자동차용 방열판 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Automotive Heat Shield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913419

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 240 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

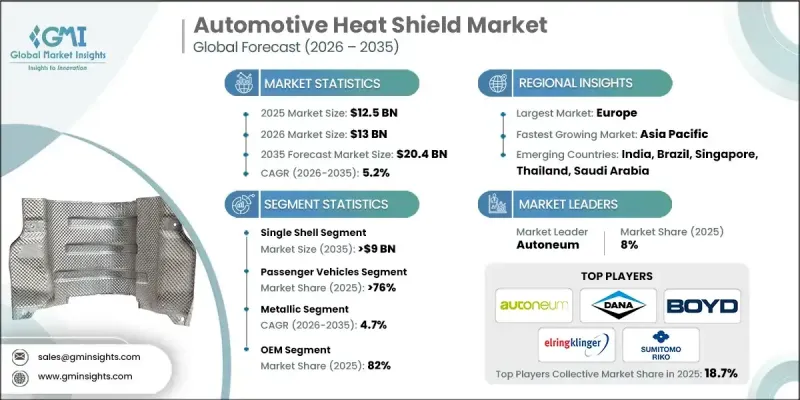

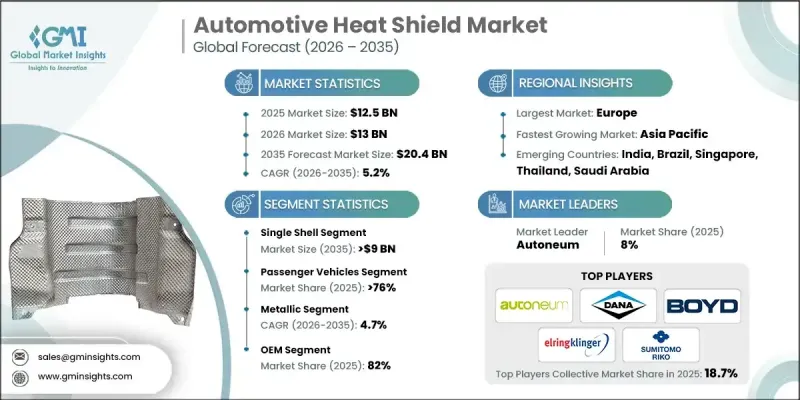

세계의 자동차용 방열판 시장은 2025년에 125억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 5.2%로 성장하여 204억 달러에 이를 것으로 예측됩니다.

시장 성장은 현대 차량 아키텍처 전반에 걸친 열 관리 요구 사항 증가에 의해 지원됩니다. 가솔린 및 디젤 차량 모두에서 과급 엔진이 채택되는 경우가 증가함에 따라 주변 부품을 보호하고 구조적 무결성을 유지하며 장기적인 엔진 성능을 지원하는 내구성 있는 열 보호 솔루션의 필요성이 커지고 있습니다. 동시에, 전기화 이동성으로의 전환으로 배터리, 파워 일렉트로닉스 및 충전 시스템과 관련된 새로운 열 제어에 대한 요구가 발생하고 있습니다. 자동차용 방열판은 열 분산 조정, 부품 수명 연장, 전기자동차 및 하이브리드 자동차 플랫폼 전반의 안전한 운전 지원을 위해 점점 활용되고 있습니다. 운전의 쾌적성과 차량의 안전성에 대한 소비자의 관심 증가도 수요를 더욱 강화하고 있습니다. 효과적인 단열재는 캐빈으로의 열 전달을 제한하고 민감한 시스템을 고온으로부터 보호하기 위한 것입니다. 규제 압력도 중요한 역할을 하고 있으며, 자동차 제조업체는 세계 시장에서 강화되는 배출 가스, 화재 안전 및 열 컴플라이언스 기준을 충족하기 위해 방열판에 의존합니다. 차량이 더 복잡하고 고출력화됨에 따라 고급 차열 솔루션은 성능, 안전 및 규제 준수에 필수적입니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 규모

125억 달러

예측 금액

204억 달러

CAGR

5.2%

2025년, 싱글 쉘 카테고리는 47%의 점유율을 차지했으며, 2035년까지 90억 달러에 달할 것으로 예측되고 있습니다. 이 부문은 비용 효율성, 제조 간편성, 특히 대량 생산 차량 플랫폼에서 중간 정도의 열 부하가 가해지는 응용 분야에서 효율성을 유지하면서 계속 높은 채택률을 유지합니다.

2025년에는 승용차가 76%의 점유율을 차지해 95억 달러 시장 규모를 창출했습니다. 대량생산, 배출가스 규제 강화, 터보차저 엔진의 보급, 전기화의 가속에 의해 주류 차종부터 고급 차종에 이르기까지 열 관리의 복잡화가 진행되고 있습니다.

미국의 자동차용 방열판 시장은 2025년 19억 1,000만 달러로 평가되었으며, 2035년까지 견조한 성장이 예상됩니다. 터보차저 엔진과 하이브리드 구동 시스템의 지속적인 보급은 첨단 배기 시스템 및 파워트레인용 방열판 솔루션에 대한 수요를 지원합니다. 경량화의 우선 과제는 효율목표 달성, 전기주행거리 연장, 연방안전기준 및 배출가스 기준 준수를 지원하기 위해 복합재료 및 다층 설계의 채용을 촉진하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 공정에 있어서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 요인

배출가스 규제 및 열 안전 규제의 엄격화

증가하는 자동차 생산 대수와 차량 보유 대수 성장

터보차저 및 고성능 엔진 채용 증가

전기자동차 및 하이브리드 자동차의 열 관리 수요 확대

애프터마켓에서 교환 수요의 성장

업계의 잠재적 위험 및 과제

원재료 가격의 변동성

완전 전기자동차에서의 방열판 사용량 감소 경향

시장 기회

EV용 배터리 및 파워 일렉트로닉스용 방열판

경량화 및 첨단 단열재 도입 상황

언더 바디 및 모듈형 방열판 솔루션 확대

신흥 시장에서 애프터마켓 및 개조 수요의 성장

성장 가능성 분석

규제 상황

북미

미국 - ISO 9001 품질경영시스템

캐나다 - ISO 45001 노동안전보건

유럽

영국 - ISO/IEC 27001 정보 보안 경영

독일 - ISO 50001 에너지 경영 시스템

프랑스 - ISO 45001 노동안전보건

이탈리아 - ISO 14001 환경 경영 시스템

스페인 - ISO 22000 식품 안전 경영 시스템

아시아태평양

중국 - ISO/IEC 27001 정보 보안 관리

일본 - ISO 14001 환경경영시스템

인도 - ISO 45001 노동안전보건

라틴아메리카

브라질 - ISO 14001 환경경영시스템

멕시코 - ISO 45001 노동 안전 위생

아르헨티나 - ISO 14001 환경 경영 시스템

중동 및 아프리카

UAE - ISO 14001 환경경영시스템

남아프리카공화국 - ISO 45001 노동안전보건

사우디아라비아 - ISO 14001 환경 경영 시스템

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

신흥기술

생산 통계

생산 거점

소비 거점

수출과 수입

비용 내역 분석

개발 비용 구조

R&D 비용 분석

마케팅 및 판매 비용

특허 분석

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경 배려형 이니셔티브

미래 시장 전망과 기회

OEM의 설계 소유권과 조달 의사 결정의 틀

OEM 지정형 및 공급자 설계형 방열판

비용, 중량, 열 성능의 트레이드 오프

플랫폼 레벨에서의 조달 전략

경량화와 재료 치환의 동향

금속에서 복합재로의 동향

경량화와 비용 감도의 균형

자동차 제조업체의 CO2 규제 대응 전략에 대한 영향

첨단 재료의 채용 장벽

EV가 방열 구성과 설계 진화에 미치는 영향

내연기관차, 하이브리드차 및 전기자동차에 있어서의 방열판 수요의 변화

배터리, 인버터 및 파워 일렉트로닉스용 차폐 필요성

차량당 순함량 변화

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 제품별, 2022-2035년

싱글 쉘

더블 쉘

샌드위치

제6장 시장 추계 및 예측 : 차량별, 2022-2035년

승용차

해치백

세단

SUV

상용차

LCV

MCV

HCV

제7장 시장 추계 및 예측 : 재료별, 2022-2035년

금속

세라믹

복합재료

제8장 시장 추계 및 예측 : 추진력별, 2022-2035년

내연기관(ICE)

하이브리드

전기식

BEV

FCEV

PHEV

제9장 시장 추계 및 예측 : 판매채널별, 2022-2035년

OEM

애프터마켓

제10장 시장 추계 및 예측 : 용도별, 2022-2035년

하부 방열판

엔진

배기

터보차저

변속

기타

제11장 시장 추계 및 예측 : 지역별, 2022-2035년

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

포르투갈

크로아티아

베네룩스

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

베트남

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

튀르키예

제12장 기업 프로파일

글로벌 기업

Autoneum

Dana

ElringKlinger

Freudenberg Sealing Technologies

Morgan Advanced Materials

Sumitomo Riko

Carcoustics

UGN

Adler Pelzer

Toyoda Gosei

Nihon Tokushu Toryo

지역 기업

Boyd

Frenzelit

Happich

Talbros

Design Engineering

Thermo-Tec Automotive

Sekisui Chemical

Sika Automotive

Trelleborg Automotive

Emerging/Disruptor Players

Alpha Engineered Components

Anhui Parker New Material

Heatshield Products

Zircotec

Pyrotek Automotive Thermal Solutions

Unifrax

JHS

영문 목차

영문목차

The Global Automotive Heat Shield Market was valued at USD 12.5 billion in 2025 and is estimated to grow at a CAGR of 5.2% to reach USD 20.4 billion by 2035.

Market growth is supported by rising thermal management requirements across modern vehicle architectures. Increasing adoption of forced-induction engines in both gasoline and diesel vehicles is intensifying the need for durable heat protection solutions that safeguard surrounding components, preserve structural integrity, and support long-term engine performance. At the same time, the shift toward electrified mobility is introducing new thermal control demands linked to batteries, power electronics, and charging systems. Automotive heat shields are increasingly used to regulate heat dispersion, improve component lifespan, and support safe operation across electric and hybrid platforms. Growing consumer focus on driving comfort and vehicle safety is further strengthening demand, as effective thermal insulation limits heat transfer into the cabin and protects sensitive systems from elevated temperatures. Regulatory pressure also plays a key role, with automakers relying on heat shields to meet tightening emission, fire safety, and thermal compliance standards across global markets. As vehicles become more complex and power-dense, advanced heat shielding solutions remain essential to performance, safety, and regulatory alignment.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$12.5 Billion

Forecast Value

$20.4 Billion

CAGR

5.2%

In 2025, the single-shell category represented 47% share and is forecast to reach USD 9 billion by 2035. This segment continues to see strong adoption due to its cost efficiency, straightforward production, and effectiveness in applications with moderate thermal exposure, particularly across high-volume vehicle platforms.

The passenger vehicles accounted for 76% share in 2025, generating USD 9.5 billion. High production volumes, stricter emission requirements, widespread turbocharged engine use, and accelerating electrification are increasing thermal management complexity across both mainstream and premium vehicle segments.

U.S. Automotive Heat Shield Market was valued at USD 1.91 billion in 2025 and is expected to post solid growth through 2035. Continued uptake of turbocharged engines and hybrid drivetrains is sustaining demand for advanced exhaust and powertrain heat shielding solutions. Lightweighting priorities encourage greater use of composite and multilayer designs to support efficiency targets, extended electric driving range, and compliance with federal safety and emission standards.

Key companies operating in the Global Automotive Heat Shield Market include Dana, Autoneum, ElringKlinger, Morgan Advanced Materials, Boyd, Freudenberg Sealing Technologies, Sumitomo Riko, Zircotec, Carcoustics, and Thermo-Tec Automotive. Companies in the Global Automotive Heat Shield Market are strengthening their competitive position through material innovation, lightweight design development, and close collaboration with vehicle manufacturers. Investments in advanced composites and multilayer insulation technologies are helping suppliers address rising thermal loads while supporting fuel efficiency and electric vehicle range targets. Manufacturers are expanding localized production and engineering capabilities to align with OEM platform strategies and shorten development cycles. Long-term supply agreements, platform-specific customization, and early-stage design integration are being used to secure recurring business.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast

1.8 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Vehicle

2.2.4 Material

2.2.5 Sales channel

2.2.6 Propulsion

2.2.7 Application

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook & strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Stringent emission and thermal safety regulations

3.2.1.3 Rising vehicle production and vehicle parc growth

3.2.1.4 Increasing adoption of turbocharged and high-performance engines

3.2.1.5 Expanding thermal management needs in electric and hybrid vehicles

3.2.1.6 Growth in aftermarket replacement demand

3.2.2 Industry pitfalls and challenges

3.2.2.1 Volatility in raw material prices

3.2.2.2 Declining heat shield intensity in fully electric vehicles

3.2.3 Market opportunities

3.2.3.1 EV battery and power electronics heat shielding

3.2.3.2 Adoption of lightweight and advanced insulation materials

3.2.3.3 Expansion of underbody and modular heat shield solutions

3.2.3.4 Aftermarket and retrofit growth in emerging markets

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 U.S. - ISO 9001 Quality Management Systems

3.4.1.2 Canada - ISO 45001 Occupational Health and Safety

3.4.2 Europe

3.4.2.1 UK - ISO/IEC 27001 Information Security Management

3.4.2.2 Germany - ISO 50001 Energy Management Systems

3.4.2.3 France - ISO 45001 Occupational Health and Safety

3.4.2.4 Italy - ISO 14001 Environmental Management Systems

3.4.2.5 Spain - ISO 22000 Food Safety Management Systems

3.4.3 Asia Pacific

3.4.3.1 China - ISO/IEC 27001 Information Security Management

3.4.3.2 Japan - ISO 14001 Environmental Management Systems

3.4.3.3 India - ISO 45001 Occupational Health and Safety

3.4.4 Latin America

3.4.4.1 Brazil - ISO 14001 Environmental Management Systems

3.4.4.2 Mexico - ISO 45001 Occupational Health and Safety

3.4.4.3 Argentina - ISO 14001 Environmental Management Systems

3.4.5 Middle East & Africa

3.4.5.1 UAE - ISO 14001 Environmental Management Systems

3.4.5.2 South Africa - ISO 45001 Occupational Health and Safety

3.4.5.3 Saudi Arabia - ISO 14001 Environmental Management Systems