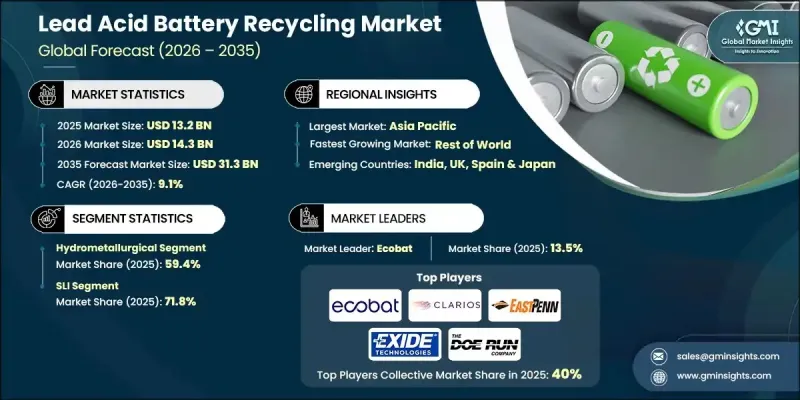

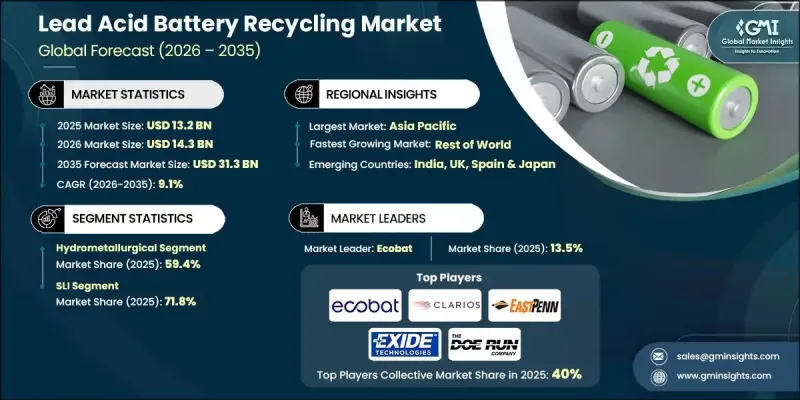

세계의 납축전지 재활용 시장은 2025년에 132억 달러로 평가되며, 2035년까지 CAGR 9.1%로 성장하며, 313억 달러에 달할 것으로 예측됩니다.

전기화 추세의 가속화와 운송, 에너지 저장 및 산업 시스템에서 납축전지의 사용 증가가 이러한 성장을 주도하고 있습니다. 납축전지 재활용은 사용한 배터리를 체계적으로 회수 및 처리하여 납, 플라스틱 부품, 전해액 등 재사용 가능한 물질을 회수하는 과정입니다. 이러한 노력은 자원 효율성 향상, 환경 리스크 감소 및 세계 지속가능성 목표와의 정합성을 지원합니다. 재활용 프로세스는 오염을 줄이고, 안전한 폐기물 처리를 보장하며, 진화하는 컴플라이언스 요건에 대응하는 데 있으며, 중요한 역할을 합니다. 배터리 소비량 증가와 환경 감시 강화가 결합되어 전 세계에서 재활용 활동이 가속화되고 있습니다. 정부와 규제기관은 체계적인 배터리 폐기물 관리 방식을 강화하고, 장기적인 시장 성장을 지원하는 프레임워크를 구축하는 한편, 여러 최종 사용 산업에서 순환 경제의 도입을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2025년 |

| 예측연도 | 2026-2035 |

| 개시시 가치 | 132억 달러 |

| 예측 금액 | 313억 달러 |

| CAGR | 9.1% |

자동차, 전원 백업 시스템, 산업 인프라에 납축전지 도입이 증가함에 따라 재활용량이 크게 증가하고 있습니다. 에너지 저장 수요의 확대에 따라 재활용은 재료 공급망의 중요한 요소로 신규 채굴 자원에 대한 의존도를 낮추는 데 기여하고 있습니다. 환경 보호와 재료 회수에 초점을 맞춘 규제 프레임워크는 제조업체와 재활용업체가 책임감 있는 폐배터리 관리 방법을 지속적으로 추진하도록 장려하고 있습니다.

습식 야금 재활용 분야는 2025년 59.4%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 9.2%로 확대될 것으로 예측됩니다. 이 방식은 다른 재활용 공정에 비해 배출량이 적고, 폐기물 발생량이 적으며, 에너지 요구량이 낮기 때문에 점점 더 많이 선택되고 있습니다. 환경 규제 준수를 지원하면서 고순도 금속 회수를 실현할 수 있는 능력은 지속가능한 운영에 중점을 둔 재활용 사업자에게 중요한 기술 선택이 되고 있습니다.

SLI 부문은 2025년 71.8%의 점유율을 차지할 것으로 예상되며, 2026-2035년 연평균 복합 성장률(CAGR) 9%를 보일 것으로 예측됩니다. 자동차 부문의 지속적인 수요와 안정적인 교체 주기가 일관된 재활용량을 지원하고 있습니다. 배터리 폐기에 대한 환경 규제가 강화됨에 따라 이 응용 분야에서 책임감 있는 회수 방법과 재료 재사용이 더욱 촉진되고 있습니다.

북미 납축전지 재활용 시장은 92.3%의 점유율을 차지하며 2035년까지 43억 달러 규모로 성장할 것으로 예측됩니다. 엄격한 환경 규제 시행, 에너지 저장 수요 증가, 납 노출로 인한 건강 위험 감소에 대한 관심 증가, 첨단 재활용 방법 및 운영 효율성 향상에 대한 관심이 증가하고 있습니다.

The Global Lead Acid Battery Recycling Market was valued at USD 13.2 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 31.3 billion by 2035.

Rising electrification trends and the increasing use of lead acid batteries across transportation, energy storage, and industrial systems drive this growth. Lead acid battery recycling involves the systematic collection and processing of spent batteries to recover reusable materials such as lead, plastic components, and electrolyte solutions. This approach supports resource efficiency, reduces environmental risks, and aligns with global sustainability objectives. The recycling process plays a critical role in reducing pollution, ensuring safe waste handling, and meeting evolving compliance requirements. Growing battery consumption, combined with stronger environmental oversight, is accelerating recycling activity worldwide. Governments and regulatory bodies are reinforcing structured battery waste management practices, creating a supportive framework for long-term market growth and encouraging circular economy adoption across multiple end-use industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.2 Billion |

| Forecast Value | $31.3 Billion |

| CAGR | 9.1% |

Rising deployment of lead-acid batteries in vehicles, power backup systems, and industrial infrastructure is significantly increasing recycling volumes. As energy storage demand grows, recycling is becoming an essential component of material supply chains, helping reduce dependency on newly mined resources. Regulatory frameworks focused on environmental protection and material recovery continue to push manufacturers and recyclers toward responsible end-of-life battery management practices.

The hydrometallurgical recycling segment held 59.4% share in 2025 and is projected to grow at a CAGR of 9.2% through 2035. This method is gaining preference due to its lower emissions, reduced waste generation, and lower energy requirements when compared to alternative recycling processes. Its ability to deliver high-purity metal recovery while supporting environmental compliance has made it a key technology choice for recyclers focused on sustainable operations.

The SLI segment held a 71.8% share in 2025 and is expected to grow at a CAGR of 9% from 2026 to 2035. Continued demand from the automotive sector and steady replacement cycles are supporting consistent recycling volumes. Strengthening environmental rules surrounding battery disposal is further reinforcing responsible recovery practices and material reuse for this application segment.

North America Lead Acid Battery Recycling Market held 92.3% share and is projected to generate USD 4.3 billion by 2035. Strict environmental enforcement, rising energy storage needs, and increased focus on reducing health risks associated with lead exposure are supporting advanced recycling practices and operational efficiency.

Prominent companies active in the Global Lead Acid Battery Recycling Market include Ecobat, Exide Technologies, Glencore, EnerSys, Clarios, Aqua Metals, Gravita India, Gopher Resource LLC, Cirba Solutions, East Penn Manufacturing Company, Interstate Batteries, Engitec Technologies, Doe Run Company, Amara Raja, Battery Recyclers of America, GME Recycling, and BPL Nigeria Limited. These participants continue to shape market dynamics through capacity expansion, technology upgrades, and strategic partnerships. Companies in the Global Lead Acid Battery Recycling Market are strengthening their competitive position through investments in cleaner recycling technologies and process optimization. Many players are focusing on expanding recycling capacity to meet rising battery disposal volumes while improving recovery efficiency. Vertical integration across collection, processing, and material reuse is being adopted to secure supply chains and control costs. Firms are also prioritizing compliance-driven innovation to meet tightening environmental standards.