무선 화재 감지 시스템 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)

Wireless Fire Detection System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913368

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 163 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

세계의 무선 화재 감지 시스템 시장은 2025년에 21억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.3%로 성장할 전망이며, 51억 달러에 이를 것으로 예측됩니다.

이 성장은 주택, 상업 및 산업 시설에서 방화 안전 및 보안 강화에 대한 수요가 증가함에 따라 견인되고 있습니다. 스마트 빌딩 기술, IoT 지원 솔루션 및 무선 통신 통합을 통해 화재 긴급 상황에 대한 실시간 모니터링 및 신속한 대응이 가능합니다. 무선 화재 감지 시스템은 유선 인프라를 필요로 하지 않으며 다양한 환경에서 유연한 설치, 신속한 도입, 효율적인 화재 관리를 실현합니다. 이 시스템에는 무선 연기 및 열 감지기, 제어반, 알람 모듈 및 통신 게이트웨이가 포함됩니다. 역사적 건축물 및 복수 존을 가지는 대규모 시설 등 복잡한 레이아웃에서도 효과적으로 동작하는 특성으로부터, 종래의 유선 시스템에 비해 채용이 확대되고 있습니다. 예지보전, 자동 경보, 원격 모니터링 기능으로 화재 안전 관리에 있어서의 인적 개입을 삭감하면서 운용 효율을 향상시킵니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

21억 달러

예측 금액

51억 달러

CAGR

9.3%

센서 부문은 2025년에 8억 5,740만 달러의 매출을 창출했습니다. 센서는 연기, 열 및 화재 발생을 실시간으로 알람하는 무선 화재 감지 시스템에서 필수적인 역할을 합니다. 연기 감지기, 열 감지기 및 다중 센서 감지기를 포함한 무선 센서는 설치의 유연성, 신뢰성, 개조 및 복잡한 건축 구조에 대한 적합성을 제공합니다.

광전 부문은 2025년 7억 670만 달러에 달했습니다. 광전 감지기는 화재에 매우 민감하며 조기 감지를 가능하게 하고 오보를 최소화합니다. 주택, 상업 시설, 산업 시설에서의 광범위한 사용은 배터리 수명 향상, 무선 연결성, 스마트 빌딩 플랫폼과의 통합을 통해 지원되며 전체 화재 안전 성능을 향상시킵니다.

북미의 무선 화재 감지 시스템 시장은 첨단 기술 채택, 강력한 규제 프레임워크 및 디지털 안전 솔루션에 대한 견조한 투자를 배경으로 2025년 32.3%의 점유율을 차지했습니다. 미국에는 주요 제조업체 및 혁신 기업이 거점을 두고 차세대 감지기의 지속적인 발전, 신속한 상업화, IoT 및 클라우드 기반 모니터링 시스템과의 원활한 통합을 촉진하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

스마트 빌딩 및 IoT 대응 방화 안전 시스템 도입 확대

정부에 의한 규제 강화 및 건축 안전 기준의 엄격화

기존 설비용 저배선식 화재 감지 솔루션에 대한 수요 증가

무선 통신, 센서, AI 기반 검출 기술에 있어서의 진보

주택, 상업, 산업 분야에 있어서의 방화 안전 의식 고조

업계의 잠재적 위험 및 과제

높은 초기 투자 비용

밀집한 도시에서 네트워크 신뢰성 및 잠재적인 신호 간섭에 관한 우려

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현재 기술 동향

신흥 기술

가격 동향

지역별

제품별

가격 전략

신흥 비즈니스 모델

컴플라이언스 요건

지속가능성 대책

소비자 심리 분석

특허 및 지적재산 분석

지정학적 및 무역 동향

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

시장 집중도 분석

주요 기업의 경쟁 벤치마킹

재무 실적 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인의 넓이

기술

혁신

지리적 존재 비교

세계 전개 분석

서비스 네트워크의 커버율

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더

챌린저

팔로워

틈새 기업

전략적 전망 매트릭스

주요 발전(2022-2025년)

합병 및 인수

제휴 및 공동 사업

기술적 진보

확대 및 투자 전략

지속가능성에 대한 노력

디지털 전환의 대처

신흥 및 스타트업 경쟁의 동향

제5장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

센서

신고 버튼

화재 경보판

입력 및 출력 모듈

기타

제6장 시장 추계 및 예측 : 센서 유형별(2022-2035년)

연기 감지기

열 감지기

가스 검출기

멀티 센서 검출기

제7장 시장 추계 및 예측 : 유형별(2022-2035년)

광전식

이온화식

듀얼 센서

기타

제8장 시장 추계 및 예측 : 모델별(2022-2035년)

완전 무선

하이브리드

제9장 시장 추계 및 예측 : 설치별(2022-2035년)

신규 설치

리노베이션

제10장 시장 추계 및 예측 : 용도별(2022-2035년)

주택

산업

상업

BFSI

교육

정부

헬스케어

접객

소매

기타

제11장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제12장 기업 프로파일

Apollo Fire Detectors Ltd.

Electro Detectors Ltd.

EMS Security Group

EuroFyre Ltd.

Gentex Corporation

Halma PLC(Apollo, Advanced, etc.)

Hochiki Corporation

Honeywell International Inc.

Johnson Controls International plc(Tyco/SimplexGrinnell)

Kidde Technologies Inc.

Robert Bosch GmbH(Bosch Security Systems)

Schneider Electric

Securi-ton AG

Siemens AG

System Sensor

AJY

영문 목차

영문목차

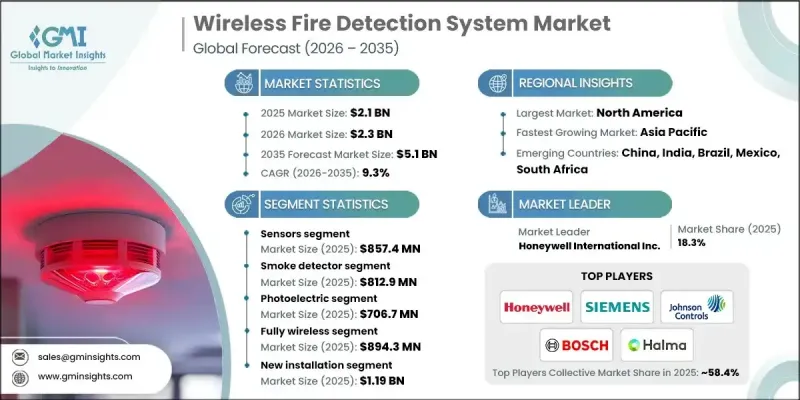

The Global Wireless Fire Detection System Market was valued at USD 2.1 billion in 2025 and is estimated to grow at a CAGR of 9.3% to reach USD 5.1 billion by 2035.

The growth is driven by the rising demand for enhanced fire safety and security across residential, commercial, and industrial spaces. The integration of smart building technologies, IoT-enabled solutions, and wireless communication is enabling real-time monitoring and faster responses to fire emergencies. Wireless fire detection systems eliminate the need for wired infrastructure, offering flexible installation, faster deployment, and efficient fire management across diverse environments. These systems include wireless smoke and heat detectors, control panels, alarm modules, and communication gateways. Their ability to operate effectively in complex layouts, including heritage buildings and large facilities with multiple zones, makes them increasingly preferred over traditional wired systems. With predictive maintenance, automated alerts, and remote monitoring, these solutions enhance operational efficiency while reducing human intervention in fire safety management.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$2.1 Billion

Forecast Value

$5.1 Billion

CAGR

9.3%

The sensors segment generated USD 857.4 million in 2025. Sensors are vital to any wireless fire detection system, providing real-time alerts for smoke, heat, and fire events. Wireless sensors, including smoke, heat, and multi-sensor detectors, offer installation flexibility, reliability, and suitability for retrofitted or complex building structures.

The photoelectric segment reached USD 706.7 million in 2025. Photoelectric detectors are highly sensitive to smoldering fires, enabling early detection and minimizing false alarms. Their widespread use in residential, commercial, and industrial setups is supported by improved battery life, wireless connectivity, and integration with smart building platforms, enhancing overall fire safety performance.

North America Wireless Fire Detection System Market held 32.3% share in 2025, driven by advanced technological adoption, strong regulatory frameworks, and robust investments in digital safety solutions. The U.S. hosts leading manufacturers and technology innovators, fostering continuous advancements, rapid commercialization of next-generation detectors, and seamless integration with IoT and cloud-based monitoring systems.

Key market participants in the Global Wireless Fire Detection System Market include Siemens AG, Kidde Technologies Inc., Schneider Electric, Honeywell International Inc., Robert Bosch GmbH (Bosch Security Systems), EMS Security Group, EuroFyre Ltd., System Sensor, Gentex Corporation, Securiton AG, Apollo Fire Detectors Ltd., Johnson Controls International plc (Tyco/SimplexGrinnell), Hochiki Corporation, Electro Detectors Ltd., and Halma PLC (Apollo, Advanced, etc.). Companies operating in the Global Wireless Fire Detection System Market are employing several strategies to strengthen their market position. These include developing next-generation detectors with enhanced sensitivity and IoT connectivity, forming strategic alliances with smart building and security solution providers, and expanding distribution networks across residential, commercial, and industrial sectors. They focus on continuous R&D to improve battery life, reduce false alarms, and enhance interoperability with building automation systems.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry snapshot

2.2 Key market trends

2.2.1 Component trends

2.2.2 Sensor type trends

2.2.3 Type trends

2.2.4 Model trends

2.2.5 Installation trends

2.2.6 Application trends

2.2.7 Regional trends

2.3 TAM Analysis, 2025-2034 (USD Billion)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing adoption of smart buildings and IoT-enabled fire safety systems.

3.2.1.2 Stricter government regulations and building safety standards.

3.2.1.3 Rising demand for retrofit low-wiring fire detection solutions.

3.2.1.4 Advancements in wireless communication, sensors, and AI-based detection.

3.2.1.5 Growing fire-safety awareness across residential, commercial, and industrial sectors.

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment costs

3.2.2.2 Concerns regarding network reliability and potential signal interference in dense urban areas.

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product

3.9 Pricing Strategies

3.10 Emerging Business Models

3.11 Compliance Requirements

3.12 Sustainability Measures

3.13 Consumer Sentiment Analysis

3.14 Patent and IP analysis

3.15 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.2.2 Market Concentration Analysis

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2022-2025

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component, 2022 - 2035 (USD Million)

5.1 Key trends

5.2 Sensors

5.3 Call Points

5.4 Fire Alarm Panels

5.5 Input/Output Modules

5.6 Others

Chapter 6 Market Estimates and Forecast, By Sensor Type, 2021 - 2034 (USD Million)

6.1 Key trends

6.2 Smoke Detector

6.3 Heat Detector

6.4 Gas Detector

6.5 Multi-sensor Detector

Chapter 7 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Million)

7.1 Key trends

7.2 Photoelectric

7.3 Ionization

7.4 Dual Sensor

7.5 Others

Chapter 8 Market Estimates and Forecast, By Model, 2022 - 2035 (USD Million)

8.1 Key trends

8.2 Fully Wireless

8.3 Hybrid

Chapter 9 Market Estimates and Forecast, By Installation, 2022 - 2035 (USD Million)

9.1 Key trends

9.2 New Installation

9.3 Retrofit

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

10.1 Key trends

10.2 Residential

10.3 Industrial

10.4 Commercial

10.4.1 BFSI

10.4.2 Education

10.4.3 Government

10.4.4 Healthcare

10.4.5 Hospitality

10.4.6 Retail

10.4.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

11.1 Key trends

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.3 Europe

11.3.1 Germany

11.3.2 UK

11.3.3 France

11.3.4 Spain

11.3.5 Italy

11.3.6 Netherlands

11.4 Asia Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 Australia

11.4.5 South Korea

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.6 Middle East and Africa

11.6.1 Saudi Arabia

11.6.2 South Africa

11.6.3 UAE

Chapter 12 Company Profiles

12.1 Apollo Fire Detectors Ltd.

12.2 Electro Detectors Ltd.

12.3 EMS Security Group

12.4 EuroFyre Ltd.

12.5 Gentex Corporation

12.6 Halma PLC (Apollo, Advanced, etc.)

12.7 Hochiki Corporation

12.8 Honeywell International Inc.

12.9 Johnson Controls International plc (Tyco / SimplexGrinnell)