식품 캡슐화 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2026-2035년)

Food Encapsulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913334

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

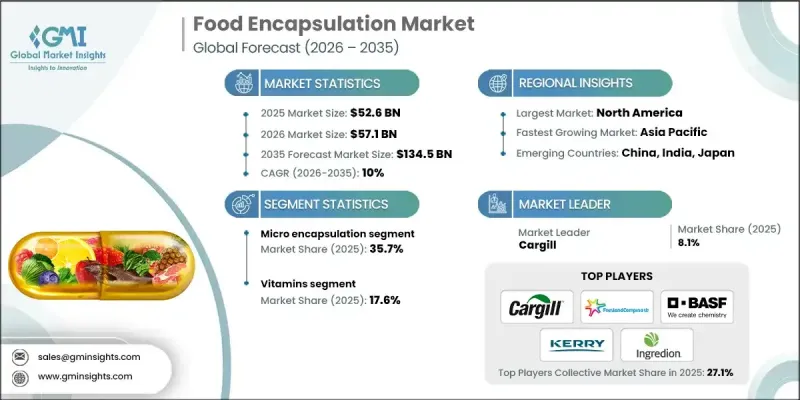

세계의 식품 캡슐화 시장은 2025년에 526억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 10%로 성장할 전망이며, 1,345억 달러에 이를 것으로 예측되고 있습니다.

시장 성장은 제조업체가 제품의 안정성, 관능 품질 및 영양가 향상에 주력하는 동안 여러 식품 카테고리에서 캡슐화의 활용을 확대함으로써 추진되고 있습니다. 캡슐화 기술은 시각적 매력, 풍미 보유 및 맛의 일관성을 개선하기 위해 점점 적용되고 포장 식품에 대한 소비자의 수용성을 향상시키고 있습니다. 감미료 배합에서 캡슐화된 원료의 이용 증가는 원료 혁신 및 식품 보존 조사에 대한 지속적인 투자에 힘입어 보다 광범위한 채용에 기여하고 있습니다. 영양에 대한 소비자 의식 증가와 강화 식품과 부가가치 식품에 대한 수요 증가가 함께 시장 확대를 지속적으로 지원하고 있습니다. 민감하고 휘발성이 높은 식품 성분을 보호할 필요성으로 인해 고급 캡슐화 솔루션에 대한 수요가 커지고 있습니다. 현대 보존 기술의 급속한 보급으로 원료 보호 및 보존 기간 성능이 더욱 향상되었습니다. 동시에, 서방 메커니즘의 진보는 기능성과 건강 효과 향상을 통해 자사 제품의 차별화를 도모하는 생산자에게 매력적인 성장 기회를 창출하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 시 가치

526억 달러

예측 금액

1,345억 달러

CAGR

10%

마이크로 캡슐화 부문은 보호 코팅 기술에 의한 민감한 성분의 보호 효과 및 다양한 식품 처방에 대한 적응성에 의해 2025년에 35.7%의 점유율을 차지했습니다.

비타민 부문은 영양 강화에 대한 관심 증가와 장기적인 건강 및 생리 기능 유지에서 비타민의 역할이 견인하여 2025년에 17.6%의 점유율을 차지했습니다.

북미의 식품 캡슐화 시장은 성숙한 포장 식품 산업, 캡슐화 재료의 풍부한 공급, 첨단 보존 기술의 지속적인 채용에 힘입어 2025년에 36.6%의 점유율을 차지했습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 위험 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

향후 시장 동향

기술 및 혁신 동향

현재 기술 동향

신흥 기술

특허 상황

무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

주요 수입국

주요 수출국

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획

제5장 시장 추계 및 예측 : 유형별(2022-2035년)

마이크로 캡슐화

나노 캡슐화

하이브리드 기술

매크로 캡슐화

제6장 시장 추계 및 예측 : 코어 페이즈별(2022-2035년)

비타민

지용성 비타민

비타민 A

비타민 D

비타민 E

비타민 K

수용성 비타민

비타민 B 복합체

비타민 C

유기산

구연산

젖산

푸마르산

사과산

기타

미네랄

효소

향료 및 에센스

보존료

감미료

착색료

프리바이오틱스

프로바이오틱스

정유

기타

제7장 시장 추계 및 예측 : 기술별(2022-2035년)

물리적 프로세스

분무

분무 건조

분무 냉각

스피닝 디스크

압출법

유동층 기술

기타

화학적 및 물리화학적 공정

제8장 시장 추계 및 예측 : 쉘 재료별(2022-2035년)

다당류

단백질

지질

유화제

기타

제9장 시장 추계 및 예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Cargill

FrieslandCampina Kievit

Royal DSM

BASF SE

Kerry Group

Ingredion Incorporated

Lycored Group

International Flavours & Fragrances Inc.(IFF)

Symrise AG

Sensient Technologies Corporation

Balchem Corporation

Firmenich SA

AVEKA Group

AJY

영문 목차

영문목차

The Global Food Encapsulation Market was valued at USD 52.6 billion in 2025 and is estimated to grow at a CAGR of 10% to reach USD 134.5 billion by 2035.

Market growth is fueled by the widening use of encapsulation across multiple food categories, as manufacturers focus on enhancing product stability, sensory quality, and nutritional value. Encapsulation technologies are increasingly applied to improve visual appeal, flavor retention, and taste consistency, which supports stronger consumer acceptance of packaged foods. Rising utilization of encapsulated ingredients in sweetener formulations is contributing to broader adoption, supported by continuous investments in ingredient innovation and food preservation research. Growing consumer awareness regarding nutrition, combined with higher demand for fortified and value-added food products, continues to support market expansion. The need to safeguard sensitive and volatile food components has strengthened demand for advanced encapsulation solutions. Rapid adoption of modern preservation techniques is further improving ingredient protection and shelf-life performance. At the same time, advancements in controlled-release mechanisms are creating attractive growth opportunities for producers seeking to differentiate their offerings through functional performance and enhanced health benefits.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$52.6 Billion

Forecast Value

$134.5 Billion

CAGR

10%

The microencapsulation segment accounted for 35.7% share in 2025, supported by its effectiveness in protecting sensitive ingredients through protective coating methods and its adaptability across diverse food formulations.

The vitamins segment held 17.6% share in 2025, driven by rising interest in nutritional enrichment and the role of vitamins in supporting long-term health and physiological functions.

North America Food Encapsulation Market held 36.6% share in 2025, supported by a mature packaged food industry, strong availability of encapsulation materials, and ongoing adoption of advanced preservation technologies.

Key companies operating in the Global Food Encapsulation Market include Ingredion Incorporated, Kerry Group, Symrise AG, Balchem Corporation, Cargill, Sensient Technologies Corporation, International Flavours & Fragrances Inc. (IFF), FrieslandCampina Kievit, BASF SE, Lycored Group, AVEKA Group, Royal DSM, and Firmenich SA. Companies in the Global Food Encapsulation Market are reinforcing their market position by investing heavily in research and development to improve encapsulation efficiency, stability, and controlled-release performance. Strategic partnerships with food manufacturers allow suppliers to co-develop customized solutions tailored to specific formulation needs. Expansion of production capacities and geographic presence helps companies meet rising global demand while improving supply reliability. Firms are also focusing on clean-label and health-oriented innovations to align with evolving consumer preferences.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Core phase

2.2.4 Technology

2.2.5 Shell material

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion & Tons)

5.1 Key trends

5.2 Micro encapsulation

5.3 Nano encapsulation

5.4 Hybrid technology

5.5 Macro encapsulation

Chapter 6 Market Estimates and Forecast, By Core Phase, 2022-2035 (USD Billion & Tons)

6.1 Key trends

6.2 Vitamins

6.2.1 Fat soluble vitamins

6.2.1.1 Vitamin A

6.2.1.2 Vitamin D

6.2.1.3 Vitamin E

6.2.1.4 Vitamin K

6.2.2 Water soluble vitamins

6.2.2.1 Vitamin B complex

6.2.2.2 Vitamin C

6.3 Organic acids

6.3.1 Citric acid

6.3.2 Lactic acid

6.3.3 Fumaric acid

6.3.4 Malic acid

6.3.5 Others

6.4 Minerals

6.5 Enzymes

6.6 Flavors & essences

6.7 Preservatives

6.8 Sweeteners

6.9 Colors

6.10 Prebiotics

6.11 Probiotics

6.12 Essential oils

6.13 Others

Chapter 7 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion & Tons)

7.1 Key trends

7.2 Physical process

7.2.1 Atomization

7.2.1.1 Spray drying

7.2.1.2 Spray chilling

7.2.1.3 Spinning disk

7.2.2 Extrusion

7.2.3 Fluid bed technique

7.2.4 Others

7.3 Chemical & physicochemical process

Chapter 8 Market Estimates and Forecast, By Shell Material, 2022-2035 (USD Billion & Tons)

8.1 Key trends

8.2 Polysaccharides

8.3 Proteins

8.4 Lipids

8.5 Emulsifiers

8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion & Tons)

9.1 Key trends

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 France

9.3.4 Spain

9.3.5 Italy

9.3.6 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 India

9.4.3 Japan

9.4.4 Australia

9.4.5 South Korea

9.4.6 Rest of Asia Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.5.4 Rest of Latin America

9.6 Middle East and Africa

9.6.1 Saudi Arabia

9.6.2 South Africa

9.6.3 UAE

9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

10.1 Cargill

10.2 FrieslandCampina Kievit

10.3 Royal DSM

10.4 BASF SE

10.5 Kerry Group

10.6 Ingredion Incorporated

10.7 Lycored Group

10.8 International Flavours & Fragrances Inc. (IFF)