Forestry Lubricants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928919

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

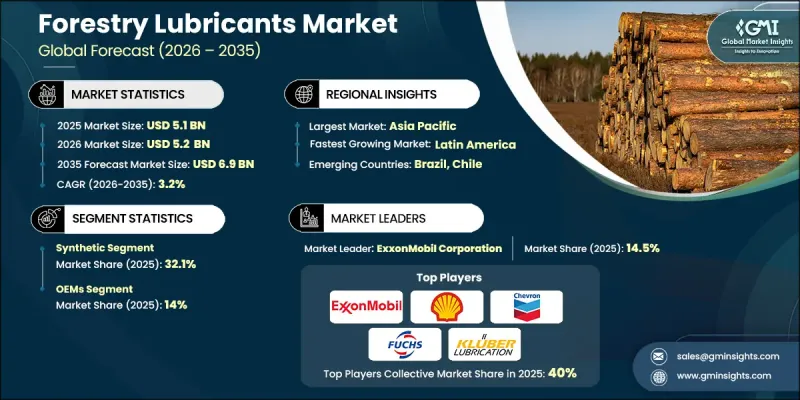

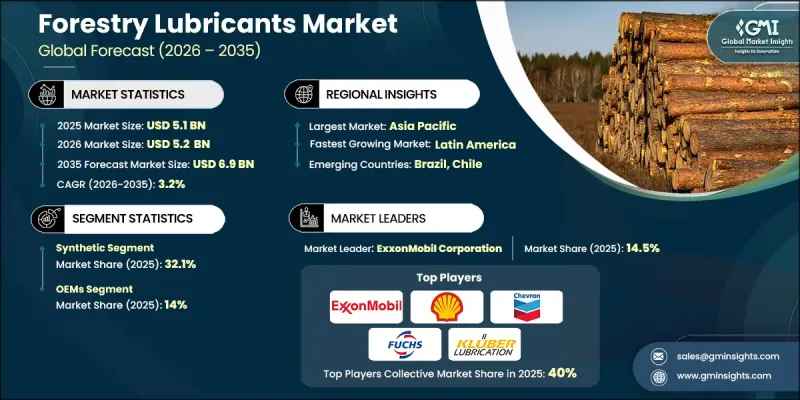

세계의 임업용 윤활유 시장은 2025년에 51억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 3.2%로 성장하여 69억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경에는 임업 작업 전반에 걸쳐 고도로 기계화된 첨단 장비의 도입이 증가하고 있다는 점을 들 수 있습니다. 이러한 장비는 가혹한 조건에서도 신뢰할 수 있는 성능을 보장하기 위해 특수 윤활유가 필요합니다. 임업기계는 원격지에서 가동되는 경우가 많기 때문에 예기치 못한 설비 가동 중단으로 인한 경제적 손실이 발생하기 때문에 수명 연장과 마모 방지 성능 향상을 실현하는 고품질 윤활유 채택을 촉진하고 있습니다. 운영자는 극한 기후 지역에서 자주 발생하는 가혹한 기계적 스트레스, 고온 환경, 높은 습도에 대한 노출을 견딜 수 있는 솔루션을 항상 찾고 있습니다. 규제 프레임워크도 시장 수요를 형성하고 있으며, 특히 친환경 윤활유 사용을 촉진하는 정책을 통해 영향을 미치고 있습니다. 이러한 규제는 상업적 보급을 지원하는 동시에 지속 가능한 산업의 고용 확대에도 기여할 것으로 기대됩니다. 이러한 윤활유에 대한 수요는 규정 준수 요구 사항과 높아지는 환경 인식에 의해 주도되고 있습니다. 재생 가능한 원료 함량이 높은 제품이 주목을 받고 있으며, 지속 가능한 재료 및 생산 방식으로의 광범위한 전환과 일치하여 장기적인 시장 모멘텀을 강화하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 가치

51억 달러

예측 금액

69억 달러

CAGR

3.2%

합성 윤활유 부문은 2025년 32.1%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 3.3%의 성장률을 보일 것으로 예측됩니다. 이러한 선도적인 위치는 장비가 지속적인 스트레스, 오염, 장시간 가동 사이클에 노출되는 가혹한 임업 환경에서의 우수한 성능에 기인합니다. 기존 대체품에 비해 열분해 및 산화에 대한 내성이 강화되어 임업 작업 전반에 걸쳐 채택이 가속화되고 있습니다.

OEM 부문은 2025년 14%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 3.2%로 성장할 것으로 전망됩니다. 주요 벌목 활동에 사용되는 여러 기계 시스템의 높은 윤활유 소비가 이 부문 수요를 주도하고 있습니다. 임업 작업은 열악한 환경에서 중요한 기계 및 유압 시스템의 기능을 유지하기 위해 신뢰할 수 있는 윤활에 크게 의존하고 있습니다.

북미 임업용 윤활유 시장은 2025년 31%의 점유율을 차지했습니다. 고도의 기계화 수준, 첨단 윤활유 배합의 보급, 환경 규제가 지역 수요를 뒷받침하고 있습니다. 기후 조건과 장비 제조업체 및 윤활유 공급업체와의 긴밀한 협력은 기계 수명 연장과 운영 효율성 향상에 더욱 기여하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter의 Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획

제5장 시장 추산·예측 : 제품별, 2022-2035

합성유

합성유 블렌드

바이오

광유

제6장 시장 추산·예측 : 용도별, 2022-2035

엔진 윤활유

변속기·기어 오일

유압작동유

그리스

핀·부싱용 그리스

베어링 그리스

체인 오일/톱가이드 오일

제지 기계용 오일

순환유

특수 제지 기계용 오일

압축기 오일

쿨란트/부동액

기타

슬라이드 웨이용 오일

방청 제

오픈 기어 윤활유

제7장 시장 추산·예측 : 최종 용도별, 2022-2035

OEM

제재소

종이 및 판지 공장

목재 제품 제조 시설

벌채·수확 회사

바이오매스 펠릿 공장

펄프 공장

삼림 계약업체/오퍼레이터

목재 운송 서비스

기타

제8장 시장 추산·예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트

기타 중동 및 아프리카

제9장 기업 개요

Amsoil Inc.

Bioblend Renewable Resources

BP plc(Castrol)

Chevron Corporation

China Petroleum &Chemical Corporation(Sinopec Corp)

Elba Lubrication Inc.

Exxon Mobil Corporation

Frontier Performance Lubricants

Fuchs Petrolub SE

Klondike Lubricants Corporation

Kluber Lubrication

Lubrizol Corporation

Pennine Lubricants

Petro-Canada Lubricants

Petronas Lubricants International(PLI)

Phillips 66 Company

Repsol S.A.

Rymax Lubricants

Shell plc

TotalEnergies SE

Others

LSH

영문 목차

영문목차

The Global Forestry Lubricants Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 3.2% to reach USD 6.9 billion by 2035.

Market expansion is supported by the increasing deployment of advanced, highly mechanized equipment across forestry operations, which requires specialized lubricants to ensure reliable performance under demanding conditions. As forestry machinery is often operated in remote locations, the financial impact of unplanned equipment stoppages has encouraged the use of premium lubricant formulations that offer extended service life and improved wear protection. Operators consistently seek solutions that can withstand heavy mechanical stress, elevated operating temperatures, and high moisture exposure commonly encountered in extreme climatic regions. Regulatory frameworks are also shaping market demand, particularly through policies promoting the use of environmentally acceptable lubricants. These regulations are expected to support commercial adoption while contributing to employment growth within sustainable industries. Demand for such lubricants is being driven by compliance requirements and growing environmental awareness. Products with high renewable content are gaining traction, aligning with broader shifts toward sustainable materials and production practices, which is reinforcing long-term market momentum.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$5.1 Billion

Forecast Value

$6.9 Billion

CAGR

3.2%

The synthetic lubricants segment accounted for 32.1% share in 2025 and is expected to grow at a CAGR of 3.3% through 2035. Their leading position is attributed to superior performance in harsh forestry environments, where equipment is exposed to continuous stress, contamination, and extended operating cycles. Enhanced resistance to thermal breakdown and oxidation compared to conventional alternatives has accelerated adoption across forestry operations.

The OEM segment held 14% share in 2025 and is forecast to grow at a CAGR of 3.2% between 2026 and 2035. High lubricant consumption across multiple machinery systems used in core harvesting activities is driving demand in this segment. Forestry operations depend heavily on reliable lubrication to maintain the uninterrupted functionality of essential mechanical and hydraulic systems in challenging environments.

North America Forestry Lubricants Market accounted for 31% share in 2025. High levels of mechanization, widespread use of advanced lubricant formulations, and environmental regulations are supporting regional demand. Climatic conditions and close collaboration between equipment manufacturers and lubricant suppliers further contribute to extended machinery life and operational efficiency.

Key companies operating in the Global Forestry Lubricants Market include Shell plc, Exxon Mobil Corporation, BP plc (Castrol), TotalEnergies SE, Fuchs Petrolub SE, Chevron Corporation, Petro-Canada Lubricants, Amsoil Inc., Lubrizol Corporation, Phillips 66 Company, Kluber Lubrication, Petronas Lubricants International (PLI), Repsol S.A., Sinopec Corp, Rymax Lubricants, Klondike Lubricants Corporation, Frontier Performance Lubricants, Bioblend Renewable Resources, Pennine Lubricants, and Elba Lubrication Inc. Companies operating in the Global Forestry Lubricants Market are strengthening their market positions through aggressive technology development, pilot programs, and ecosystem partnerships. Many players are investing in artificial intelligence, autonomous navigation, and fleet optimization software to improve reliability and scalability. Strategic collaborations with retailers, logistics firms, and municipalities help accelerate deployment and regulatory acceptance.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Application

2.2.4 End use

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter';s analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By Product

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Synthetic

5.3 Synthetic blend oil

5.4 Bio-based

5.5 Mineral

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Engine Lubrication

6.3 Transmission & Gear Oils

6.4 Hydraulic Fluids

6.5 Greases

6.5.1 Pin & Bushing Greases

6.5.2 Bearing Greases

6.6 Chain Oils / Saw Guide Oils

6.7 Paper Machine Oils

6.7.1 Circulating Oils

6.7.2 Specialty Paper Machine Oils

6.8 Compressor Oils

6.9 Coolants / Antifreeze

6.10 Others

6.10.1 Slideway Oils

6.10.2 Rust Preventives

6.10.3 Open Gear Lubricants

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 OEMs

7.3 Sawmills

7.4 Paper & Paperboard Mills

7.5 Wood Products Manufacturing Units

7.6 Logging / Harvesting Companies

7.7 Biomass Pellet Mills

7.8 Pulp Mills

7.9 Forest Contractors / Operators

7.10 Timber Transport Services

7.11 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 UK

8.3.3 France

8.3.4 Spain

8.3.5 Italy

8.3.6 Rest of Europe

8.4 Asia Pacific

8.4.1 China

8.4.2 India

8.4.3 Japan

8.4.4 Australia

8.4.5 South Korea

8.4.6 Rest of Asia Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.5.4 Rest of Latin America

8.6 Middle East and Africa

8.6.1 Saudi Arabia

8.6.2 South Africa

8.6.3 UAE

8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

9.1 Amsoil Inc.

9.2 Bioblend Renewable Resources

9.3 BP plc (Castrol)

9.4 Chevron Corporation

9.5 China Petroleum & Chemical Corporation (Sinopec Corp)