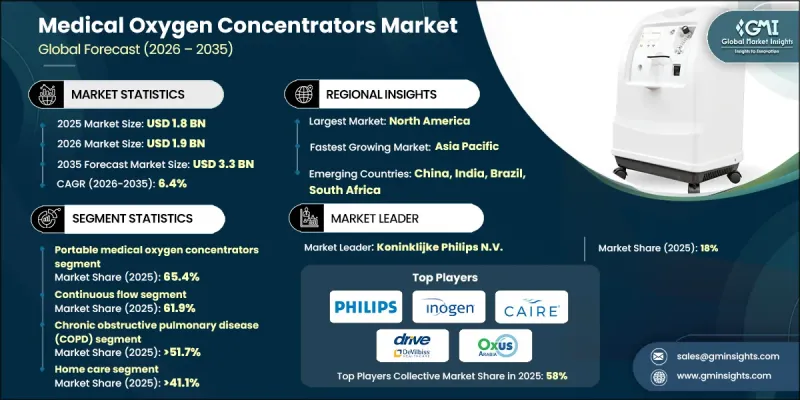

세계의 의료용 산소발생기 시장은 2025년 18억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 6.4%로 성장할 전망이며, 33억 달러에 이를 것으로 예측됩니다.

이 성장은 만성 호흡기 질환의 발생률 증가, 대기 오염에 대한 노출 증가 및 세계 노인 인구 비율 증가로 인한 것입니다. 산소발생기는 만성 호흡기 질환으로 인한 호흡 곤란에 직면하는 환자에게 장기 산소 요법을 제공하는 데 중요한 역할을 합니다. 이 장치는 주변 공기를 여과하여 산소를 생성하고 농축 산소를 환자에게 직접 공급하므로 부피가 큰 저장 용기가 필요하지 않습니다. 의료 시스템은 비용 효율적이고 신뢰성 있으며 확장 가능한 호흡기 솔루션으로 산소발생기의 도입을 확대하고 있습니다. 공중위생 시책 추진, 의료기기에 대한 액세스 개선, 쾌적성을 중시한 케어를 요구하는 환자의 의향을 배경으로, 재택치료에 대한 명확한 이행이 진행되고 있는 것도 시장을 뒷받침하고 있습니다. 장치의 효율성, 소음 저감, 에너지 성능의 향상도 도입 촉진에 기여하고 있습니다. 조기 호흡기 개입 및 장기적인 질병 관리의 중요성에 대한 인식 증가는 병원, 클리닉 및 재택 관리 환경에서 수요를 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 33억 달러 |

| CAGR | 6.4% |

2025년 현재 휴대용 의료용 산소발생기 부문은 65.4%의 점유율을 차지했습니다. 이 시스템은 컴팩트하고 가벼운 설계로 이동성, 편리성 및 지속적인 산소 공급을 실현합니다. 환자는 일상 생활이나 여행 중에도 자립적인 생활을 할 수 있어 치료를 중단하지 않고 계속할 수 있는 휴대형 솔루션을 점점 선호되고 있습니다. 보다 스마트한 산소 공급 시스템, 긴 수명 배터리 성능, 디지털 연결성 등 지속적인 기술적 진보가 이 부문의 확대를 뒷받침하고 있습니다.

연속 유량 부문은 2025년에 61.9%의 점유율을 차지했습니다. 연속 유량 장치는 안정된 산소 공급을 실현하기 때문에 안정 시 및 수면 중에 안정된 치료를 필요로 하는 환자에게 필수적입니다. 그 신뢰성과 높은 산소 수요에 대한 대응 능력으로 임상 현장 및 재택 치료 모두에서 널리 활용되고 있습니다.

미국의 의료용 산소발생기 시장은 2025년 6억 3,520만 달러에 달했습니다. 견고한 의료 인프라, 광범위한 보험 적용 범위, 재택 치료 솔루션의 보급 확대가 시장을 견인하고 있습니다. 디지털 건강 플랫폼 및 원격 모니터링 시스템과의 통합으로 다양한 의료 현장에서의 사용이 더욱 가속화되고 있습니다.

The Global Medical Oxygen Concentrators Market was valued at USD 1.8 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 3.3 billion by 2035.

Growth is driven by the rising incidence of chronic respiratory disorders, increasing air pollution exposure, and the growing proportion of elderly populations worldwide. Oxygen concentrators play a vital role in delivering long-term oxygen therapy for patients facing breathing difficulties caused by chronic respiratory conditions. These devices generate oxygen by filtering ambient air and supplying concentrated oxygen directly to patients, eliminating the need for bulky storage cylinders. Healthcare systems increasingly adopt oxygen concentrators as cost-effective, reliable, and scalable respiratory solutions. The market also benefits from a clear shift toward home-based healthcare, supported by public health initiatives, improved access to medical devices, and patient preference for comfort-driven care. Advances in device efficiency, noise reduction, and energy performance further enhance adoption. Growing awareness of early respiratory intervention and long-term disease management strengthens demand across hospitals, clinics, and home care environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 6.4% |

The portable medical oxygen concentrators segment held 65.4% share in 2025. These systems provide mobility, convenience, and continuous oxygen support in compact and lightweight designs. Patients increasingly prefer portable solutions that allow independence and uninterrupted therapy during daily activities or travel. Ongoing technological improvements, including smarter oxygen delivery systems, extended battery performance, and digital connectivity, continue to drive segment expansion.

The continuous flow segment held a 61.9% share in 2025. Continuous flow devices deliver a constant oxygen supply, making them essential for patients requiring stable therapy during rest or sleep. Their reliability and ability to support higher oxygen needs make them widely used in both clinical and homecare settings.

United States Medical Oxygen Concentrators Market reached USD 635.2 million in 2025. Strong healthcare infrastructure, broad insurance coverage, and rising adoption of home healthcare solutions support market leadership. Integration with digital health platforms and remote monitoring systems further accelerates usage across care settings.

Key companies operating in the Global Medical Oxygen Concentrators Market include Koninklijke Philips N.V., Inogen, CAIRE, Drive DeVilbiss Healthcare, Teijin Limited, React Health, Precision Medical, O2 Concepts, Daikin Industries, Jiangsu Yuyue Medical Equipment & Supply, BPL Medical Technologies, BESCO Medical, Foshan Keyhub Electronic Industries, ESAB Corporation, and OXUS. Companies in the medical oxygen concentrators market strengthen their market position by focusing on product innovation, portability, and energy efficiency. Manufacturers invest in lightweight designs, quieter operation, and longer battery life to enhance patient comfort and usability. Expansion into homecare and telehealth-integrated solutions supports wider adoption. Strategic partnerships with healthcare providers and distributors improve market access and service reach. Regulatory compliance, quality certifications, and patient safety remain core priorities.