Secure Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913459

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

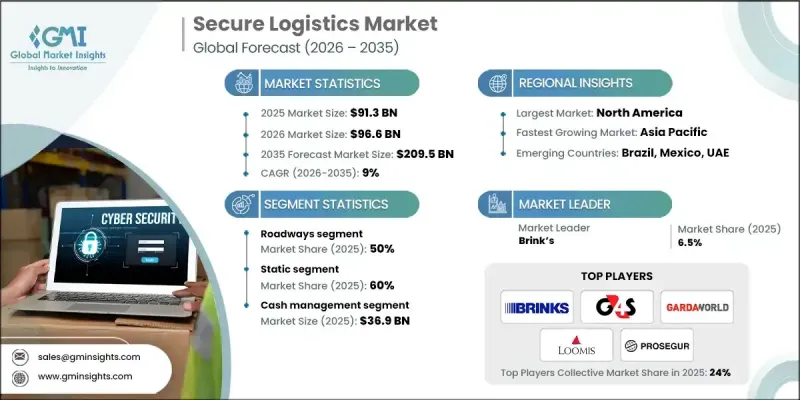

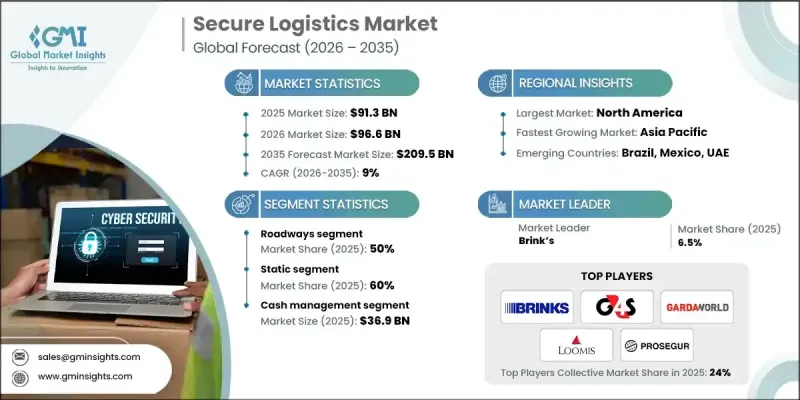

세계의 보안 물류 시장은 2025년 913억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 9%로 성장하여 2,095억 달러에 이를 것으로 예측됩니다.

이러한 성장은 국제무역의 꾸준한 증가, 고가치 화물의 보호에 대한 우려 증가, 그리고 신뢰성이 높고 규제에 따른 밸류체인 운영에 대한 의존도의 상승에 의해 견인되고 있습니다. 다양한 산업의 조직들이 금전적 자산, 기밀성이 높은 자재, 규제 대상품, 중요한 비즈니스 문서의 보호를 보다 중시하게 되어 전문적인 물류 서비스에 대한 수요가 높아지고 있습니다. 물류 업무의 지속적인 디지털 변환은 운송 수명주기 전반에 걸쳐 가시성, 추적 가능성 및 위험 관리를 개선하여 전통적인 운송 및 보관 모델을 변화시키고 있습니다. 수집, 운송 및 배달에서 자산의 종단 간 모니터링은 손실 최소화, 업무 효율성 향상 및 규제 요구 사항에 대응하는 기업의 표준 요구 사항이 되고 있습니다. 시장 확대는 또한 온라인 상거래 성장, 국제 운송량 증가, 결제 생태계 진화, 고가치 화물에 대한 위험 완화 및 보험 조정에 대한 관심 증가에 의해 지원되고 있습니다. 안전한 물류 서비스는 비즈니스 연속성과 비즈니스 탄력성의 기초 요소가 되었습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 규모

913억 달러

예측 금액

2,095억 달러

CAGR

9%

도로 운송 부문은 2025년 50%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 8.4%를 보일 것으로 예측됩니다. 이 부문은 높은 가치와 민감한 화물의 유연성, 신뢰성 및 비용 효율적인 운송을 제공할 수 있기 때문에 주도적인 지위를 유지하고 있습니다. 디지털 기술을 활용한 차량 관리 및 모니터링 기능의 광범위한 도입에 의해 국내 및 지역 공급망 전체에서 신뢰성이 높은 배송 실적, 리스크 저감, 컴플라이언스의 확보가 실현되고 있습니다. 도로 운송의 운영 범위와 확장성은 계속해서 다양한 산업에서 선호되는 선택입니다.

정적 부문은 2025년에 60%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR) 8%에서 추이할 것으로 예측됩니다. 이 부문이 주도적인 입장에 있는 것은 안전한 보관 환경의 제공, 집중 관리 기능, 자산의 지속적인 모니터링을 담당하고 있기 때문입니다. 고급 데이터 중심 관리 툴과 통합 모니터링 프레임워크는 분산 운영 전반에서 워크플로우 효율성 향상, 보호 기준 강화, 일관된 컴플라이언스를 제공합니다. 정적 서비스는 종합적인 보안 물류 네트워크의 구조적 기반을 형성하고 모바일 운영과의 원활한 협력을 지원합니다.

미국의 보안 물류 시장은 2025년 76%의 점유율을 차지하여 242억 달러 규모를 창출했습니다. 시장 리더십은 고가치 자산을 다루는 대기업의 강한 집중, 첨단 디지털 도입 및 확립된 규제 시스템에 의해 지원됩니다. 통합 물류 플랫폼, 실시간 시각화 도구 및 예측 리스크 관리 솔루션의 광범위한 활용은 국내 전역에서 시장 확대를 지속적으로 추진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 요인

현금 수송 및 고가치화물 보호에 대한 수요 증가

기술적 진보

규제 준수 요건

전자상거래 및 크로스 보더 무역의 성장

업계의 잠재적 위험 및 과제

높은 운영 비용

보안 위험 및 도난

시장 기회

신흥 시장에서의 사업 확대

디지털 솔루션 통합

3개 고가치 및 기밀화물용 전문 보안 솔루션

성장 가능성 분석

규제 상황

북미

미국 교통부(DOT) 및 연방 자동차 운송 안전국(FMCSA) 가이드라인

OSHA 기준

캐나다 귀중화물 운송 규제 및 노동법

유럽

독일 연방노동사회성(BMAS) 및 연방경찰(Bundespolizei) 규제

프랑스 CNIL 및 내무성 가이드라인

영국 ACPO(경찰장관협회) 및 HSE(건강안전집행국) 가이드라인

이탈리아 내무부 및 노동부의 컴플라이언스

아시아태평양

중국 주택도시농촌개발부 및 공안국 가이드라인

일본 국토교통성(MLIT) 컴플라이언스

한국 고용노동성부(MOEL)의 규제

인도 도로교통부(MoRTH) 가이드라인

라틴아메리카

브라질 교통부 및 MTE 가이드라인

멕시코 연방 통신부(SCT) 및 노동부(STPS) 가이드라인

중동 및 아프리카

아랍에미리트(UAE) 인재자원 및 에미리트화 가이드라인

사우디아라비아 인적자원사회개발부 및 교통부 규제

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

신흥기술

가격 동향

지역별

제품별

비용 내역 분석

특허 분석

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

이용 사례 시나리오

위험, 위협 및 손실 프로파일 분석

도난, 도용 및 무장 강도 위험 프로파일링

내부자 위협 및 공모 위험

사이버 및 피지컬 보안 위협(GPS 위장, 데이터 침해)

지역별 리스크 강도 매핑(고 리스크 회랑)

보험, 책임 및 리스크 이전 메커니즘

고가치 화물용 보험보상 모델

화물주, 물류사업자, 보험사간의 책임분담

손실 이력이 보험료에 미치는 영향

지역별 책임 한도에 관한 규제

서비스 레벨 아키텍처와 계약 모델

엔드 투 엔드형과 모듈형 보안 물류 서비스의 비교

SLA의 구성(대응 시간, 손실 임계값, 위약금)

계약 기간과 가격 체계

벤더 락인과 퇴출 위험

보안 인프라와 자산 배치 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 서비스별, 2022-2035년

정적

모바일

제6장 시장 추계 및 예측 : 운송 수단별, 2022-2035년

도로 운송

항공 운송

철도

수로

제7장 시장 추계 및 예측 : 용도별, 2022-2035년

현금 관리

귀금속

기밀 문서

고감도 전자 기기

기타

제8장 시장 추계 및 예측 : 지역별, 2022-2035년

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

싱가포르

한국

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

아랍에미리트(UAE)

남아프리카

사우디아라비아

제9장 기업 프로파일

글로벌 기업

Brink’s

DHL Secure Logistics

G4S

GardaWorld

Loomis

Loomis International

Malca-Amit

Prosegur

Securitas

Transguard

지역 기업

Brink’s UK

CMS Info Systems

G4S South Africa

GardaWorld Canada

Loomis France

Maltacourt Global Logistics

Prosegur Cash Mexico

SecurCash Europe

Transnational Secure Logistics

Tristar Secure Logistics

신흥기업

Apex Cash Transport

Elite Armored Transport

Quantum Secure Logistics

Sentinel Cash Solutions

Swift Secure Logistics

JHS

영문 목차

영문목차

The Global Secure Logistics Market was valued at USD 91.3 billion in 2025 and is estimated to grow at a CAGR of 9% to reach USD 209.5 billion by 2035.

Growth is being driven by the steady rise in international trade, heightened concern around the protection of high-value shipments and increasing reliance on dependable and compliant supply chain operations. Organizations across multiple sectors are placing greater emphasis on safeguarding monetary assets, sensitive materials, regulated goods, and critical business documents, which is elevating demand for specialized logistics services. Ongoing digital transformation within logistics operations is reshaping traditional transport and storage models by improving visibility, traceability, and risk control throughout the movement lifecycle. End-to-end oversight of assets during collection, transit, and delivery is becoming a standard requirement as businesses seek to minimize loss, enhance operational efficiency, and meet regulatory expectations. Market expansion is further supported by the growth of online commerce, rising international shipment volumes, evolving payment ecosystems, and increased focus on risk mitigation and insurance alignment for valuable cargo. Secure logistics services have become a foundational component of business continuity and operational resilience.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$91.3 Billion

Forecast Value

$209.5 Billion

CAGR

9%

The roadways segment accounted for 50% share in 2025 and is projected to grow at a CAGR of 8.4% from 2026 to 2035. This segment maintains its lead due to its ability to provide adaptable, dependable, and cost-efficient movement of high-value and sensitive consignments. Broad deployment of digitally enabled fleet management and monitoring capabilities supports reliable delivery performance, risk reduction, and compliance across domestic and regional supply chains. The operational reach and scalability of road-based transport continue to make it the preferred option across industries.

The static segment held 60% share in 2025 and is expected to register a CAGR of 8% through 2035. This segment leads due to its role in providing secure storage environments, centralized control functions, and continuous oversight of assets. Advanced data-driven management tools and integrated monitoring frameworks enable improved workflow efficiency, enhanced protection standards, and consistent compliance across distributed operations. Static services form the structural backbone of comprehensive secure logistics networks and support seamless coordination with mobile operations.

United States Secure Logistics Market accounted for 76% share and generated USD 24.2 billion in 2025. Market leadership is supported by a strong concentration of large enterprises handling high-value assets, advanced digital adoption, and well-established regulatory systems. Widespread use of integrated logistics platforms, real-time visibility tools, and predictive risk management solutions continues to drive market expansion across the country.

Key companies operating in the Global Secure Logistics Market include Prosegur, Brink's, Loomis, GardaWorld, G4S, Transguard, Securitas, DHL Secure Logistics, CMS Info Systems, and Maltacourt Global Logistics. Companies in the Global Secure Logistics Market are strengthening their market position through technology-driven service enhancement and geographic expansion. Many providers are investing in advanced digital platforms to improve visibility, control, and risk assessment across logistics operations. Strategic partnerships with financial institutions, retailers, and technology firms are helping expand service portfolios and client reach. Firms are also focusing on fleet modernization, infrastructure upgrades, and workforce training to improve service reliability and compliance.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Service

2.2.3 Mode of Transportation

2.2.4 Application

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising demand for cash-in-transit and high-value goods protection

3.2.1.2 Technological advancements

3.2.1.3 Regulatory compliance requirements

3.2.1.4 Growth in e-commerce and cross-border trade

3.2.2 Industry pitfalls and challenges

3.2.2.1 High operational costs

3.2.2.2 Security risks and theft

3.2.3 Market opportunities

3.2.3.1 Expansion in emerging markets

3.2.3.2 Integration of digital solutions

3.2.3. 3 Specialized secure solutions for high-value and sensitive goods

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S. DOT & FMCSA Guidelines

3.4.1.2 OSHA Standards

3.4.1.3 Canada Transport of Valuable Goods Regulations & Labour Code

3.4.2 Europe

3.4.2.1 Germany BMAS & Bundespolizei Regulations

3.4.2.2 France CNIL & Ministry of the Interior Guidelines

3.4.2.3 United Kingdom ACPO & HSE Guidelines

3.4.2.4 Italy Ministry of the Interior & Ministry of Labour Compliance

3.4.3 Asia Pacific

3.4.3.1 China MOHURD & Public Security Bureau Guidelines

3.4.3.2 Japan MLIT Compliance

3.4.3.3 South Korea MOEL Regulations

3.4.3.4 India MoRTH Guidelines

3.4.4 Latin America

3.4.4.1 Brazil Ministry of Transport & MTE Guidelines

3.4.4.2 Mexico SCT & STPS Guidelines

3.4.5 Middle East and Africa

3.4.5.1 UAE Ministry of Human Resources & Emiratisation Guidelines

3.4.5.2 Saudi Arabia HRSD & Transport Ministry Regulations