Trichlorosilane Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928953

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

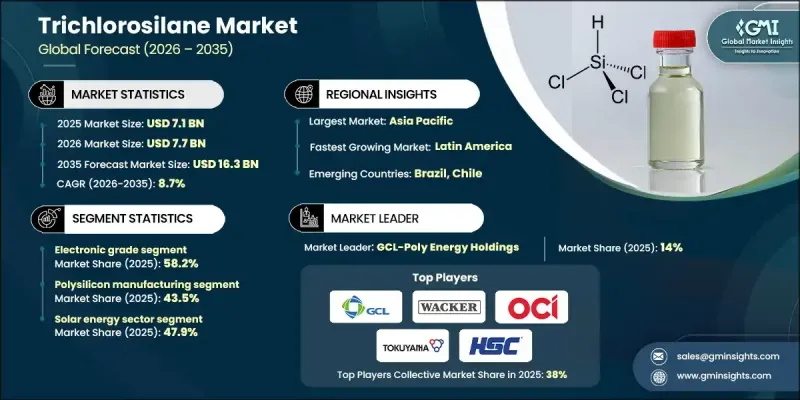

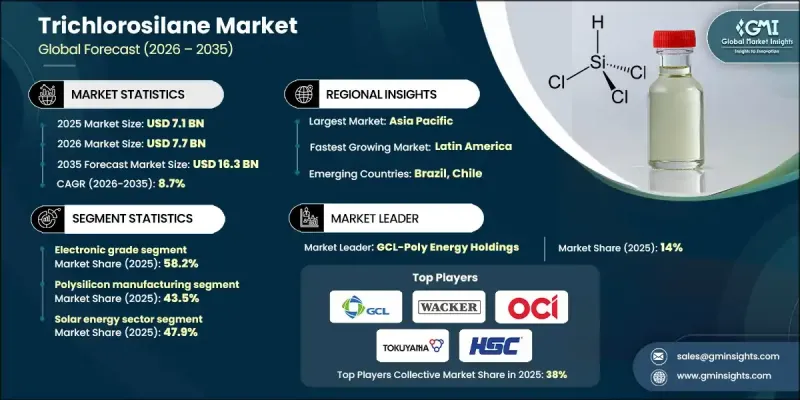

세계의 트리클로로실란 시장은 2025년에 71억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 8.7%로 성장하여 163억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경에는 전자기기, 태양광 발전, 그린 수소 기술에서 고순도 실리콘에 대한 의존도가 높아지는 것을 들 수 있습니다. 탄소중립과 청정에너지에 대한 전 세계적인 노력으로 태양광 발전의 도입이 가속화되고 있으며, 특히 아시아태평양에서는 주요 경제권의 정부 지원 정책이 현지 태양광 제조를 촉진하고 있습니다. 반도체 분야도 수요에 크게 기여하고 있으며, 인공지능, 전기자동차, 5G, IoT 디바이스 등 신기술에는 트리클로로실란 유래의 초순수 폴리실리콘이 필수적입니다. 기업들은 수요 증가에 대응하기 위해 고도화 공정에 대한 투자와 생산능력 확대를 추진하고 있습니다. 또한, 환경 규제와 생산 비용 절감의 필요성으로 인해 유동층 반응기(FBR) 기술 등 에너지 효율이 높은 공정으로의 전환이 진행되고 있습니다. 이 기술은 기존 방식에 비해 최대 80%의 에너지 소비를 절감할 수 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

71억 달러

예측 금액

163억 달러

CAGR

8.7%

전자 등급 TCS 부문은 2025년 58.2%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 8.9%의 성장률을 보일 것으로 예측됩니다. 이 부문의 선도적 지위는 반도체, 태양광 셀, 광섬유용 초순수 폴리실리콘 제조에 중요한 역할을 하고 있기 때문입니다. 첨단 전자기기에서 결함 없는 웨이퍼 및 칩 생산의 필요성으로 인해 순도 99.9999% 이상의 TCS에 대한 수요가 증가하고 있습니다. 저급 대체품은 고성능 반도체 용도에 필요한 엄격한 순도 요건을 충족시킬 수 없습니다.

태양광 에너지 분야는 2025년 47.9%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 8.6%를 나타낼 것으로 예측됩니다. 트리클로로실란은 결정질 실리콘 태양전지에 필수적인 태양전지 등급 폴리실리콘의 주요 원료입니다. 특히 태양광 발전 용량 확대를 목표로 하는 국가들의 탈탄소화 및 청정에너지 도입을 위한 전 세계적인 노력이 시장 성장을 지속적으로 견인하고 있습니다.

북미 트리클로로실란 시장은 2025년 25.9%의 점유율을 차지했습니다. 이 지역의 성장은 국내 반도체 및 태양전지 제조 생태계를 재구축하기 위한 정부 정책에 의해 뒷받침되고 있으며, 이는 트리클로로실란의 생산량 및 소비량 증가를 촉진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter의 Five Forces 분석

PESTEL 분석

가격 동향

지역별

등급별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)

(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획

제5장 시장 추산·예측 : 등급별, 2022-2035

전자 등급

산업용 등급

제6장 시장 추산·예측 : 용도별, 2022-2035

폴리실리콘 제조

시란가스 생산

실리콘 중간체

태양전지

광섬유

코팅 및 접착제

실험실용 시약

반도체 부품

제7장 시장 추산·예측 : 최종 용도별, 2022-2035

태양광 에너지 분야

태양광발전 셀 제조

태양전지판 제조

반도체 및 일렉트로닉스

IC제조

웨이퍼 및 칩 제조

MEMS 센서

LED 및 광검출기 제조

화학 처리

시란 및 실리콘 제조

특수화학 중간체

통신

광섬유 케이블 및 부품

유리 프리폼 제조

자동차·모빌리티

ADAS 및 EV용 실리콘 칩

실리콘 기술을 이용한 코팅과 센서

항공우주 및 방위

내열성 실리콘 부품

전자 실드 부품

건설 및 인프라

내후성 실란트

코팅·접착제

헬스케어 및 의료기기

의료용 실리콘 및 임플란트

진단용 센서 부품

제8장 시장 추산·예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트

기타 중동 및 아프리카

제9장 기업 개요

American Elements

Evonik Industries

GCL-Poly Energy Holdings

Gelest

Haihang Group

Hemlock Semiconductor Operations

Hubei Jianghan New Materials

Iota Corporation

Linde

OCI Company Ltd.

REC Silicon

Shin-Etsu Chemical

Siad

Tokuyama Corporation

Wacker Chemie

Others

LSH

영문 목차

영문목차

The Global Trichlorosilane Market was valued at USD 7.1 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 16.3 billion by 2035.

Market expansion is driven by the increasing reliance on high-purity silicon for electronics, solar energy, and green hydrogen technologies. The global push toward carbon neutrality and clean energy has accelerated solar PV adoption, particularly in Asia-Pacific region, where supportive government policies in major economies have incentivized local solar manufacturing. The semiconductor sector is also contributing significantly to demand, with emerging technologies like artificial intelligence, electric vehicles, 5G, and Internet of Things devices requiring ultra-high-purity polysilicon derived from TCS. Companies are responding with investments in advanced purification processes and expanded production capacities to meet rising demand. Additionally, environmental regulations and the need to lower production costs are prompting a shift toward energy-efficient processes such as Fluidized Bed Reactor (FBR) technology, which reduces energy consumption by up to 80% compared to conventional methods.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$7.1 Billion

Forecast Value

$16.3 Billion

CAGR

8.7%

The electronic-grade TCS segment held 58.2% share in 2025 and is expected to grow at a CAGR of 8.9% through 2035. The segment's leadership stems from its critical role in producing ultra-pure polysilicon for semiconductors, solar PV cells, and fiber optics. Demand for 99.9999%+ purity TCS is rising due to the requirement for defect-free wafer and chip production in advanced electronics. Lower-grade alternatives fail to meet the stringent purity needed for high-performance semiconductor applications.

The solar energy sector accounted for 47.9% share in 2025 and is projected to grow at a CAGR of 8.6% through 2035. TCS serves as a primary feedstock for solar-grade polysilicon, essential for crystalline silicon PV cells. Global efforts toward decarbonization and clean energy adoption, particularly in nations aiming to expand solar PV capacity, continue to drive market growth.

North America Trichlorosilane Market held 25.9% in 2025. Growth in the region is supported by government initiatives designed to rebuild domestic semiconductor and solar manufacturing ecosystems, spurring higher production and consumption of TCS.

Leading players in the Global Trichlorosilane Market include American Elements, Evonik Industries, Tokuyama Corporation, OCI Company Ltd., REC Silicon, Wacker Chemie, Shin-Etsu Chemical, Linde, Gelest, GCL-Poly Energy Holdings, Haihang Group, Hemlock Semiconductor Operations, Hubei Jianghan New Materials, Iota Corporation, and Siad. Companies in the Global Trichlorosilane Market are pursuing several strategies to strengthen their foothold. Investments in advanced purification and production technologies enhance product quality and capacity. Strategic partnerships and joint ventures expand market access and secure supply chains for high-purity silicon. Firms are also focusing on sustainability by adopting energy-efficient manufacturing methods to meet environmental regulations. Expanding into emerging regions with high solar and semiconductor growth helps capture new customer bases.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Grade

2.2.3 Application

2.2.4 End use

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter';s analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By grade

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Grade, 2022-2035 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Electronic Grade

5.3 Industrial Grade

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Polysilicon Manufacturing

6.3 Silane Gas Production

6.4 Silicone Intermediate

6.5 Photovoltaic Cells

6.6 Optical Fibers

6.7 Coatings and Adhesives

6.8 Laboratory Reagents

6.9 Semiconductor Components

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Solar Energy Sector

7.2.1 Photovoltaic cell production

7.2.2 Solar panel manufacturing

7.3 Semiconductor & Electronics

7.3.1 IC manufacturing

7.3.2 Wafer and chip fabrication

7.3.3 MEMS sensors

7.3.4 LED & photodetector fabrication

7.4 Chemical Processing

7.4.1 Silane and silicone production

7.4.2 Specialty chemical intermediates

7.5 Telecommunications

7.5.1 Optical fiber cables and components

7.5.2 Glass preform production

7.6 Automotive & Mobility

7.6.1 Silicon chips for ADAS and EVs

7.6.2 Coatings and sensors using silicon tech

7.7 Aerospace & Defense

7.7.1 High-temperature resistant silicone parts

7.7.2 Electronic shielding components

7.8 Construction & Infrastructure

7.8.1 Weather-resistant sealants

7.8.2 Coatings & adhesives

7.9 Healthcare & Medical Devices

7.9.1 Medical-grade silicones and implants

7.9.2 Diagnostic sensor components

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)