비닐 아세테이트 모노머 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Vinyl Acetate Monomer (VAM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913441

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

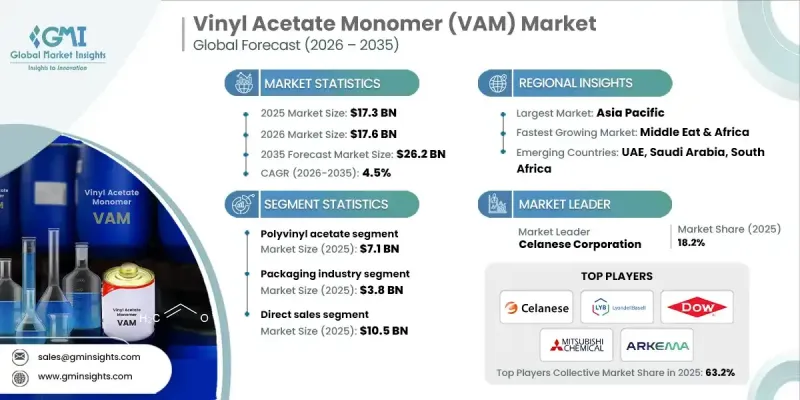

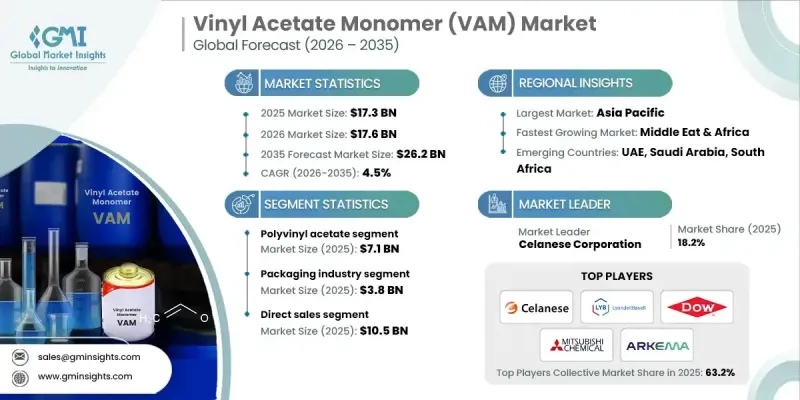

세계의 비닐 아세테이트 모노머(VAM) 시장은 2025년 173억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 4.5%로 성장하여 262억 달러에 이를 것으로 예측됩니다.

이 시장의 성장은 고성능, 지속가능한 포장 솔루션에 대한 수요 증가와 폴리 비닐 아세테이트, 에틸렌 비닐 아세테이트, 폴리 비닐 알코올과 같은 VAM 유래 폴리머 용도 확대에 이어지고 있습니다. 이 폴리머는 뛰어난 접착성, 방수성, 다용도로 포장 필름과 유연한 라미네이트에 선호됩니다. 게다가 소비재와 산업용 포장의 소비 증가, 건설, 자동차 및 공업용 도료 분야에서의 성장이 수요를 뒷받침하고 있습니다. 도시화의 진전, 인프라 정비, 개수 활동 증가에 따라, VAM 수지를 기본으로 한 접착제, 실란트, 코팅제, 복합재료의 사용이 증가하고 있습니다. 낮은 VOC 및 수성 배합을 촉진하는 환경 규제는 기존의 용매 기반 재료에서 일부 용도로 전환하고 있습니다. 첨단 생산 기술과 최적화된 제조 공정은 효율성을 높이고 공급 신뢰성을 확보하며 세계 시장에서 경쟁력을 강화하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 규모

173억 달러

예측 금액

262억 달러

CAGR

4.5%

폴리 비닐 아세테이트 부문은 접착제, 페인트, 코팅 및 건축 자재의 광범위한 용도에 힘입어 2025년에 71억 달러 시장 규모를 달성했습니다. 뛰어난 접착성, 조제의 용이함, 수성 용도와의 궁합이 좋기 때문에 포장, 목공, 종이 제품 용도에서 주요 원료가 되고 있습니다. 환경 친화적인 저 휘발성 유기 화합물(VOC) 접착제에 대한 수요가 증가함에 따라 세계 VAM 시장의 중요성이 더욱 강화되고 있습니다.

포장 업계는 2025년 38억 달러에 이르렀으며 VAM 소비량에서 가장 큰 비율을 차지했습니다. VAM 유래 PVA, PVB, EVOH 등의 폴리머는 습기와 산소를 차단하는 포장에 필수적인 우수한 접착성, 투명성, 배리어성을 제공합니다. 전자상거래 성장, FMCG 유통 네트워크 확대, 가볍고 재활용 가능한 포장 재료로의 전환이 이 부문 수요를 이끌고 있습니다.

북미의 비닐 아세테이트 모노머(VAM) 시장은 2025년 45억 달러 규모에 달했습니다. 이 지역은 통합된 석유화학 인프라, 에틸렌과 아세트산 등의 원료의 풍부한 공급, 접착제, 수성 도료, 포장 필름 및 건설용 폴리머 등 성숙한 다운스트림 시장을 갖고 있기 때문에 26%의 점유율을 차지하고 있습니다. 이 견고한 산업 기반은 VAM의 안정적인 대량 소비와 시장 성장을 보장합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 요인

수성 접착제 및 도료에 대한 수요 증가

포장 산업 확대

용제계에서 수성계로 이행

업계의 잠재적 위험 및 과제

원재료 가격의 변동성

엄격한 휘발성 유기 화합물(VOC) 배출 규제

시장 기회

식품 포장용 고배리어 EVOH 필름

의약품 전달 시스템용 의료 등급 EVA

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

용도별

미래 시장 동향

기술과 혁신 동향

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산에서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추계 및 예측 : 용도별, 2022-2035년

폴리비닐 아세테이트

폴리비닐 알코올

폴리비닐 부티랄

에틸렌 비닐 알코올

비닐 클로라이드 비닐 아세테이트 공중합체

폴리비닐포르말

기타

제6장 시장 추계 및 예측 : 최종 이용 산업별, 2022-2035년

폴리비닐 아세테이트(PVAc)

에멀젼 폴리머

접착제

도료 및 바인더

에틸렌 비닐 아세테이트 공중합체(EVA)

필름

발포체

핫멜트 접착제

태양광 봉지재

폴리비닐알코올(PVOH)

섬유

종이용 코팅제

도료 및 페인트

건축용 도료

공업용 도료

섬유용 화학제품

사이징제

마감제

종이용 화학제품

종이용 바인더

라미네이트

기타

제7장 시장 추계 및 예측 : 유통 채널별, 2022-2035년

직접 판매

리셀러

무역 회사

온라인 판매

제8장 시장 추계 및 예측 : 지역별, 2022-2035년

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Celanese Corporation

LyondellBasell Industries

Dow

Mitsubishi Chemical Corporation

Arkema

Wacker Chemie AG

Henan GP Chemicals Co., Ltd.

Suneco Chem

Meru Chem Pvt.Ltd.

Tiankai Chemical

Gantrade Corporation

Opes International

Jubilant Ingrevia

Vinipul Chemicals

JHS

영문 목차

영문목차

The Global Vinyl Acetate Monomer (VAM) Market was valued at USD 17.3 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 26.2 billion by 2035.

The market is propelled by the rising demand for high-performance, sustainable packaging solutions and the expanding use of VAM-derived polymers such as polyvinyl acetate, ethylene-vinyl acetate, and polyvinyl alcohol. These polymers are favored in packaging films and flexible laminates due to their excellent bonding, waterproofing, and versatility. The demand is further fueled by increased consumption of consumer goods, industrial packaging, and growth across the construction, automotive, and industrial coatings sectors. Rising urbanization, infrastructure development, and renovation activities are increasing the use of adhesives, sealants, coatings, and composites based on VAM resins. Environmental regulations promoting low-VOC and water-based formulations are shifting some applications from traditional solvent-based materials. Advanced production technologies and optimized manufacturing processes are enhancing efficiency, ensuring supply reliability, and strengthening competitive positions in the global market.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$17.3 Billion

Forecast Value

$26.2 Billion

CAGR

4.5%

The polyvinyl acetate segment generated USD 7.1 billion in 2025, driven by its widespread use in adhesives, paints, coatings, and construction materials. Its superior bonding, easy formulation, and compatibility with water-based applications make it a key ingredient in packaging, woodworking, and paper applications. The growing preference for environmentally friendly, low-VOC adhesives continues to reinforce its importance in the global VAM landscape.

The packaging industry reached USD 3.8 billion in 2025, accounting for the highest consumption of VAM. Polymers such as PVA, PVB, and EVOH, derived from VAM, provide exceptional adhesion, clarity, and barrier properties essential for moisture- and oxygen-resistant packaging. Growth in e-commerce, FMCG distribution networks, and the shift toward lightweight, recyclable packaging materials drives demand in this segment.

North America Vinyl Acetate Monomer (VAM) Market accounted for USD 4.5 billion in 2025. The region holds a 26% share due to its integrated petrochemical infrastructure, abundant supply of feedstocks like ethylene and acetic acid, and a mature downstream market for adhesives, water-based coatings, packaging films, and construction polymers. This strong industrial base ensures consistent high-volume VAM consumption and stable market growth.

Major players operating in the Global Vinyl Acetate Monomer (VAM) Market include Celanese Corporation, LyondellBasell Industries, Dow, Mitsubishi Chemical Corporation, Arkema, Wacker Chemie AG, Henan GP Chemicals Co., Ltd., Suneco Chem, Meru Chem Pvt. Ltd., Tiankai Chemical, Gantrade Corporation, Opes International, Jubilant Ingrevia, and Vinipul Chemicals. Companies in the Vinyl Acetate Monomer (VAM) Market strengthen their foothold by investing heavily in research and development to improve product performance, sustainability, and application versatility. They expand manufacturing capacities and establish integrated production facilities to secure reliable supply chains and reduce costs. Strategic partnerships, collaborations with downstream polymer producers, and geographic market expansion help target high-growth regions. Firms also adopt environmentally compliant production processes and low-VOC formulations to meet regulatory standards and attract eco-conscious clients.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Usage

2.2.3 End use industry

2.2.4 Distribution

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing demand for waterborne adhesives & coatings

3.2.1.2 Expansion of packaging industry

3.2.1.3 Shift from solvent-based to water-based formulations

3.2.2 Industry pitfalls and challenges

3.2.2.1 Raw material price volatility

3.2.2.2 Stringent VOC emission regulations

3.2.3 Market opportunities

3.2.3.1 High-barrier EVOH films for food packaging

3.2.3.2 Medical-grade EVA for pharmaceutical delivery systems

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By Usage

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Usage, 2022 - 2035 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Polyvinyl acetate

5.3 Polyvinyl alcohol

5.4 Polyvinyl butyral

5.5 Ethylene vinyl alcohol

5.6 Vinyl chloride-vinyl acetate copolymer

5.7 Polyvinyl formal

5.8 Others

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2022 - 2035 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Polyvinyl acetate (PVAc)

6.2.1 Emulsion polymers

6.2.2 Adhesives

6.2.3 Paints & binders

6.3 Ethylene vinyl acetate (EVA)

6.3.1 Films

6.3.2 Foams

6.3.3 Hot-melt adhesives

6.3.4 Solar encapsulants

6.4 Polyvinyl alcohol (PVOH)

6.4.1 Fibers

6.4.2 Paper coatings

6.5 Coatings & paints

6.5.1 Architectural coatings

6.5.2 Industrial coatings

6.6 Textile chemicals

6.6.1 Sizing agents

6.6.2 Finishing agents

6.7 Paper Chemicals

6.7.1 Paper binders

6.7.2 Laminates

6.8 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Direct sales

7.3 Distributors

7.4 Merchant traders

7.5 Online sales

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Kilo Tons)