자동차용 차동 기어 시장 : 성장 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Automotive Differential Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913451

리서치사:Global Market Insights Inc.

발행일:2026년 01월

페이지 정보:영문 230 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

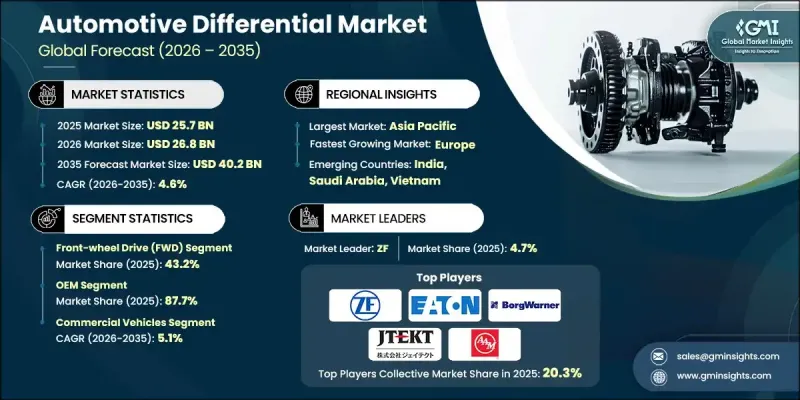

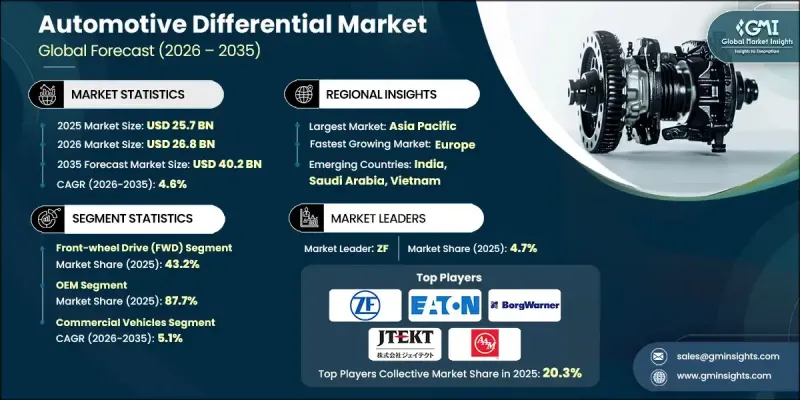

세계의 자동차용 차동 기어 시장은 2025년 257억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 4.6%로 성장하여 402억 달러에 이를 것으로 예측됩니다.

시장 성장은 중산계급 소비자의 가처분 소득 수준 상승과 운송 및 물류 섹터의 지속적인 확대에 견인되는 세계 자동차 생산 증가에 의해 지원되고 있습니다. 개인 이동 수단과 화물 운송에 대한 수요 증가는 승용차와 상용차 모두의 지속적인 생산에 기여하고 있으며, 이는 자동차용 차동 기어 수요를 직접 지원합니다. 대중교통 시스템과 물류 업무의 성장은 버스, 밴, 트럭의 제조를 더욱 가속화하고 시장의 기세를 강화하고 있습니다. 차동 기어 제조업체는 변화하는 파워트레인 구조에 대응하기 위해 차량 고유의 솔루션 개발을 강화하고 있습니다. 전기자동차와 하이브리드 자동차의 보급 확대로 공급업체는 새로운 구동 시스템 요구 사항에 적합한 차동 시스템의 재 설계 및 통합을 추진하고 있습니다. 기술 진보로 토크 배분, 트랙션 관리, 차량 안정성을 향상시키는 전자 제어식 및 스마트 차동 시스템에 대한 주목이 높아지고 있습니다. 차량 시스템이 소프트웨어 주도형 및 센서 통합형으로 진화하는 가운데, 전자 제어식 첨단 차동 기어는 다양한 차종 카테고리에서 중요성을 증가시키고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 규모

257억 달러

예측 금액

402억 달러

CAGR

4.6%

2025년 시점에서 전륜 구동 부문은 43.2%의 점유율을 차지하여 111억 달러의 수익을 창출했습니다. 전륜 구동 구성은 비용 효율성과 컴팩트한 설계로 널리 채택되어 동력 전달 부품이 단일 어셈블리에 통합되어 있습니다. 이 구조는 제조의 복잡성과 차량 전체의 비용을 절감하고 세계 시장에서의 보급을 지원합니다.

2025년 시점에서 OEM 부문은 87.7%의 점유율을 차지했으며 2035년까지 359억 달러에 달할 것으로 예측됩니다. OEM 제조업체는 통합된 차량 생산 전략과 진화하는 성능 요구사항을 충족하는 고품질의 용도 특화형 구성 요소를 제공할 수 있기 때문에 차동 장치 공급의 주요 공급원이 되고 있습니다.

미국의 자동차용 차동 기어 시장은 2025년 38억 3,000만 달러에 달했습니다. 시장 성장은 자동차 생산 활동 증가와 자동차 제조업체와 부품 공급업체 간의 협력 강화에 의해 지원됩니다. 자사 생산에 따른 높은 제조 비용이 OEM 제조업체에 전문 차동 기어 제조업체와의 제휴를 촉구해, 맞춤화된 구동계 요구에 대응하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 요인

세계 자동차 생산 대수 증가

SUV 및 사륜구동 차량에 대한 수요 증가

오프로드 차량 및 레크리에이션 차량 부문의 성장

상용차의 보급 확대

업계의 잠재적 위험 및 과제

차량의 중량 및 패키징 제약

설계 및 유지 보수의 복잡성

시장 기회

전기자동차에 전기식 차동 장치 보급 확대

고성능 차동 기어에 대한 애프터마켓 수요 증가

신흥 자동차 시장에서의 성장

가볍고 컴팩트한 차동 기어 솔루션 개발

성장 가능성 분석

규제 상황

북미

SAE(자동차 기술회)

FMVSS(연방 자동차 안전 기준-NHTSA)

ASTM International

CSA Group

유럽

UNECE(유엔 유럽 경제위원회) 규제(ECE)

ISO(국제표준화기구)

EN 규격(CEN)

TUV 규격/인증

아시아태평양

JIS(일본 공업 규격)

GB/T 규격(중국)

AIS(자동차 산업 규격 - 인도)

라틴아메리카

ABNT 규격(브라질)

NOM 규격(멕시코)

IRAM 규격(아르헨티나)

중동 및 아프리카

GSO 규격(걸프 협력 회의)

SASO 규격(사우디아라비아)

SABS 규격(남아프리카)

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

신흥기술

가격 동향

지역별

제품별

생산 통계

생산 거점

소비 거점

수출과 수입

비용 내역 분석

지속가능성과 환경영향

환경 영향 평가

사회적 영향과 지역사회에의 공헌

거버넌스와 기업의 사회적 책임

지속 가능한 금융과 투자 동향

전기화의 영향 평가

전기자동차용 차동 장치의 설계상 차이

E-axle의 통합 동향

전기자동차의 토크 벡터링

기존 제조업체의 전환 과제

성능 및 효율 벤치마크

유형별 차동 효율 평가

내구성 및 수명 분석

소음, 진동 및 불쾌감(NVH) 성능

열 관리 능력

사례 연구

전망과 기회

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 차종별, 2022-2035년

오픈 디퍼렌셜

리미티드 슬립 디퍼렌셜(LSD)

전자 제어식 리미티드 슬립 디퍼렌셜(ELSD)

잠금식 차동 기어

수동 잠금(드라이버 조작식)

자동 잠금(휠 슬립을 감지)

토크 차동 기어

제6장 시장 추계 및 예측 : 컴포넌트별, 2022-2035년

차동 기어

차동 케이스 및 하우징

베어링 및 씰

전자제어부품

제7장 시장 추계 및 예측 : 차량별, 2022-2035년

승용차

해치백

세단

SUV

상용차

소형 상용차(LCV)

대형 상용차(MCV)

대형 상용차(HCV)

제8장 시장 추계 및 예측 : 구동 방식별, 2022-2035년

전륜 구동(FWD)

후륜 구동(RWD)

총륜 구동(AWD)/사륜구동(4WD)

제9장 시장 추계 및 예측 : 추진력별, 2022-2035년

내연기관(ICE)

전기자동차(EV)

하이브리드

제10장 시장 추계 및 예측 : 판매 채널별, 2022-2035년

OEM

애프터마켓

제11장 시장 추계 및 예측 : 지역별, 2022-2035년

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

베네룩스

아시아태평양

중국

인도

일본

한국

ANZ

싱가포르

말레이시아

인도네시아

베트남

태국

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제12장 기업 프로파일

글로벌 기업

ZF

American Axle & Manufacturing(AAM)

Dana

BorgWarner

GKN Automotive

Eaton

JTEKT

Linamar

Schaeffler

Magna

Hyundai Mobis

Meritor(Cummins)

Continental

NSK

지역 기업

Bharat Gears

Neapco

Huayu Automotive Systems

Tata Motors

Sona Comstar

AmTech

Univance

신흥기업

Auburn Gear

Drexler Automotive

RT Quaife

Xtrac

JHS

영문 목차

영문목차

The Global Automotive Differential Market was valued at USD 25.7 billion in 2025 and is estimated to grow at a CAGR of 4.6% to reach USD 40.2 billion by 2035.

Market growth is supported by rising global vehicle production, driven by higher disposable income levels among middle-class consumers and continued expansion within the transportation and logistics sectors. Increasing demand for personal mobility and freight movement is contributing to sustained production of both passenger and commercial vehicles, which directly supports demand for automotive differentials. Growth in public transportation systems and logistics operations has further accelerated manufacturing of buses, vans, and trucks, strengthening market momentum. Differential manufacturers are increasingly developing vehicle-specific solutions to align with changing powertrain architectures. The growing presence of electric and hybrid vehicles is encouraging suppliers to redesign and integrate differential systems suited to new drivetrain requirements. Technology advancement is shifting focus toward electronically controlled and smart differential systems that enhance torque distribution, traction management, and vehicle stability. As vehicle systems become more software-driven and sensor-integrated, electronically advanced differentials are gaining greater relevance across multiple vehicle categories.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$25.7 Billion

Forecast Value

$40.2 Billion

CAGR

4.6%

The front-wheel drive segment held 43.2% share and generated USD 11.1 billion in 2025. Front-wheel drive configurations are widely adopted due to their cost efficiency and compact design, where power delivery components are integrated into a single assembly. This structure reduces manufacturing complexity and overall vehicle cost, supporting widespread use across global markets.

The original equipment manufacturer segment accounted for 87.7% share in 2025 and is expected to reach USD 35.9 billion by 2035. OEMs remain the primary channel for differential supply due to their ability to deliver high-quality, application-specific components that align with integrated vehicle production strategies and evolving performance requirements.

U.S. Automotive Differential Market reached USD 3.83 billion in 2025. Market growth is supported by rising vehicle production activity and increasing collaboration between automakers and component suppliers. High manufacturing costs associated with in-house production are encouraging OEMs to partner with specialized differential manufacturers to meet customized drivetrain needs.

Key companies operating in the Global Automotive Differential Market include Dana, ZF, Magna, Eaton, BorgWarner, GKN Automotive, Schaeffler, American Axle & Manufacturing, Linamar, and JTEKT. Companies active in the Global Automotive Differential Market are strengthening their market position through technology innovation, strategic partnerships, and platform-specific product development. Many manufacturers are investing in advanced differential technologies that improve efficiency, durability, and electronic control compatibility. Collaboration with vehicle OEMs is being prioritized to co-develop integrated drivetrain solutions tailored to evolving powertrain architectures. Firms are expanding their global manufacturing footprint to serve regional markets more efficiently and reduce supply chain risks. Emphasis on lightweight materials and precision engineering is helping improve performance and fuel efficiency.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Differential

2.2.3 Component

2.2.4 Vehicle

2.2.5 Drive

2.2.6 Propulsion

2.2.7 Sales Channel

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising global vehicle production

3.2.1.2 Growing demand for SUVs and all-wheel drive vehicles

3.2.1.3 Growth in off-road and recreational vehicle segment

3.2.1.4 Increasing penetration of commercial vehicles

3.2.2 Industry pitfalls and challenges

3.2.2.1 Weight and packaging constraints in vehicles

3.2.2.2 Complexity in design and maintenance

3.2.3 Market opportunities

3.2.3.1 Rising adoption of electric differentials in EVs

3.2.3.2 Increasing aftermarket demand for performance differentials

3.2.3.3 Growth in emerging automotive markets

3.2.3.4 Development of lightweight and compact differential solutions

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 SAE (Society of Automotive Engineers)

3.4.1.2 FMVSS (Federal Motor Vehicle Safety Standards - NHTSA)

3.4.1.3 ASTM International

3.4.1.4 CSA Group

3.4.2 Europe

3.4.2.1 UNECE Regulations (ECE)

3.4.2.2 ISO (International Organization for Standardization)

3.4.2.3 EN Standards (CEN)

3.4.2.4 TUV Standards/Certifications

3.4.3 Asia Pacific

3.4.3.1 JIS (Japanese Industrial Standards)

3.4.3.2 GB/T Standards (China)

3.4.3.3 AIS (Automotive Industry Standards - India)

3.4.4 Latin America

3.4.4.1 ABNT Standards (Brazil)

3.4.4.2 NOM Standards (Mexico)

3.4.4.3 IRAM Standards (Argentina)

3.4.5 Middle East & Africa

3.4.5.1 GSO Standards (Gulf Cooperation Council)

3.4.5.2 SASO Standards (Saudi Arabia)

3.4.5.3 SABS Standards (South Africa)

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product

3.9 Production statistics

3.9.1 Production hubs

3.9.2 Consumption hubs

3.9.3 Export and import

3.10 Cost breakdown analysis

3.11 Sustainability and environmental impact

3.11.1 Environmental impact assessment

3.11.2 Social impact & community benefits

3.11.3 Governance & corporate responsibility

3.11.4 Sustainable finance & investment trends

3.12 Electrification impact assessment

3.12.1 EV differential design differences

3.12.2 E-axle integration trends

3.12.3 Torque vectoring in EVs

3.12.4 Transition challenges for traditional manufacturers

3.13 Performance & efficiency benchmarking

3.13.1 Differential efficiency ratings by type

3.13.2 Durability and lifespan analysis

3.13.3 Noise, vibration, and harshness (NVH) performance