폴리테트라메틸렌 에테르 글리콜 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2026-2035년)

Polytetramethylene Ether Glycol Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913397

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

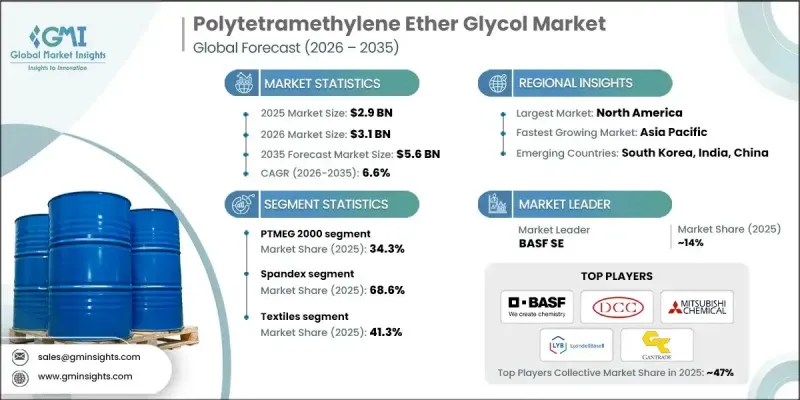

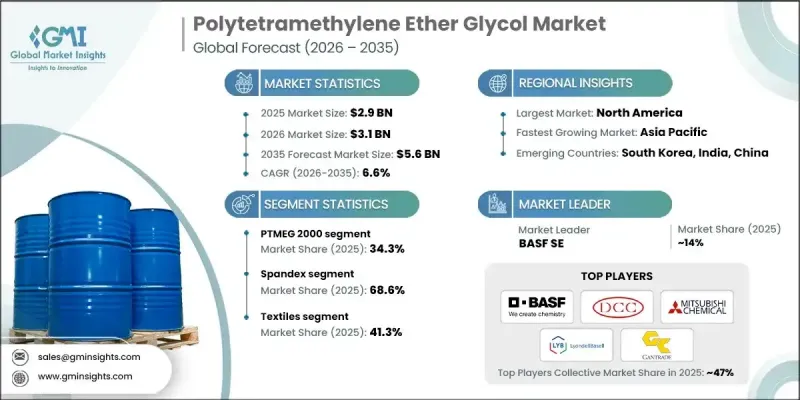

세계의 폴리테트라메틸렌 에테르 글리콜 시장은 2025년 29억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 6.6%로 성장하여 56억 달러에 이를 것으로 예측됩니다.

시장 확대는 섬유, 자동차 부품 및 첨단 재료 응용 분야에서 고성능 폴리머 수요 증가로 인한 것입니다. 폴리테트라메틸렌 에테르 글리콜(폴리테트라하이드로퓨란이라고도 함)은 탄성 섬유, 열가소성 엘라스토머 및 특수 폴리머의 핵심 구성 요소로 알려져 있습니다. 폭넓은 분자량 범위에서의 가용성은 유연성, 탄력성, 기계적 안정성이 요구되는 용도로 사용할 수 있습니다. 섬유 제조의 성장, 자동차 생산에 있어서 경량 소재의 채용 확대, 고성능 폴리머의 지속적인 혁신이 결합되어 시장 역학을 형성하고 있습니다. 생산자는 일관성, 순도 및 공정 효율성을 높이기 위해 최신 제조 기술에 투자하고 있으며, 이로 인해 까다로운 최종 이용 산업 전반의 채택 확대가 지원됩니다. 동시에 지속가능성에 대한 배려가 생산전략에 영향을 미치고 있으며 환경부하 저감, 자원 효율 향상, 순환형 경제 원칙과의 무결성에 대한 주력이 강화되고 있습니다. 이러한 추세로 인해 성숙 시장과 신흥 시장 모두에서 세계 수요가 지속적으로 확보되고 있습니다.

시장 범위

시작 연도

2025년

예측 기간

2026-2035년

시작 규모

29억 달러

시장 규모 예측

56억 달러

CAGR

6.6%

PTMEG 2000 등급은 2025년에 34.3%의 점유율을 차지했으며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 6.6%를 보일 것으로 예측됩니다. 이 등급은 우수한 탄성, 인장 강도 및 가공 유연성을 지원하는 균형 잡힌 분자 구조로 주도적인 지위를 유지합니다. 그 성능 특성으로부터 내구성과 일관된 기계적 특성을 필요로 하는 용도에 있어서 선호되는 옵션이 되고 있습니다.

스판덱스 부문은 2025년에 68.6%의 점유율을 차지했으며, 2035년까지 연평균 복합 성장률(CAGR)7%를 보일 것으로 예측됩니다. 신축성과 쾌적성을 갖춘 의류에 대한 수요가 견조하게 성장하고 있는 것이, PTMEG 기반 섬유의 많은 소비를 지지하고 있어 뛰어난 복원성, 내구성, 미관 성능을 제공하는 능력이 이것을 뒷받침하고 있습니다.

미국의 폴리테트라메틸렌 에테르 글리콜 시장은 2025년 3억 9,790만 달러 규모를 기록했습니다. 확립된 탄성섬유 생산, 열가소성 폴리우레탄의 광범위한 이용, 테크니컬 텍스타일 및 고성능 소재 분야의 지속적인 기술 혁신으로 수요는 견조하게 추진하고 있으며, 이 나라 지역의 주도적 지위를 강화하고 있습니다.

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

업계의 생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 요인

업계의 잠재적 위험과 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

신흥기술

가격 동향

지역별

제품 등급별

미래 시장 동향

기술과 혁신 동향

현재의 기술 동향

신흥기술

특허 동향

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산에서의 에너지 효율

환경에 배려한 대처

탄소발자국 고려

제4장 경쟁 구도

소개

기업별 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 동향

기업 인수합병(M&A)

사업 제휴 및 협력

신제품 발매

확대 계획

제5장 시장의 추정 및 예측 : 제품 등급별(2022-2035년)

PTMEG 250

PTMEG 650

PTMEG 1000

PTMEG 1400

PTMEG 1800

PTMEG 2000

기타

제6장 시장의 추정 및 예측 : 용도별(2022-2035년)

스판덱스

열가소성 우레탄 엘라스토머

코폴리에스테르 에테르 엘라스토머

기타

제7장 시장의 추정 및 예측 : 최종 이용 산업별(2022-2035년)

코팅

건설

접착제 및 실란트

섬유

인조 가죽

자동차

산업용

레저 및 스포츠

기타

제8장 시장의 추정 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

BASF SE

Dairen Chemical Corporation

Mitsubishi Chemical Corporation

LyondellBasell Industries NV

Gantrade Corporation

Ashland Global Holdings Inc.

Lanxess AG

Kuraray Co., Ltd.

Chang Chun Petrochemical

Shanxi Sanwei Group

Korea PTG Co., Ltd.

China Petrochemical Corporation

Brenntag

SINOPEC Great Wall Energy

IMCD Group

JHS

영문 목차

영문목차

The Global Polytetramethylene Ether Glycol Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 6.6% to reach USD 5.6 billion by 2035.

Market expansion is driven by rising demand for high-performance polymers across textiles, automotive components, and advanced material applications. Polytetramethylene ether glycol, also referred to as polytetrahydrofuran, is recognized for its role as a core building block in elastic fibers, thermoplastic elastomers, and specialty polymers. Availability across a broad range of molecular weights enables its use in applications requiring flexibility, resilience, and mechanical stability. Growth in textile manufacturing, increasing adoption of lightweight materials in automotive production, and ongoing innovation in performance polymers are collectively shaping market dynamics. Producers are investing in modern manufacturing techniques to enhance consistency, purity, and process efficiency, which is supporting wider adoption across demanding end-use industries. At the same time, sustainability considerations are influencing production strategies, with a greater focus on reducing environmental impact, improving resource efficiency, and aligning with circular economy principles. These trends are ensuring continued global demand across both mature and emerging markets.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$2.9 billion

Forecast Value

$5.6 billion

CAGR

6.6%

The PTMEG 2000 accounted for 34.3% share in 2025 and is expected to grow at a CAGR of 6.6% from 2026 to 2035. This grade maintains a leading position due to its balanced molecular structure, which supports strong elasticity, tensile strength, and processing flexibility. Its performance profile makes it a preferred option for applications requiring durability and consistent mechanical properties.

The spandex segment held 68.6% share in 2025 and is projected to grow at a CAGR of 7% through 2035. Strong growth in demand for stretchable and comfortable apparel is sustaining high consumption of PTMEG-based fibers, supported by its ability to deliver excellent recovery, durability, and aesthetic performance.

United States Polytetramethylene Ether Glycol Market generated USD 397.9 million in 2025. Demand remains strong due to established elastic fiber production, widespread use of thermoplastic polyurethanes, and continuous innovation in technical textiles and performance materials, reinforcing the country's leading regional position.

Key companies operating in the Global Polytetramethylene Ether Glycol Market include BASF SE, Mitsubishi Chemical Corporation, LyondellBasell Industries N.V., Kuraray Co., Ltd., Lanxess AG, Ashland Global Holdings Inc., Dairen Chemical Corporation, Chang Chun Petrochemical, Shanxi Sanwei Group, Korea PTG Co., Ltd., China Petrochemical Corporation, SINOPEC Great Wall Energy, Gantrade Corporation, Brenntag, and IMCD Group. Companies active in the Global Polytetramethylene Ether Glycol Market are strengthening their competitive position through capacity expansion, product differentiation, and technology advancement. Manufacturers are prioritizing process optimization to achieve higher purity levels, consistent molecular weight distribution, and improved production efficiency. Strategic investments in sustainable manufacturing practices and alternative feedstocks are helping align operations with evolving environmental expectations. Firms are also expanding global distribution networks and forming long-term supply agreements with downstream users to secure stable demand.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Product grade

2.2.2 Application

2.2.3 End use industry

2.2.4 Regional

2.3 TAM Analysis, 2025-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product grade

3.9 Future market trends

3.10 Technology and innovation landscape

3.10.1 Current technological trends

3.10.2 Emerging technologies

3.11 Patent landscape

3.12 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

3.12.1 Major importing countries

3.12.2 Major exporting countries

3.13 Sustainability and environmental aspects

3.13.1 Sustainable practices

3.13.2 Waste reduction strategies

3.13.3 Energy efficiency in production

3.13.4 Eco-friendly initiatives

3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Grade, 2022-2035 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 PTMEG 250

5.3 PTMEG 650

5.4 PTMEG 1000

5.5 PTMEG 1400

5.6 PTMEG 1800

5.7 PTMEG 2000

5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Spandex

6.3 Thermoplastic urethane elastomer

6.4 Co-polyester ether elastomers

6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2022-2035 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Coatings

7.3 Construction

7.4 Adhesives & sealants

7.5 Textiles

7.6 Artificial leather

7.7 Automotive

7.8 Industrial

7.9 Leisure & sports

7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)