콜라겐 케이싱 시장의 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2026-2035년)

Collagen Casings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1928878

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

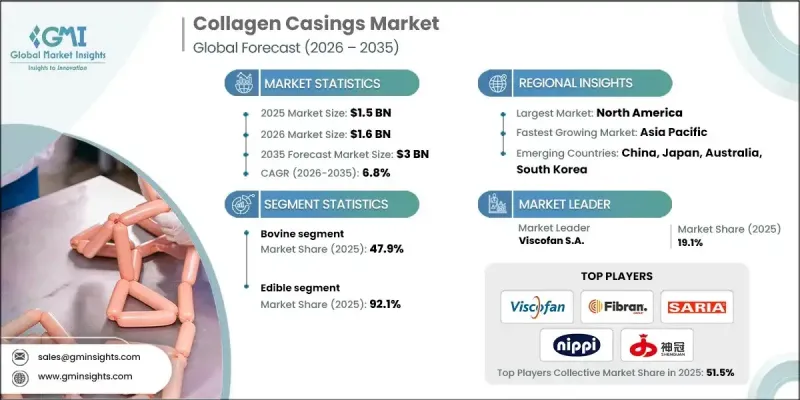

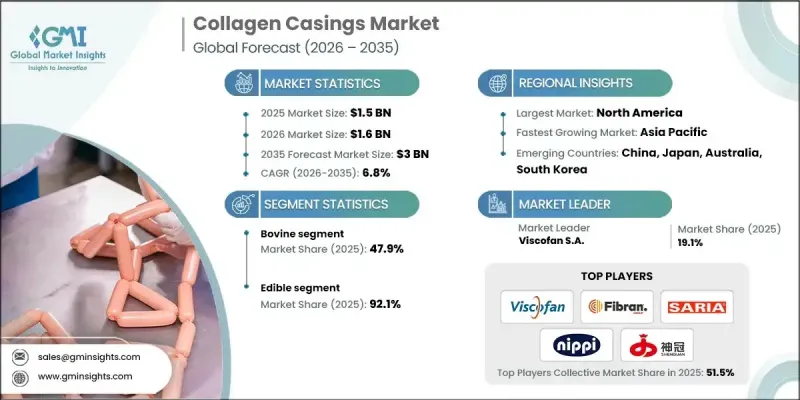

세계의 콜라겐 케이싱 시장은 2025년에 15억 달러로 평가되었으며, 2035년까지 CAGR 6.8%로 성장하여 30억 달러에 달할 것으로 예측됩니다.

콜라겐 케이싱은 소 또는 돼지 유래 콜라겐으로 제조된 식용 가능한 고단백 소시지 케이싱으로, 동물의 장에서 추출한 기존 케이싱을 대체할 수 있는 자연스럽고 지속가능한 대안을 제시합니다. 주로 소가죽으로 생산되며, 균일성, 편리성, 고속 자동화 기계와의 호환성으로 인해 소시지 생산에 널리 채택되어 육류 가공업체의 업무 효율을 크게 향상시킵니다. 전 세계 육류 소비가 꾸준히 증가함에 따라 천연 소재 대체품에 비해 확장성과 비용 효율적인 솔루션을 제공하는 콜라겐 케이싱에 대한 수요가 증가하고 있습니다. 유엔식량농업기구(FAO)에 따르면, 세계 육류 생산량은 2023년 약 3억 6,400만 톤에 달할 것으로 예상되며, 특히 신흥시장에서 지속적인 성장이 예상됩니다. 콜라겐 케이싱은 일관된 직경을 유지하고, 제조 공정의 하중을 견딜 수 있으며, 엄격한 식품 안전 규정을 충족하면서 오염 위험을 줄일 수 있다는 점에서 높은 평가를 받고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035

개시시 가치

15억 달러

예측 금액

30억 달러

CAGR

6.8%

소 콜라겐 부문은 2025년 47.9%의 점유율을 차지했으며, 2035년까지 연평균 6.6%의 성장률을 기록할 것으로 예측됩니다. 강도, 안정성, 자동화 생산 라인에 대한 완벽한 통합성으로 인해 주요 소시지 가공업체들이 선호하는 제품입니다. 소고기 산업으로부터의 공급이 보장되기 때문에 비용 효율적인 조달과 신뢰할 수 있는 성능을 실현하고 있습니다.

식용 콜라겐 케이싱 부문은 2025년 92.1%의 점유율을 차지했습니다. 생, 가열처리, 훈제 가공된 식용 케이싱은 대량 생산되는 소시지 제조에 널리 사용되고 있습니다. 소비 시 제품 부착 상태를 유지하는 특성, 균일한 크기, 자동 충전 시스템과의 호환성으로 인해 전 세계 모든 규모의 육류 가공업체에게 최적의 선택이 되고 있습니다.

북미 콜라겐 케이싱 시장은 2025년 4억 4,620만 달러를 기록했으며, 2026년부터 2035년까지 연평균 6.6%의 성장률을 보일 것으로 전망됩니다. 자연 유래, 클린 라벨, 알레르겐 프리 식품에 대한 소비자 수요가 증가함에 따라 육가공품, 레토르트 식품, 스낵에 콜라겐 케이싱을 적용하는 사례가 늘고 있습니다. 기업들은 건강, 투명성, 제품 품질에 대한 소비자의 기대에 부응하기 위해 지속가능한 조달과 환경 친화적인 제조 공정에 점점 더 집중하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계의 부가가치

밸류체인에 영향을 미치는 요인

디스럽션

업계에 대한 영향요인

성장 촉진요인

세계의 육류 소비량과 가공량 증가

천연 케이싱에 대한 우위성

지속가능성과 순환경제 동향

업계의 잠재적 리스크와 과제

원재료 가격 변동성

대체 케이싱 제품과의 경쟁 상황

시장 기회

태너리 폐기물의 유효 활용

프리미엄 인증 시장

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porters 분석

PESTEL 분석

가격 동향

지역별

소스별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS 코드)(참고 : 무역 통계는 주요국에 대해서만 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 실천

폐기물 절감 전략

생산의 에너지 효율

친환경적인 대처

탄소발자국에의 배려

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병

제휴·협업

신제품 발매

사업 확대 계획

제5장 시장 추정 및 예측 : 소스별, 2022-2035

소

돼지

가금

수산

양 및 염소

제6장 시장 추정 및 예측 : 제품별, 2022-2035

식용

비식용

제7장 시장 추정 및 예측 : 구경별, 2022-2035

소구경(14-32 mm)

중구경(33-50 mm)

대구경(50mm 이상)

제8장 시장 추정 및 예측 : 용도별, 2022-2035

생소시지

가열 소시지

건조 숙성 소시지

훈제 소시지

육류 기반 스낵

기타

제9장 시장 추정 및 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트

기타 중동 및 아프리카

제10장 기업 개요

Belkozin

FABIOS S.A.

Fibran Group

Foodchem International Corporation

Nippi Inc.

PS Seasoning

SARIA SE & Co. KG

Shenguan Holdings(Group) Limited

Viscofan S.A.

Viskoteepak

KSM

영문 목차

영문목차

The Global Collagen Casings Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 3 billion by 2035.

Collagen casings are edible, protein-rich sausage casings made from bovine or porcine collagen, offering a natural and sustainable alternative to traditional casings derived from animal intestines. They are primarily produced from bovine hides and are widely used in sausage manufacturing because they provide uniformity, convenience, and compatibility with high-speed automated machinery, which significantly boosts operational efficiency for meat processors. The steady rise in global meat consumption is fueling demand for collagen casings, as they provide scalable and cost-effective solutions compared to natural alternatives. According to the Food and Agriculture Organization, global meat production reached nearly 364 million metric tons in 2023, with expectations of continuous growth, particularly in emerging markets. Collagen casings are favored because they maintain consistent diameters, withstand production forces, and reduce contamination risks while meeting stringent food safety regulations.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.5 Billion

Forecast Value

$3 Billion

CAGR

6.8%

The bovine collagen segment held a 47.9% share in 2025 and is expected to grow at a CAGR of 6.6% through 2035. Its strength, stability, and seamless integration into automated production lines make it a preferred choice for major sausage processors. Availability from the beef industry ensures cost-effective sourcing and reliable performance.

The edible collagen casings segment held 92.1% share in 2025. Fresh, cooked, and smoked edible casings are widely used in high-volume sausage production. Their ability to remain on the product during consumption, uniform sizing, and compatibility with automated stuffing systems make them the go-to option for meat processors of all scales worldwide.

North America Collagen Casings Market captured USD 446.2 million in 2025 and is projected grow at a CAGR of 6.6% from 2026 to 2035. Rising consumer demand for natural, clean-label, and allergen-free foods is driving the adoption of collagen casings in processed meat, ready-to-eat meals, and snacks. Companies are increasingly focusing on sustainable sourcing and environmentally friendly manufacturing processes to meet consumer expectations regarding health, transparency, and product quality.

Key players in the Global Collagen Casings Market include FABIOS S.A., Belkozin, Nippi Inc., PS Seasoning, Fibran Group, Viscofan S.A., Shenguan Holdings (Group) Limited, Viskoteepak, Foodchem International Corporation, and SARIA SE & Co. KG. Market participants are strengthening their position by investing in R&D to develop high-performance, consistent, and clean-label casings. Collaborations with meat processors and food manufacturers allow them to customize solutions for automated production lines. Geographic expansion into emerging markets with growing meat consumption enhances market penetration. Companies also focus on sustainable sourcing and eco-friendly manufacturing processes to meet regulatory standards and consumer demand. Offering technical support, training, and innovation in casing design further solidifies brand loyalty and increases competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Source

2.2.3 Product

2.2.4 Caliber

2.2.5 Application

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising global meat consumption & processing

3.2.1.2 Advantages over natural casings

3.2.1.3 Sustainability & circular economy trends

3.2.2 Industry pitfalls and challenges

3.2.2.1 Raw material price volatility

3.2.2.2 Competition from alternative casings

3.2.3 Market opportunities

3.2.3.1 Tannery waste valorization

3.2.3.2 Premium certification markets

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter';s analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By source

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Million Metres)

5.1 Key trends

5.2 Bovine

5.3 Porcine

5.4 Poultry

5.5 Marine

5.6 Ovine & caprine

Chapter 6 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Million Meters)

6.1 Key trends

6.2 Edible

6.3 Non-edible

Chapter 7 Market Estimates and Forecast, By Caliber, 2022-2035 (USD Billion) (Million Meters)

7.1 Key trends

7.2 Small diameter (14-32 mm)

7.3 Medium diameter (33-50 mm)

7.4 Large diameter (>50 mm)

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Million Meters)

8.1 Key trends

8.2 Fresh sausages

8.3 Cooked sausages

8.4 Dry-cured sausages

8.5 Smoked sausages

8.6 Meat-based snacks

8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Million Meters)