활용하여 차량, 드라이버 및 클라우드 서비스를 실시간으로 연결하는 확장 가능한 디지털 에코시스템을 제공합니다. 원활한 연결성과 지능형 기능에 대한 기대가 높아지는 가운데 SDFaaS는 세계 승용차 및 상용차 부문에서 차세대 차량 전략의 기반 요소가 됩니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

82억 달러

예측 금액

857억 달러

CAGR

26.3%

자동차 제조업체는 분산형 ECU 구조에서 구역별 전자 및 전기 아키텍처에 의해 지원되는 집중형 컴퓨팅으로의 전환을 적극적으로 추진하고 있습니다. 이 아키텍처의 전환은 SDVaaS 비즈니스 모델에 필요한 기술 기반을 구축하는 동시에 차량 배선을 간소화하고, 시스템 효율성을 향상시키며, 여러 플랫폼에 걸쳐 통일적인 서비스 제공을 가능하게 합니다. 중앙 집중식 및 구역별 설계는 소프트웨어 재사용, 신기능의 신속한 전개, 다양한 차종 라인 간 용이한 확장성을 제공합니다. OEM은 SDV 플랫폼의 성숙을 가속화하기 위해 클라우드 제공업체, AI 개발자, 기술 기업과의 협업을 강화하고 있습니다. 이러한 파트너십은 고급 분석 기능, 고성능 컴퓨팅, 안전한 클라우드 인터페이스를 제공하여 개발 기간 단축, 원격 제품 개발, 전개, 유지보수, 수명 주기 관리를 제공합니다. SDVaaS 플랫폼은 자동차 제조업체들이 더 풍부한 디지털 경험을 제공하고 차량의 수명주기를 통해 고객과의 지속적인 관계를 유지할 수 있도록 합니다.

통합형 SDV 플랫폼 부문은 2025년에 39%의 점유율을 차지했으며, 2026-2035년 연평균 복합 성장률(CAGR) 27%로 성장할 전망입니다. 이러한 공급업체가 이점을 유지하는 이유는 차량 클라우드 인프라, 운영 체제 및 용도 계층을 통합 플랫폼에 통합한 종합적인 종단 간 솔루션을 제공하기 때문입니다. 이러한 통합은 대규모 OTA 업데이트를 지원하여 여러 차종 및 제품 포트폴리오에 걸쳐 동적 서비스 전개를 가능하게 합니다. 통합 제공업체는 격리된 도구가 아닌 완전한 생태계를 제공함으로써 OEM 채택을 간소화하고 완전한 소프트웨어 정의 차량으로의 전환을 가속화하면서 세계 차량 전체에서 일관성, 보안 및 확장성을 보장합니다.

하이브리드 도입 모델 부문은 2025년에 42%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 27.3%로 성장할 것으로 예측됩니다. 하이브리드 SDFaaS 전개는 온프레미스 인프라와 프라이빗 및 퍼블릭 클라우드 환경을 융합하여 기업에 운영 유연성 및 비용 관리를 강화합니다. 자동차 제조업체는 데이터 처리, 분석 및 향상된 기능을 위해 클라우드 확장성을 활용하면서 민감한 워크로드를 로컬로 관리합니다. 이 접근법은 규제, 성능 및 보안 요구 사항을 충족하면서 정확한 비용 최적화를 가능하게 합니다. 하이브리드 전개는 단계적인 SDV 전개를 지원하고 차량 소프트웨어의 복잡성이 증가함에 따라 OEM이 혁신 속도와 인프라 안정성의 균형을 맞출 수 있습니다.

미국의 SDVaaS 플랫폼 시장은 2025년 26억 2,000만 달러에 달했습니다. 미국은 주요 자동차 제조업체와 기술 기업 간 강력한 협력, 특히 커넥티드 자동차 인프라, OTA 기능, V2X 통신, 자율 시스템을 추진하는 혁신 허브 내에서의 협업을 통해 SDV 도입에서 주도적인 입장을 유지하고 있습니다. 연방정부의 지원은 자율주행차의 시험 주행 및 커넥티드 모빌리티 구상을 촉진하는 정책을 통해 이 우위를 강화하고 있습니다. 이러한 시책은 연구 투자를 촉진하고 고속도로, 스마트 회랑, 도시 환경에서 선진적인 SDV 기술의 실증 실험을 가능하게 함으로써, 미국을 SDV의 혁신과 도입에 있어서 세계의 중심지로 자리매김하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

개인화에 대한 소비자 수요

집중형 E/E 아키텍처의 도입 상황

OEM 기술 파트너십 확대

규제 주도의 보안 OTA

업계의 잠재적 위험 및 과제

사이버 보안 및 프라이버시 리스크

분단된 크로스 브랜드 기준

시장 기회

구독형 플랫폼 수익

OEM 및 클라우드의 전략적 제휴

타사 개발자 생태계

데이터 구동형 모빌리티 서비스

성장 가능성 분석

규제 상황

북미

미국 운수성(DOT) 기준

직업안전보건국(OSHA) 가이드라인

미국 환경보호청(EPA)

유럽

EN ISO 컨테이너 표준

유럽연합의 관세 및 안전규제

BS EN/CEN 규격

국가 규격(UNE, DIN 등)

아시아태평양

중국 국가 표준(GB 규격)

일본 JIS 규격 요건

한국 KS 인증

인도의 BIS 규격

태국공업규격협회(TISI)

라틴아메리카

INMETRO(국립 계량 연구소)

INTI 인증(국립공업기술연구소)

NOM 규격(Norma Oficial Mexicana)

중동 및 아프리카

ESMA/에미레이트 호환성 평가 체계(ECAS)

GCC 기술규제

SABS 인증

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

비용 내역 분석

벤더의 비용 구조

비용 구성요소 도입

지속적인 운영 비용

간접적인 고객 비용

특허 분석

지속가능성 및 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서 에너지 효율화

환경에 배려한 대처

탄소발자국에 관한 고려 사항

이용 사례

비즈니스 모델 및 수익화 모델

SDVaaS 비즈니스 모델의 전체상

플랫폼 라이선싱 및 구독 모델

사용량 베이스 및 종량 과금 모델

개발 서비스(DaaS) 모델

수익 분배 및 파트너십 모델

구매자의 의사결정 기준 및 조달 행동

바이어 환경 개관

의사결정 프로세스의 분석

중요한 평가 기준

벤더 선정 및 RFP 프로세스

협상의 역학

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 플랫폼별(2022-2035년)

통합형 SDV 플랫폼 제공업체

도메인 솔루션 제공업체

컴포넌트 전문 플랫폼

서비스로서의 설계 및 개발

소프트웨어 운영 서비스(SOaaS)

제6장 시장 추계 및 예측 : 차량별(2022-2035년)

승용차

해치백

세단

SUV

상용차

LCV(소형 상용차)

중형 상용차(MCV)

대형 상용차(HCV)

제7장 시장 추계 및 예측 : 용도별(2022-2035년)

ADAS 및 자율주행 플랫폼

운영체제 및 미들웨어 플랫폼

인포테인먼트 및 커넥티비티 플랫폼

차량 효율 및 성능 플랫폼

안전, 보안 및 기능 안전 플랫폼

제8장 시장 추계 및 예측 : 전개 모드별(2022-2035년)

온프레미스

프라이빗 클라우드

퍼블릭 클라우드

하이브리드

제9장 시장 추계 및 예측 : 최종 용도별(2022-2035년)

테크놀로지 네이티브 및 SDV 퍼스트의 OEM 제조업체

기존 자동차 제조업체

Tier 1 및 Tier 2 자동차 부품 제조업체

자동차용 소프트웨어 및 기술 제공업체

반도체 및 컴퓨팅 플랫폼 제공 기업

제10장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

폴란드

루마니아

아시아태평양

중국

인도

일본

한국

ANZ

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계 기업

Amazon Web Services(AWS)

Aptiv

ARM

BlackBerry

Continental

Google

Microsoft

NVIDIA

Qualcomm

Robert Bosch

지역 기업

Elektrobit Automotive

ETAS

HERE Technologies

Infineon Technologies

NXP Semiconductors

Red Hat

Renesas Electronics

STMicroelectronics

TTTech Auto

Visteon

신흥 기업

Aurora Innovation

Canoo

Motional

Sonatus

Woven by Toyota

AJY

영문 목차

영문목차

The Global SDV-as-a-Service Platform Market was valued at USD 8.2 billion in 2025 and is estimated to grow at a CAGR of 26.3% to reach USD 85.7 billion by 2035.

Market growth directly links to rising consumer demand for smartphone-style vehicle experiences, frequent software enhancements, and highly personalized mobility features. Automakers actively respond by adopting cloud-enabled software platforms that support over-the-air updates, digital feature activation, and subscription-based services, allowing vehicles to evolve well after purchase. Vehicles increasingly function as software-defined products rather than static machines, enabling continuous value creation across the ownership lifecycle. This transformation reshapes revenue models, strengthens customer engagement, and expands post-sale monetization opportunities. OEMs rely on SDVaaS platforms to deliver scalable digital ecosystems that connect vehicles, drivers, and cloud services in real time. As expectations for seamless connectivity and intelligent features rise, SDVaaS becomes a foundational element in next-generation vehicle strategies across passenger and commercial segments worldwide.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$8.2 Billion

Forecast Value

$85.7 Billion

CAGR

26.3%

Automakers actively transition from distributed ECU structures to centralized computing supported by zonal electronic and electrical architectures. This architectural shift creates the technical foundation required for SDVaaS business models while simplifying vehicle wiring, improving system efficiency, and enabling unified service delivery across multiple platforms. Centralized and zonal designs allow software reuse, faster deployment of new features, and easier scalability across different vehicle lines. OEMs increasingly collaborate with cloud providers, AI developers, and technology companies to accelerate SDV platform maturity. These partnerships provide advanced analytics, high-performance computing, and secure cloud interfaces that shorten development timelines and support remote product creation, deployment, maintenance, and lifecycle management. SDVaaS platforms empower automakers to deliver richer digital experiences and maintain continuous interaction with customers throughout the vehicle lifespan.

The integrated SDV platform segment held 39% share in 2025 and will grow at a CAGR of 27% from 2026 to 2035. These providers dominate because they deliver comprehensive, end-to-end solutions that combine vehicle cloud infrastructure, operating systems, and application layers into unified platforms. Such integration supports large-scale OTA updates and enables dynamic service deployment across multiple vehicle models and product portfolios. By offering complete ecosystems rather than isolated tools, integrated providers simplify adoption for OEMs and accelerate the transition toward fully software-defined vehicles while ensuring consistency, security, and scalability across global fleets.

The hybrid deployment model segment held a 42% share in 2025 and is expected to grow at a CAGR of 27.3% through 2035. Hybrid SDVaaS deployments blend on-premises infrastructure with private and public cloud environments, giving enterprises greater operational flexibility and cost control. Automakers manage sensitive workloads locally while leveraging cloud scalability for data processing, analytics, and feature expansion. This approach allows precise cost optimization while meeting regulatory, performance, and security requirements. Hybrid deployments support phased SDV rollouts and enable OEMs to balance innovation speed with infrastructure stability as vehicle software complexity increases.

US SDV-as-a-Service Platform Market reached USD 2.62 billion in 2025. The US maintains leadership in SDV adoption due to strong collaboration between major automakers and technology firms, particularly within innovation hubs that advance connected vehicle infrastructure, OTA capabilities, V2X communication, and autonomous systems. Federal support strengthens this position through policies that encourage autonomous vehicle testing and connected mobility initiatives. These measures boost research investments and enable real-world validation of advanced SDV technologies across highways, smart corridors, and urban environments, positioning the US as a global center for SDV innovation and deployment.

Key players active in the Global SDV-as-a-Service Platform Market include NVIDIA, Bosch, Amazon Web Services, Qualcomm Technologies, Google, Continental, Microsoft, BlackBerry QNX, Vector Informatik, and Aptiv. Companies operating in the SDV-as-a-Service Platform Market strengthen their foothold by investing heavily in end-to-end software ecosystems, cloud-native architectures, and scalable computing platforms. Strategic alliances with automakers, semiconductor firms, and AI developers help providers expand technical capabilities and accelerate deployment timelines. Vendors focus on modular platform designs that allow OEMs to customize features while maintaining core system stability. Continuous innovation in cybersecurity, data analytics, and real-time vehicle intelligence remains central to competitive positioning.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.3 GMI AI policy & data integrity commitment

1.4 Research trail & confidence scoring

1.4.1 Research trail components

1.4.2 Scoring components

1.5 Data collection

1.5.1 Partial list of primary sources

1.6 Data mining sources

1.6.1 Paid sources

1.7 Base estimates and calculations

1.7.1 Base year calculation

1.8 Forecast model

1.9 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Platform

2.2.3 Vehicle

2.2.4 Application

2.2.5 Deployment model

2.2.6 End use

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook

2.6 Strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Consumer demand for personalization

3.2.1.2 Centralized E/E architectures adoption

3.2.1.3 OEM-tech partnerships expansion

3.2.1.4 Regulatory-driven secure OTA

3.2.2 Industry pitfalls and challenges

3.2.2.1 Cybersecurity and privacy risks

3.2.2.2 Fragmented cross-brand standards

3.2.3 Market opportunities

3.2.3.1 Subscription-based platform revenues

3.2.3.2 OEM-cloud strategic alliances

3.2.3.3 Third-party developer ecosystems

3.2.3.4 Data-driven mobility services

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S. Department of Transportation (DOT) Standards

3.4.1.2 Occupational Safety and Health Administration (OSHA) Guidelines

3.4.1.3 U.S. Environmental Protection Agency (EPA)

3.4.2 Europe

3.4.2.1 EN ISO Container Standards

3.4.2.2 European Union Customs and Safety Regulations

3.4.2.3 BS EN / CEN Standards

3.4.2.4 National Standards (UNE, DIN, etc.)

3.4.3 Asia Pacific

3.4.3.1 China GB (Guobiao) Standards

3.4.3.2 Japan JIS Requirements

3.4.3.3 Korea KS Certification

3.4.3.4 Indian BIS Standards

3.4.3.5 Thai Industrial Standards Institute (TISI)

3.4.4 Latin America

3.4.4.1 INMETRO (National Institute of Metrology)

3.4.4.2 INTI certification (Instituto Nacional de Tecnologia Industrial)