Barite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928923

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

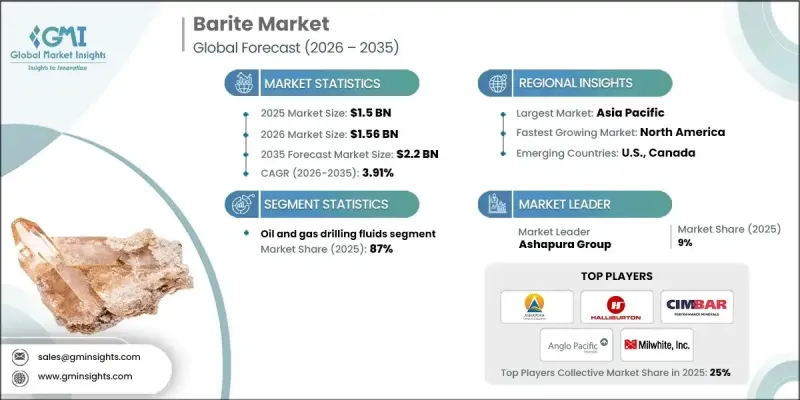

세계의 중정석 시장은 2025년에 15억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.91%로 성장하여 22억 달러에 이를 것으로 예측됩니다.

시장 성장은 개발도상국의 인프라 개발 및 건설 활동 증가로 인해 중정석의 소비 범위가 기존 용도를 넘어서는 범위로 확대되고 있습니다. 아시아태평양, 라틴아메리카 및 중동의 대규모 인프라 및 산업 프로젝트에 대한 투자 증가는 고밀도 건설 솔루션 및 특수 산업 응용 분야에 사용되는 중정석 기반 재료에 대한 수요 증가에 기여하고 있습니다. 동시에 환경 규제 요건과 지속가능성 목표가 업계 내 채굴 및 가공 관행을 재구성하고 있습니다. 미국의 규제 프레임워크는 폐수 관리, 배출 규제, 공정 최적화 등 중정석 생산업체에 엄격한 운영 기준을 부과하고 있습니다. 비에너지 분야로의 다각화에도 불구하고 석유 및 가스 산업은 여전히 세계 중정석 사용량의 대부분을 차지하며 수요의 주요 견인차 역할을 하고 있습니다. 이 광물은 천연의 고밀도를 가지고 있기 때문에 시추 작업의 압력 균형 유지, 작업 안전성 향상, 효율성 확보에 필수적입니다. 이러한 복합적인 요인들이 세계 중정석 시장공급 전략, 가격 변동, 장기적인 투자 판단에 영향을 미치고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

15억 달러

예측 금액

22억 달러

CAGR

3.91%

중정석 등급은 비중 기준에 따라 구분되며, API 4.1 등급은 2010년 도입 이후 시추 유체 분야에서 가장 널리 사용되는 사양으로 자리 잡았습니다. API 4.2 등급은 최저 밀도 4.20 g/mL의 고순도 옵션으로, API 표준을 준수할 필요가 없는 상황에서는 서브 API 등급이 활용됩니다. 특수 고밀도 중정석은 최대 수준의 재료 중량과 성능이 요구되는 용도에만 사용됩니다.

석유 및 가스 시추 유체 분야는 2025년 87%의 점유율을 차지했습니다. 이러한 응용 분야에서 중정석은 유체 밀도를 증가시켜 지하 압력을 관리하고, 유정 안정성을 유지하며, 운영 위험을 줄이고, 시추 활동 중 시추 잔여물을 제거하는 데 도움을 주는 가중재 역할을 합니다.

아시아태평양의 중정석 시장은 2025년 45.1%의 점유율을 차지했습니다. 이는 이 지역의 견조한 생산과 소비에 힘입은 것입니다. 중국은 세계 최대 생산국임과 동시에 2024년 생산량이 약 210만 톤에 달하는 등 국내 수요도 꾸준히 증가하고 있습니다. 인도는 주요 공급국으로서의 역할을 지속적으로 강화하고 있으며, 같은 해 생산량은 약 260만 톤으로 증가했습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter의 Five Forces 분석

PESTEL 분석

가격 동향

지역별

형태별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국에 관한 고려사항

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

확대 계획

제5장 중정석 시장 : 비중 등급별, 2022-2035

API 등급 4.2

API 등급 4.1

서브 API 등급(비중 3.9-4.0)

기타

제6장 중정석 시장 : 형태별, 2022-2035

덩어리진 상태

분말

제7장 중정석 시장 : 용도별, 2022-2035

석유 및 가스 시추액

바륨 화학제품

페인트 및 코팅

고무 및 플라스틱

의약품

유리 및 세라믹

방사선 차폐

마찰 제품

기타

제8장 중정석 시장 : 최종 이용 산업별, 2022-2035

석유 및 가스 산업

건설 업계

의료 업계

자동차 산업

화학 제조

페인트 및 코팅 제조

기타

제9장 시장 규모와 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

기타 중동 및 아프리카

제10장 기업 개요

Spectrum Chemical Manufacturing

Deutsche Baryt Industrie

Halliburton

New Riverside Ochre

Albar Industrial Minerals

Excalibar Minerals

Anglo Pacific Minerals

SCR-Sibelco

Ashapura Group

Barium &Chemicals

CIMBAR Performance Minerals

Milwhite

Mil-Spec Industries

International Earth Products

LSH

영문 목차

영문목차

The Global Barite Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 3.91% to reach USD 2.2 billion by 2035.

Market growth is supported by rising infrastructure development and construction activity across developing regions, which is broadening the scope of barite consumption beyond its conventional uses. Increasing investments in large-scale infrastructure and industrial projects across the Asia Pacific, Latin America, and the Middle East are contributing to higher demand for barite-based materials used in high-density construction solutions and specialized industrial applications. At the same time, environmental compliance requirements and sustainability goals are reshaping mining and processing practices within the industry. Regulatory frameworks in the United States impose strict operational standards on barite producers, including wastewater management, discharge control, and process optimization. Despite diversification into non-energy sectors, the oil and gas industry continues to be the primary driver of demand, accounting for the majority of global barite usage. The mineral's naturally high density makes it essential for maintaining pressure balance, enhancing operational safety, and supporting efficiency during drilling activities. These combined factors continue to influence supply strategies, pricing dynamics, and long-term investment decisions across the global barite market.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.5 Billion

Forecast Value

$2.2 Billion

CAGR

3.91%

Barite grades are segmented based on specific gravity standards, with API Grade 4.1 emerging as the most widely used specification in drilling fluid applications since its introduction in 2010. API Grade 4.2 remains a higher-purity option with a minimum density of 4.20 g/mL, while sub-API grades are utilized where compliance with API specifications is not required. Specialty high-density barite is reserved for applications that demand maximum material weight and performance.

The oil & gas drilling fluids segment accounted for 87% share in 2025. In these applications, barite acts as a weighting material that increases fluid density to manage subsurface pressure, support wellbore stability, reduce operational risk, and assist in the removal of drilling debris during extraction activities.

Asia Pacific Barite Market held a 45.1% share in 2025, supported by strong regional production and consumption. China remains the largest global producer while also maintaining substantial domestic demand, with output reaching nearly 2.1 million metric tons in 2024. India continues to strengthen its role as a key supplier, with production volumes increasing to approximately 2.6 million metric tons during the same year.

Key companies active in the Global Barite Market include Halliburton, Ashapura Group, SCR-Sibelco, CIMBAR Performance Minerals, Deutsche Baryt Industrie, Milwhite, Spectrum Chemical Manufacturing, Excalibar Minerals, Anglo Pacific Minerals, Barium & Chemicals, Albar Industrial Minerals, Mil-Spec Industries, New Riverside Ochre, and International Earth Products. Companies operating in the Global Barite Market are adopting a range of strategies to reinforce their market position and expand global reach. These include capacity expansion initiatives, modernization of mining and processing facilities, and investment in environmentally compliant production methods. Firms are prioritizing long-term supply agreements with end-use industries, particularly in energy and infrastructure sectors, to ensure demand stability. Strategic acquisitions, partnerships, and geographic diversification are also being pursued to strengthen distribution networks. Additionally, companies are focusing on quality optimization, cost control, and regulatory compliance to maintain competitiveness while meeting evolving industry standards and sustainability expectations.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Specific gravity grade

2.2.2 Form

2.2.3 Application

2.2.4 End Use industry

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter';s analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By form

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Barite Market, By Specific Gravity Grade, 2022-2035 (USD Billion, Kilo Tons)

5.1 Key trends

5.2 API grade 4.2

5.3 API grade 4.1

5.4 Sub-API grade (3.9-4.0 sg)

5.5 Others

Chapter 6 Barite Market, By Form, 2022-2035 (USD Billion, Kilo Tons)

6.1 Key trends

6.2 Lumps

6.3 Powder

Chapter 7 Barite Market, By Application, 2022-2035 (USD Billion, Kilo Tons)

7.1 Key trends

7.2 Oil & gas drilling fluids

7.3 Barium chemicals

7.4 Paints & coatings

7.5 Rubber & plastics

7.6 Pharmaceuticals

7.7 Glass & ceramics

7.8 Radiation shielding

7.9 Friction products

7.10 Others

Chapter 8 Barite Market, By End Use Industry, 2022-2035 (USD Billion, Kilo Tons)

8.1 Key trends

8.2 Oil & gas industry

8.3 Construction industry

8.4 Healthcare industry

8.5 Automotive industry

8.6 Chemical manufacturing

8.7 Paints & coatings manufacturing

8.8 Others

Chapter 9 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)