Fire Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913405

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

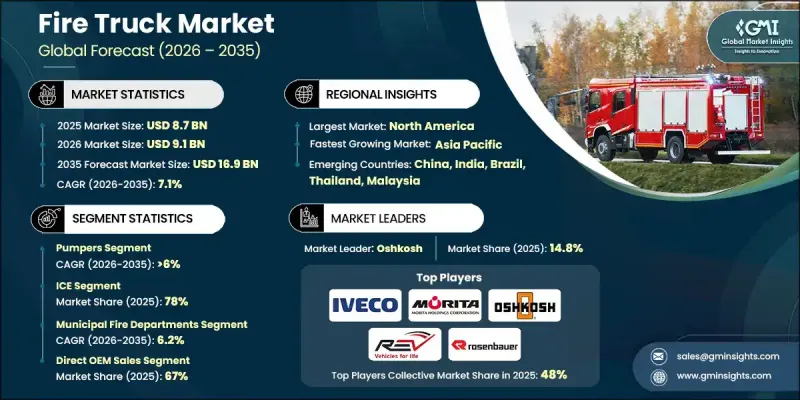

세계의 소방차 시장은 2025년 87억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 7.1%로 성장해 169억 달러에 이를 것으로 예측됩니다.

급속한 도시화가 진행되고, 인구 밀도, 고층 건축, 산업 활동이 계속 증가함에 따라 화재 위험과 긴급시 대 응요건이 높아지면서 시장은 꾸준한 기세를 늘리고 있습니다. 지자체와 산업지대에서는 확대되는 주택지, 상업시설, 인프라 자산을 보호하기 위해 현대적인 소방차에 대한 예산배분을 증가시키고 있습니다. 소방당국은 진화하는 안전기준, 배출가스 규제, 성능요건에 대응하기 위해 차량군의 현대화를 점점 우선시하고 있습니다. 많은 소방서는 운영상의 신뢰성과 컴플라이언스 기준을 충족하지 못한 구식 차량을 퇴역시켜 펌프 능력 향상, 도달 거리 연장, 탑승자의 안전 시스템 강화를 갖춘 첨단 소방 차량에 대한 투자를 추진하고 있습니다. 최신의 소방차는 신뢰성의 향상, 가동 정지 시간의 삭감, 디지털 기술의 통합 강화를 실현해, 각 기관의 긴급 대응 태세 강화에 공헌하고 있습니다. 또한 실시간 진단, 상황 인식, 효율적인 자원 배치를 지원하는 커넥티드 시스템의 보급 확대도 시장을 뒷받침하고 있어 복잡한 긴급 사태에서도 소방기관이 신속하게 대응하고 보다 효과적으로 활동할 수 있게 하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 규모

87억 달러

예측 금액

169억 달러

CAGR

7.1%

펌프차 카테고리는 2025년에 43%의 점유율을 차지했으며, 2026년부터 2035년까지 CAGR 6%를 보일 것으로 예측됩니다. 수요는 펌프 효율성 향상, 차량 조작성 개선, 밀집된 도시 환경에서의 효과적인 운영 능력에 의해 지원됩니다. 노후화된 차량의 대안과 비용 효율적인 다목적 소방차량에 대한 관심 증가가 이 부문의 확대를 지속적으로 추진하고 있습니다.

내연기관 기반 소방차는 2025년 78%의 점유율을 차지했고, 2035년까지 연평균 복합 성장률(CAGR) 6.6%를 보일 것으로 예측됩니다. 이러한 이점은 확립된 구동계 기술, 연료의 광범위한 가용성 및 가혹한 소방 활동에서 지속적인 출력을 공급할 수 있는 능력에 의해 지원됩니다. 배출가스 제어와 자동차 모니터링 시스템의 지속적인 개선으로 이러한 차량은 엄격한 환경 기준을 준수합니다.

미국 소방차 시장은 2025년 31억 9,000만 달러 규모에 이르렀습니다. 노후화된 차량의 갱신은 유지비 증가, 안전성의 부족, 갱신된 운용 기준 적합과 같은 과제에 임하는 소방 부문에 있어서도 여전히 주요한 성장 요인입니다. 여러 수준의 자금 조달 시책이 현대적인 긴급 차량의 조달을 가속화하고, 갱신 사이클의 단축과 소방관의 보호, 차량 신뢰성에 대한 투자 확대를 지지하고 있습니다.

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 요인

도시화와 인프라 확장

엄격한 방화 안전 규제

플릿의 현대화와 갱신 사이클

소방 설비의 기술적 진보

업계의 잠재적 위험 및 과제

높은 차량 및 유지 보수 비용

긴 OEM 리드 타임과 예산 제약

시장 기회

전기화 및 하이브리드 소방차

공항 및 산업용 소방 수요

텔레메트리 및 텔레매틱스 통합

애프터마켓에서의 업그레이드와 개조

성장 가능성 분석

규제 상황

북미

연방 자동차 안전 기준(FMVSS)

환경보호청(EPA) 유럽

유럽

VDA 가이드라인(VDA 5)

EU 형식 인증/완성차 형식 인증(WVTA)

UNE 규격(스페인 규격 협회)

장관령 및 UNI 규격

BS EN 규격 및 영국 형식 인증

아시아태평양

중국 국가 표준(GB)

일본 JIS 규격 요건

한국 KS 인증

자동차 산업 표준 140

태국공업규격협회(TISI)

라틴아메리카

INMETRO(국립 계량 연구소)

INTI 인증(국립공업기술연구소)

NOM(Norma Oficial Mexicana) 규격

중동 및 아프리카

ESMA/에미레이트 호환성 평가 체계(ECAS)

GCC 기술규제

SABS 인증

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

신흥기술

가격 분석

제품별

지역별

비용 내역 분석

총소유비용(TCO) 프레임워크

기술 유형별 총소유비용(TCO)

부품 단가 분석

AM과 기존 제조 비용 비교

생산 통계

생산 거점

소비 거점

수출입

특허 분석

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

이용 사례

애프터마켓 서비스 및 재생 에코시스템

보수 및 서비스 계약

예비 부품 및 개수 수요

수명 주기 서비스 수익에 대한 기여도

플릿 라이프사이클 및 갱신 사이클 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 차량별, 2022-2035년

펌프차

사다리차

탱커

구조차

항공기 구조 및 소방(ARFF) 차량

산업용 트럭

특수 트럭

제6장 시장 추계 및 예측 : 파워트레인별, 2022-2035년

내연기관(ICE)

전기자동차

하이브리드

제7장 시장 추계 및 예측 : 용도별, 2022-2035년

지자체 소방서

공항 소방 서비스

산업 소방 서비스

산불 관리

기타

제8장 시장 추계 및 예측 : 용량별, 2022-2035년

1,000갤런 미만

1,000-2,000갤런

2,000갤런 이상

제9장 시장 추계 및 예측 : 판매 채널별, 2022-2035년

직접 OEM 판매

정규 판매점/유통업체

제10장 시장 추계 및 예측 : 지역별, 2022-2035년

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

러시아

폴란드

루마니아

아시아태평양

중국

인도

일본

한국

ANZ

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

글로벌 기업

Bronto Skylift

IVECO(Magirus)

KME Fire Apparatus

Metz Fire & Rescue

Morita

Oshkosh

REV

Rosenbauer

Seagrave Fire Apparatus

Ziegler

지역 제조업체

Danko Emergency Equipment

Darley

Desautel

E-ONE

Ferrara Fire Apparatus

HME Ahrens

Marion Body Works

Smeal Fire Apparatus

Terberg DTS

Vema Lift

신흥 제조업체

Chase enterprise

FPT Industrial Electric Fire Truck

Minerva Fire Trucks

Sino Fire Trucks

TATA Fire Trucks

Volkan Fire Trucks

JHS

영문 목차

영문목차

The Global Fire Truck Market was valued at USD 8.7 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 16.9 billion by 2035.

The market is gaining steady momentum as rapid urbanization continues to increase population density, vertical construction, and industrial activity, all of which elevate fire risk and emergency preparedness requirements. Municipal bodies and industrial zones are allocating higher budgets toward modern firefighting fleets to safeguard expanding residential areas, commercial complexes, and infrastructure assets. Fire authorities are increasingly prioritizing fleet modernization to align with evolving safety mandates, emission norms, and performance expectations. Many departments are retiring legacy vehicles that no longer meet operational reliability or compliance benchmarks and are investing in advanced apparatus with enhanced pumping capacity, extended reach, and improved crew safety systems. Modern fire trucks deliver greater reliability, reduced downtime, and better integration of digital technologies, helping agencies strengthen emergency response readiness. The market is also benefiting from rising adoption of connected systems that support real-time diagnostics, situational awareness, and efficient resource deployment, enabling fire services to respond faster and operate more effectively in complex emergency scenarios.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$8.7 Billion

Forecast Value

$16.9 Billion

CAGR

7.1%

The pumper category accounted for 43% share in 2025 and is anticipated to grow at a CAGR of 6% from 2026 to 2035. Demand is supported by advancements in pump efficiency, improved vehicle handling, and the ability to operate effectively in dense urban environments. Replacement of aging units and growing interest in cost-effective, multipurpose firefighting vehicles continue to support this segment's expansion.

The internal combustion engine-based fire trucks held a share of 78% in 2025 and are projected to grow at a CAGR of 6.6% through 2035. This dominance is supported by established drivetrain technology, widespread fuel availability, and the ability to deliver sustained power output for demanding firefighting operations. Ongoing enhancements in emissions control and onboard monitoring systems are helping these vehicles remain compliant with tightening environmental standards.

U.S. Fire Truck Market generated USD 3.19 billion in 2025. Replacement of aging fleets remains a primary growth driver as departments address rising maintenance expenses, safety gaps, and compliance with updated operational standards. Funding initiatives at multiple levels are accelerating procurement of modern emergency vehicles, supporting faster replacement cycles and higher investment in firefighter protection and vehicle reliability.

Key companies active in the Global Fire Truck Market include Rosenbauer, Oshkosh, REV Group, Morita, Ziegler, Bronto Skylift, Metz Fire & Rescue, KME Fire Apparatus, IVECO (Magirus), and HME Ahrens. Manufacturers in the Global Fire Truck Market are reinforcing their market position through continuous product innovation, customization, and long-term service offerings. Companies are investing in advanced chassis design, digital control systems, and modular configurations to meet diverse operational needs across regions. Strategic focus on lifecycle support, including maintenance contracts and parts availability, is helping strengthen customer relationships. Localization of manufacturing and supplier networks is being used to improve delivery timelines and cost efficiency. Partnerships with fire departments for co-development and testing are enabling manufacturers to align products with real-world requirements while ensuring compliance with evolving safety and environmental regulations.

Table of Contents

Chapter 1 Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.2.2 Research trail & confidence scoring

1.2.2.1 Research trail components

1.2.2.2 Scoring components

1.3 Data collection

1.3.1 Partial list of primary sources

1.4 Data mining sources

1.4.1 Paid sources

1.5 Base estimates and calculations

1.5.1 Base year calculation

1.6 Forecast model

1.7 Research transparency addendum

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Vehicle

2.2.3 Powertrain

2.2.4 Application

2.2.5 Capacity

2.2.6 Sales channel

2.3 TAM analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook

2.6 Strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Urbanization & infrastructure expansion

3.2.1.2 Stringent fire safety regulations

3.2.1.3 Fleet modernization & replacement cycles

3.2.1.4 Technological advancements in firefighting equipment

3.2.2 Industry pitfalls and challenges

3.2.2.1 High vehicle & maintenance costs

3.2.2.2 Long OEM lead times & budget constraints

3.2.3 Market opportunities

3.2.3.1 Electrification & hybrid fire trucks

3.2.3.2 Airport & industrial firefighting demand

3.2.3.3 Telemetry & telematics integration

3.2.3.4 Aftermarket upgrades & retrofitting

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.1.1 Federal Motor Vehicle Safety Standards (FMVSS)