Aluminum Pigments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928925

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

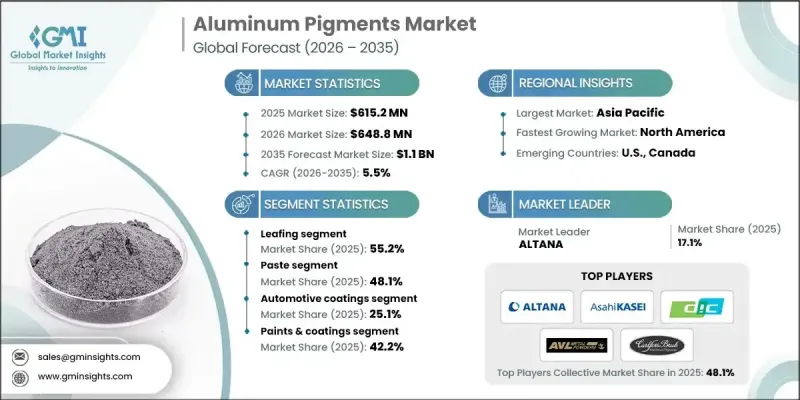

세계의 알루미늄 안료 시장은 2025년에 6억 1,520만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.5%로 성장하여 11억 달러에 이를 것으로 예측되고 있습니다.

자동차, 포장, 화장품, 페인트 및 코팅 등의 분야에서 수요가 증가하면서 시장이 확대되고 있습니다. 알루미늄 안료는 금속 광택과 반사 특성으로 높은 평가를 받고 있으며, 시각적 매력을 높일 뿐만 아니라 최종 제품의 기능적 성능도 향상시킵니다. 거울 표면을 구현하고, 내구성을 높이고, 내식성을 향상시키며, 열 안정성을 강화합니다. 이 안료는 높은 불투명도, 밝기, 금속 효과를 제공하므로 장식용 및 기능성 코팅에 이상적입니다. 반사 능력은 열 흡수를 줄여 에너지 효율에도 기여합니다. 화학적 안정성과 환경 내성 또한 완제품의 수명을 더욱 연장시킵니다. 자동차 코팅 및 고급 퍼스널케어 제품에서의 사용 증가는 다양한 산업 분야에서 고품질 마감재에 대한 수요를 뒷받침하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

6억 1,520만 달러

예측 금액

11억 달러

CAGR

5.5%

리프팅 알루미늄 안료 부문은 2025년에 55.2%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 5.6%의 성장률을 보일 것으로 예측됩니다. 이 부문은 초박형 반사층을 형성하고 고도의 금속성 광택 표면을 생성하는 능력으로 인해 주목을 받고 있습니다. 이러한 특성으로 인해 리프팅 안료는 자동차 및 장식용 고급 코팅에 우선적으로 선택되고 있습니다.

제품 형태별로는 페이스트형 알루미늄 안료 부문이 2025년 48.1%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 5.6%의 성장률을 보일 것으로 예측됩니다. 페이스트 안료는 우수한 분산성, 균일한 분포, 쉬운 혼화성을 제공하기 때문에 산업용도료, 자동차 도료, 장식용 도료에 널리 사용되고 있습니다. 이러한 특성은 매끄럽고 반사율이 높은 표면을 보장하며, 제조업체는 제품의 시각적 매력과 내구성을 모두 향상시킬 수 있습니다.

북미 알루미늄 안료 시장은 2025년 26.1%의 점유율을 차지하며 견조한 성장세를 이어갈 것으로 예측됩니다. 이 지역 수요는 자동차, 도료, 포장 분야가 주도하고 있습니다. 지속가능성과 환경 친화적 인 노력이 생산에 영향을 미치면서 제조업체는 저 VOC 및 수성 배합에 초점을 맞추었습니다. 자동차 분야는 여전히 주요 분야이며, 소비자와 제조업체는 제품 미관을 향상시키기 위해 고광택 및 반사성 마감을 요구하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter의 Five Forces 분석

PESTEL 분석

가격 동향

지역별

유형별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획

제5장 시장 추산·예측 : 유형별, 2022-2035

리핑

비리핑

제6장 시장 추산·예측 : 형태별, 2022-2035

페이스트

분말

펠릿

기타(플레이크 등)

제7장 시장 추산·예측 : 용도별, 2022-2035

자동차용 페인트

산업용 페인트

건축용·장식용 페인트

그라비어 인쇄 용잉크

프렉소 인쇄용 잉크

산업용 플라스틱

네일 제품

페이스메이크압

헤어케어 제품

기타

제8장 시장 추산·예측 : 최종 이용 산업별, 2022-2035

페인트 및 코팅

인쇄 잉크

플라스틱

퍼스널케어 및 화장품

기타(건설, 전자기기 등)

제9장 시장 추산·예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트

기타 중동 및 아프리카

제10장 기업 개요

ALTANA

Asahi Kasei

AVL METAL POWDERS n.v.

Carlfors Bruk

DIC CORPORATION

Kolortek Co., Ltd.

Metaflake Ltd

SCHLENK SE

Shan Dong Jie Han Metal Material Co., Ltd

TOYO ALUMINIUM K.K.

Zhangqiu metallic pigment co.,ltd.

ZuXing New Materials Co., Ltd.

LSH

영문 목차

영문목차

The Global Aluminum Pigments Market was valued at USD 615.2 million in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 1.1 billion by 2035.

The market is expanding due to rising demand across sectors such as automotive, packaging, cosmetics, and paints & coatings. Aluminum pigments are prized for their metallic sheen and reflective properties, which not only enhance visual appeal but also improve functional performance in end-use products. They deliver a mirror-like finish, increase durability, boost corrosion resistance, and enhance thermal stability. These pigments offer high opacity, brightness, and metallic effects, making them ideal for decorative and functional coatings. Their reflective capabilities also contribute to energy efficiency by reducing heat absorption. Chemical stability and environmental resilience further add to the longevity of finished products. Increasing use in automotive coatings and luxury personal care items continues to drive adoption, supported by demand for high-quality finishes in various industries.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$615.2 Million

Forecast Value

$1.1 Billion

CAGR

5.5%

The leafing aluminum pigments segment held 55.2% share in 2025 and is projected to grow at a CAGR of 5.6% through 2035. This segment is gaining traction due to its ability to form ultra-thin reflective layers, producing highly metallic and glossy surfaces. Such properties make leafing pigments a preferred choice for premium coatings in automotive and decorative applications.

In terms of product form, the paste aluminum pigments segment held 48.1% share in 2025 and is expected to grow at a CAGR of 5.6% between 2026 and 2035. Paste pigments are widely used in industrial coatings, automotive finishes, and decorative paints because they provide excellent dispersibility, uniform distribution, and easy blending. These features ensure smooth, reflective surfaces and enable manufacturers to enhance both the visual appeal and durability of their products.

North America Aluminum Pigments Market accounted for 26.1% share in 2025 and continues to exhibit strong growth. The region's demand is driven by applications in automotive, coatings, and packaging sectors. Sustainability and eco-friendly practices are increasingly influencing production, leading manufacturers to focus on low-VOC and water-based formulations. Automotive remains a key sector, with consumers and manufacturers seeking high-gloss and reflective finishes to elevate product aesthetics.

Key players in the Global Aluminum Pigments Market include Metaflake Ltd, DIC CORPORATION, ALTANA, Asahi Kasei, SCHLENK SE, Carlfors Bruk, TOYO ALUMINIUM K.K., Zhangqiu Metallic Pigment Co., Ltd., ZuXing New Materials Co., Ltd., Kolortek Co., Ltd., and AVL METAL POWDERS n.v. Market participants are adopting several strategies to strengthen their presence and expand market share. Companies are investing in advanced manufacturing technologies and eco-friendly processes to meet sustainability requirements. They are increasing production capacities, enhancing R&D for high-performance pigments, and diversifying product portfolios. Strategic collaborations, partnerships, and regional expansions allow firms to access new markets and serve emerging applications. Focus on product innovation, quality improvement, and operational efficiency further solidifies the market position and ensures long-term competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Form

2.2.4 Application

2.2.5 End use industry

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter';s analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Million) (Kilo Tons)

5.1 Key trends

5.2 Leafing

5.3 Non-leafing

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

6.1 Key trends

6.2 Paste

6.3 Powder

6.4 Pellets

6.5 Others (flakes, etc)

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

7.1 Key trends

7.2 Automotive coatings

7.3 Industrial coatings

7.4 Architectural/decorative coatings

7.5 Gravure inks

7.6 Flexographic inks

7.7 Industrial plastic

7.8 Nail products

7.9 Face makeup

7.10 Hair care products

7.11 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Million) (Kilo Tons)

8.1 Key trends

8.2 Paints & coatings

8.3 Printing inks

8.4 Plastics

8.5 Personal care & cosmetics

8.6 Others (construction, electronics, etc)

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)