Traffic Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928987

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 246 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

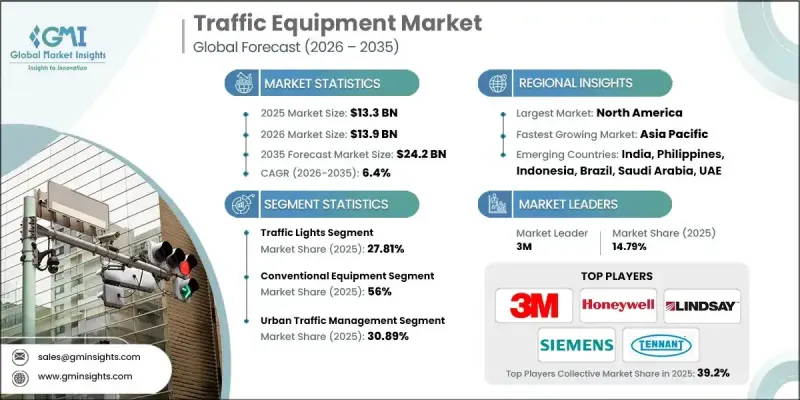

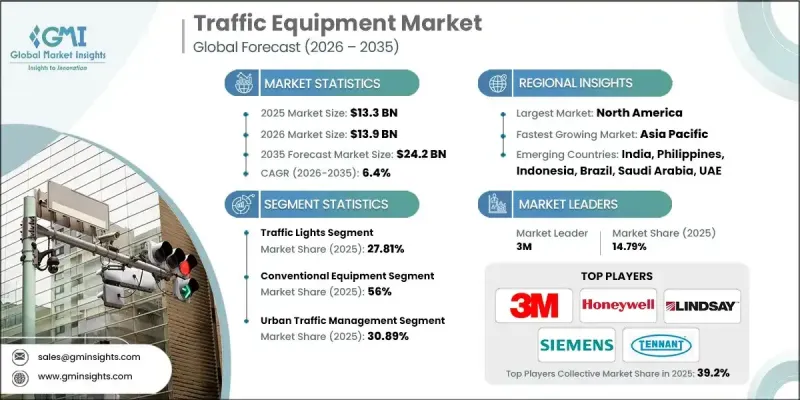

세계의 교통 설비 시장은 2025년에 133억 달러로 평가되었으며, 2035년까지 CAGR 6.4%로 성장하여 242억 달러에 달할 것으로 예측됩니다.

시장 확대는 도시 교통의 급속한 변화, 대규모 인프라 구축, 세계 도로 안전 관리에 대한 관심의 증가로 뒷받침되고 있습니다. 교통 설비는 더 이상 기본적인 도로변 설치물에 국한되지 않고, 상호연결된 기술 주도형 교통 관리 솔루션으로 진화하고 있습니다. 신호 시스템, 도로 표지판, 장벽, 모니터링 도구, 지능형 제어 장치 등의 장비는 통합된 안전 및 이동성 네트워크의 일부로 도입되고 있습니다. 이러한 시스템은 도시 도로망, 고속도로, 건설 지역, 지자체 인프라뿐만 아니라 응답성과 신뢰성이 매우 중요한 스마트 시티 개발 프로그램에도 널리 적용되고 있습니다. 정부 기관과 교통 당국은 교통 흐름 개선, 교통 체증 감소, 도로 안전 향상을 위해 투자를 확대하고 있습니다. 안전 중시 정책과 지능형 교통 이니셔티브는 구식 장비에서 첨단 표준을 준수하는 솔루션으로 교체하는 것을 가속화하고 있습니다. 선진 지역에서는 자동화, 가시성, 데이터 연결성이 강조되는 반면, 개발도상국에서는 기초 교통 통제 인프라의 확충과 단계적 디지털화에 초점을 맞추고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035

개시시 가치

133억 달러

예측 금액

242억 달러

CAGR

6.4%

신호등 부문은 2025년 27.81%의 점유율을 차지했으며, 2035년까지 연평균 4.6%의 성장률을 기록할 것으로 전망됩니다. 도시화 추세와 차량 밀도의 증가로 인해 효율적인 교차로 및 보행자 교통 통제에 대한 수요가 지속되고 있습니다. 현대의 신호 시스템은 지속가능한 모빌리티 목표를 지원하기 위해 에너지 절약 기술과 적응 기능을 점점 더 많이 도입하고 있습니다.

기존 장비는 2025년 56%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 5.6%로 성장할 것으로 예상됩니다. 저렴한 가격, 내구성, 규제 준수, 다양한 도로 환경에서의 도입 용이성 등으로 인해 전통적인 교통 제어 솔루션이 계속 주류를 이루고 있습니다.

미국 교통 장비 시장은 2025년 85.17%의 점유율을 차지하며 41억 달러의 수익을 창출할 것으로 예상됩니다. 교통 인프라와 도로 현대화에 대한 지속적인 투자로 인해 국내 전체에서 강한 수요가 지속되고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계의 부가가치

밸류체인에 영향을 미치는 요인

디스럽션

업계에 대한 영향요인

성장 촉진요인

도로 인프라 개발에 대한 투자 증가

도로 안전과 사고 절감에 대한 주목 상승

스마트 시티 및 고도 교통 시스템(ITS) 확대

도시화와 차량 밀도 증가

업계의 잠재적 리스크와 과제

첨단 교통 시스템에의 초기 투자액이 고액인 것

지역별로 분단 된 규제 기준

시장 기회

스마트하고 접속된 교통 기기의 도입

신흥 경제국의 인프라 정비 진전

민관 제휴(PPP) 프로젝트

성장 가능성 분석

규제 상황

북미

연방 고속도로국(FHWA) 기준

유럽

독일 : 교통 신호 및 도로 안전법

영국 : 교통 표지 규칙 및 일반 지시(TSRGD)

프랑스 : 모빌리티 지향법(LOM법)

이탈리아 : 국가 도로 안전·인프라 규제

아시아태평양

중국 : 스마트 시티 및 ITS 가이드라인

인도 : 고도 교통 관리 시스템 의무화

일본 : 도로 교통법과 ITS 정책

호주 : 주 레벨 스마트 교통 인프라 규제

라틴아메리카

브라질 : 국가 교통안전 가이드라인

멕시코 : 도시 도로 안전 프로그램

아르헨티나 : 주별 교통 및 도로 안전 규제

중동 및 아프리카

아랍에미리트 : 전기자동차(EV) 및 스마트 시티 교통 규제

사우디아라비아 : 도로 안전과 교통 현대화 정책

남아프리카공화국 : 그린 교통 전략

Porters 분석

PESTEL 분석

생산 통계

생산 거점

소비 거점

수출입

기술과 혁신 동향

현재 기술 동향

신기술

특허 분석

가격 분석

지역별

제품별

비용 내역 분석

지속가능성과 환경 영향 분석

지속가능한 대처

폐기물 절감 전략

생산의 에너지 효율

친환경적인 대처

탄소발자국에 관한 고려사항

향후 전망과 기회

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

주요 시장 기업 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴·협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추정 및 예측 : 제품별, 2022-2035

신호기

교통안전 표지

교통 차단기

교통 콘

교통 관리 게이트

기타

제6장 시장 추정 및 예측 : 용도별, 2022-2035

도시 교통 관리

고속도로 관리

주차장 관리

작업 구역 안전 대책

기타

제7장 시장 추정 및 예측 : 기술별, 2022-2035

기존 설비

스마트/커넥티드 기기

제8장 시장 추정 및 예측 : 최종 용도별, 2022-2035

정부·자치체

민간 계약업체

운송 기관

제9장 시장 추정 및 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

아시아태평양

중국

인도

일본

호주

한국

필리핀

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제10장 기업 개요

세계 기업

3 M

Econolite

Honeywell

Iteris

Jenoptik

Kapsch TrafficCom

Lindsay

Siemens

SWARCO

TrafFix Devices

지역 플레이어

Cortina Safety Products

Dicke Safety Products

Eagle Manufacturing

HSS Hire

JSP Safety

Melba Swintex

Oaklands

Oxford Plastics

Pexco

Plasticade

Road Traffic Solutions

Seton

Tennants

신흥 기업

National Tool Hire Shops

Work Area Protection

KSM

영문 목차

영문목차

The Global Traffic Equipment Market was valued at USD 13.3 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 24.2 billion by 2035.

Market expansion is supported by rapid urban mobility transformation, large-scale infrastructure development, and heightened focus on road safety management worldwide. Traffic equipment is no longer limited to basic roadside installations and is increasingly evolving into interconnected, technology-driven traffic management solutions. Devices such as signaling systems, road markings, barriers, monitoring tools, and intelligent control units are now being deployed as part of integrated safety and mobility networks. These systems are widely adopted across urban road networks, highways, construction zones, and municipal infrastructure, as well as within smart city development programs where responsiveness and reliability are critical. Government bodies and transportation authorities are increasing investments to improve traffic flow, reduce congestion, and enhance roadway safety. Safety-focused policies and intelligent transport initiatives are accelerating the replacement of legacy equipment with advanced, compliant solutions. While developed regions emphasize automation, visibility, and data connectivity, developing economies continue to focus on expanding foundational traffic control infrastructure alongside gradual digital upgrades.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$13.3 Billion

Forecast Value

$24.2 Billion

CAGR

6.4%

The traffic lights segment held 27.81% share in 2025 and is projected to grow at a CAGR of 4.6% through 2035. Strong urbanization trends and increasing vehicle density are sustaining demand for efficient intersection and pedestrian traffic control. Modern signaling systems are increasingly incorporating energy-efficient technologies and adaptive features to support sustainable mobility objectives.

The conventional equipment accounted for 56% share in 2025 and is expected to grow at a CAGR of 5.6% from 2026 to 2035. Traditional traffic control solutions continue to dominate due to their affordability, durability, regulatory compliance, and ease of deployment across diverse road environments.

United States Traffic Equipment Market held 85.17% share and generated USD 4.10 billion in 2025. Ongoing investments in transportation infrastructure and roadway modernization are sustaining strong demand across the country.

Key companies operating in the Global Traffic Equipment Market include Siemens, 3M, Honeywell, Lindsay, TrafFix Devices, Cortina Safety, Eagle Manufacturing, Dicke Safety, JSP Safety, and Tennants. Companies in the traffic equipment market are reinforcing their competitive position through innovation, infrastructure partnerships, and product diversification. Many players are investing in smart and connected equipment that integrates sensors, communication technologies, and data analytics to improve traffic efficiency and safety. Expanding product portfolios to address both traditional and intelligent traffic systems is a key strategy. Manufacturers are also focusing on regulatory compliance and certification to support adoption across public infrastructure projects. Strategic collaborations with government agencies and contractors help secure long-term contracts.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Technology

2.2.4 Application

2.2.5 End Use

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising Investments in Road Infrastructure Development

3.2.1.2 Growing Emphasis on Road Safety and Accident Reduction

3.2.1.3 Expansion of Smart Cities and Intelligent Transport Systems (ITS)

3.2.1.4 Urbanization and Rising Vehicle Density

3.2.2 Industry pitfalls and challenges

3.2.2.1 High Initial Investment for Advanced Traffic Systems

3.2.2.2 Fragmented Regulatory Standards Across Regions

3.2.3 Market opportunities

3.2.3.1 Adoption of Smart and Connected Traffic Equipment

3.2.3.2 Infrastructure Upgrades in Emerging Economies

3.2.3.3 Public-Private Partnership (PPP) Projects

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 Federal Highway Administration (FHWA) Standards.

3.4.2 Europe

3.4.2.1 Germany: Traffic Signal and Road Safety Act

3.4.2.2 UK: Traffic Signs Regulations & General Directions (TSRGD)

3.4.2.3 France: Mobility Orientation Law (LOM Act)

3.4.2.4 Italy: National Road Safety and Infrastructure Regulations

3.4.3 Asia Pacific

3.4.3.1 China: Smart City and ITS Guidelines

3.4.3.2 India: Intelligent Traffic Management System Mandate