건설 펀치 리스트 소프트웨어 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)

Construction Punch List Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928980

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 245 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

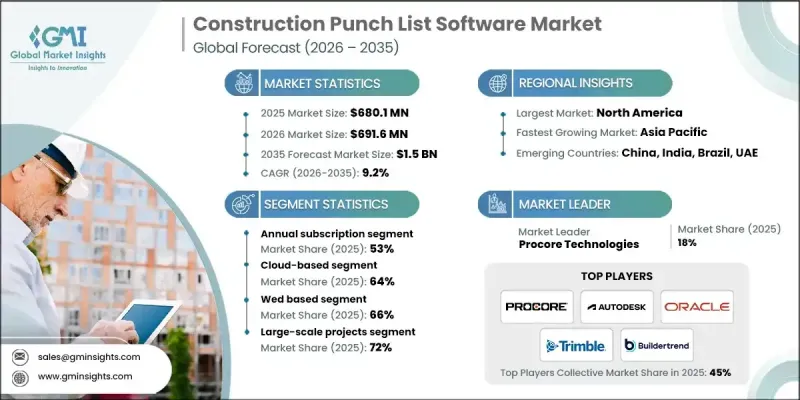

세계의 건설 펀치 리스트 소프트웨어 시장은 2025년에 6억 8,010만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.2%로 성장하여 15억 달러에 이를 것으로 예측됩니다.

시장 성장은 건설 팀이 프로젝트 완료 단계의 과제 식별, 추적 및 해결의 효율성을 높이기 위해 디지털 도구에 대한 의존도를 높이고 있음을 반영합니다. 펀치리스트 소프트웨어는 건설 라이프사이클 전반에 걸쳐 이해관계자간의 실시간 협업을 지원하여 투명성과 책임성을 향상시킵니다. 건설 부문이 성숙하고 디지털 대응력이 높은 지역에서 도입이 가장 많이 진행되고 있습니다. 북미는 빠른 기술 도입과 확립된 SaaS 환경으로 선두를 유지하고 있으며, 유럽은 엄격한 품질 및 컴플라이언스 기준에 힘입어 그 뒤를 잇고 있습니다. 디지털 전환이 품질 관리 및 완료 작업의 워크플로우 관리 방식을 재구성하는 가운데 업계는 빠르게 진화하고 있습니다. 인공지능을 활용한 분석은 프로젝트의 미비점을 자동 식별하여 정확성과 효율성을 높이고 있으며, 모바일 퍼스트 개발 전략은 현장의 조작성과 대응력을 높이고 있습니다. 클라우드 기반 배포는 확장성, 지속적인 업데이트, 멀티 디바이스 지원, 안전한 데이터 관리, 현지 인프라의 부담을 줄여주기 때문에 선호되는 모델입니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

6억 8,010만 달러

예측 금액

15억 달러

CAGR

9.2%

연간 구독 모델 부문은 2025년에 53%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 8.5%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이러한 계획은 공급자에게는 예측 가능한 수익원을 제공하고, 건설사에게는 대규모 선행 투자를 피함으로써 재무 계획을 간소화합니다. 연간 가격 체계는 비용 효율성과 유연성의 균형을 이루기 때문에 여러 프로젝트를 동시에 관리하는 계약자에게 특히 매력적입니다.

클라우드 기반 솔루션은 2025년 64%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 9.7%를 보일 것으로 예측됩니다. 클라우드 플랫폼은 전용 하드웨어나 사내 IT 리소스가 필요하지 않으면서도 원활한 업데이트, 확장 가능한 성능, 안전한 데이터 스토리지를 제공합니다. 공유 인프라 모델은 강력한 데이터 보호 표준을 유지하면서 효율성을 더욱 높일 수 있습니다.

미국의 건설 펀치리스트 소프트웨어 시장은 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 7.1%를 보일 것으로 예측됩니다. 높은 건설 지출 수준과 디지털 프로젝트 관리 도구의 광범위한 채택으로 세계 최고의 위치를 유지하고 있습니다. 강력한 국내 기술 생태계가 지속적으로 작동하여 계약자에게 고급 소프트웨어 기능에 대한 조기 액세스를 제공합니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

미국-건축 기준법, OSHA 기준 및 디지털 건설 의무화

캐나다-국가 건축 기준(NBC) 및 주 디지털 건설 구상

유럽

독일-EU건설 제품 규칙(CPR)

영국-공공 프로젝트 BIM 레벨 2 의무화

프랑스-RE2020 건축 규제와 디지털 건설 컴플라이언스

이탈리아-국가 부흥·레지리엔스 계획(PNRR)

아시아태평양

중국-디지털 건설 정책과 스마트 시티 구상

인도-쿠니타치 BIM 도입 가이드라인 및 스마트 시티 구상

일본-i-Construction 구상(국토 교통성)

호주-내셔널 BIM 및 디지털 엔지니어링 프레임워크

LATAM

멕시코-내셔널 BIM 및 디지털 엔지니어링 프레임워크

아르헨티나-건축 규제와 공공 인프라 디지털화

중동 및 아프리카

남아프리카공화국-국가 건축 규제 및 디지털 컴플라이언스 요건

사우디아라비아-비전 2030 및 국가 변혁 프로그램

Porter의 Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

특허 분석

이용 사례와 성공 사례

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국에 관한 고려사항

구입자 채택과 구매 행동

기능적 특징 벤치마킹

통합과 상호운용성 상황

전망과 기회

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획과 자금조달

제5장 시장 추산·예측 : 구독 모델별, 2022-2035

월간

연간

원타임 라이선스

제6장 시장 추산·예측 : 도입 모델별, 2022-2035

On-Premise

클라우드 기반

제7장 시장 추산·예측 : 유형별, 2022-2035

웹 기반

모바일 앱

제8장 시장 추산·예측 : 프로젝트 규모별, 2022-2035

대규모 프로젝트

중소규모 프로젝트

제9장 시장 추산·예측 : 최종 용도별, 2022-2035

종합 건설 업자

하청 업자

플랜트 엔지니어링 계약업체

건축가 및 엔지니어

건물 소유자

기타

제10장 시장 추산·예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

베네룩스

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제11장 기업 개요

세계 기업

Autodesk

Citrix Systems

Deltek

Nemetschek

Oracle

PlanGrid

Procore Technologies

Trimble(Viewpoint)

지역 기업

Alpha Software

Buildertrend

eSUB Construction Software

Fieldwire

FINALCAD

Kahua

Newforma

Novade Solutions

SKYSITE

UDA Technologies

신기술 이노베이터

Connecteam

Iflexion

InEight

LetsBuild

OnSite Punchlist

Raken

Strata Systems

LSH

영문 목차

영문목차

The Global Construction Punch List Software Market was valued at USD 680.1 million in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 1.5 billion by 2035.

Market growth reflects the increasing reliance of construction teams on digital tools to streamline issue identification, tracking, and resolution during project completion phases. Punch list software supports real-time coordination across stakeholders throughout the construction lifecycle, improving transparency and accountability. Adoption remains strongest in regions with mature construction sectors and high digital readiness. North America continues to lead due to early technology uptake and a well-established software-as-a-service environment, while Europe follows closely, supported by rigorous quality and compliance standards. The industry is evolving rapidly as digital transformation reshapes how quality control and closeout workflows are managed. Artificial intelligence-driven analysis is enhancing accuracy and efficiency by supporting automated identification of project deficiencies, while mobile-first development strategies are improving on-site usability and responsiveness. Cloud-based deployment has become the preferred model, offering scalability, continuous updates, multi-device accessibility, and secure data management without the burden of on-site infrastructure.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$680.1 Million

Forecast Value

$1.5 Billion

CAGR

9.2%

The annual subscription models segment accounted for 53% share in 2025 and is projected to grow at a CAGR of 8.5% between 2026 and 2035. These plans provide predictable revenue streams for providers and simplify financial planning for construction firms by avoiding large upfront investments. Annual pricing structures are particularly appealing to contractors managing multiple projects simultaneously, as they balance cost efficiency with flexibility.

The cloud-based solutions represented 64% share in 2025 and are expected to grow at a CAGR of 9.7% through 2035. Cloud platforms enable seamless updates, scalable performance, and secure data storage while removing the need for dedicated hardware or internal IT resources. Shared infrastructure models further enhance efficiency while maintaining strong data protection standards.

U.S. Construction Punch List Software Market is forecast to grow at a CAGR of 7.1% from 2026 to 2035. The country maintains a leading global position due to high construction spending levels and widespread adoption of digital project management tools. A strong domestic technology ecosystem continues to provide contractors with early access to advanced software capabilities.

Key companies active in the Global Construction Punch List Software Market include Procore Technologies, Autodesk, Oracle, Trimble (Viewpoint), Buildertrend, Fieldwire, Deltek, Alpha Software, UDA Technologies, and Strata Systems. Companies operating in the Global Construction Punch List Software Market focus on strengthening their market position through product innovation, platform integration, and customer-centric development. Investment in artificial intelligence, automation, and analytics enhances software functionality and user value. Vendors prioritize cloud-native architectures to improve scalability and deployment speed while supporting remote collaboration. Strategic partnerships with construction firms and technology providers expand market reach and solution interoperability. Flexible pricing models and subscription offerings help attract a broader customer base.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.3 Research trail and confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Best estimates and calculations

1.6.1 Base year calculation for any one approach

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Subscription Model

2.2.3 Deployment Model

2.2.4 Type

2.2.5 Project Size

2.2.6 End Use

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Rising digital adoption in construction

3.2.1.3 Need for better team collaboration

3.2.1.4 Focus on quality and timely completion

3.2.1.5 Mobile and cloud-based accessibility

3.2.1.6 Growth in large construction projects

3.2.2 Industry pitfalls and challenges

3.2.2.1 High implementation costs

3.2.2.2 Resistance to digital adoption

3.2.3 Market opportunities

3.2.3.1 Adoption of AI and automation for defect detection

3.2.3.2 Expansion in emerging markets with growing construction activities

3.2.3.3 Integration with BIM and project management tools

3.2.3.4 Demand for mobile-first and cloud-based solutions

3.2.3.5 Offering analytics for predictive maintenance and project efficiency

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 US- Building codes, OSHA standards, and digital construction mandates

3.4.1.2 Canada - National building code (NBC) and provincial digital construction initiatives

3.4.2 Europe

3.4.2.1 Germany- EU construction products regulation (CPR)

3.4.2.2 UK- BIM Level 2 mandate for public projects

3.4.2.3 France- RE2020 building regulation and digital construction compliance

3.4.2.4 Italy- National Recovery and Resilience Plan (PNRR)

3.4.3 Asia Pacific

3.4.3.1 China- Digital construction policies and Smart City initiatives

3.4.3.2 India- National BIM adoption guidelines and Smart Cities Mission

3.4.3.3 Japan- i-Construction initiative (MLIT)

3.4.3.4 Australia- National BIM and digital engineering frameworks

3.4.4 LATAM

3.4.4.1 Mexico- National BIM and digital engineering frameworks

3.4.4.2 Argentina- Building regulations and public infrastructure digitization

3.4.5 MEA

3.4.5.1 South Africa- National building regulations and digital compliance requirements

3.4.5.2 Saudi Arabia- Vision 2030 and national transformation program