Cryogenic Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892907

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 135 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

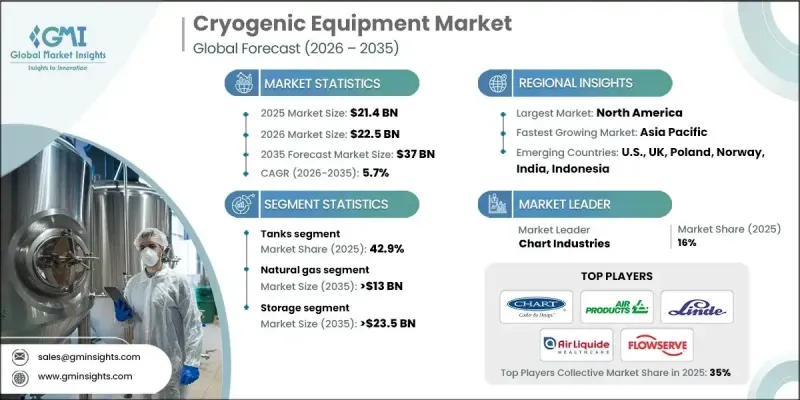

세계의 극저온 장비 시장은 2025년에 214억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 5.7%를 나타내 370억 달러에 이를 것으로 예측됩니다.

시장 성장은 천연 가스 저장을 위한 첨단 액화 시스템의 채택 확대와 저온 작동을 최적화하는 자동 밸브 조립체의 통합 증가에 의해 견인되고 있습니다. LNG 벙커링용 극저온 펌프의 도입 확대와 해운 분야 전체에서의 배출 감축 이니셔티브가 결합되어 설계상의 우선사항을 형성하고 있습니다. 극저온 장비는 질소, 산소, 수소, 헬륨, 천연 가스와 같은 가스를 액화하는 데 필수적인 극저온 환경에서 물질을 제조, 취급, 저장, 운송하는 특수 장비 및 시스템을 의미합니다. 진공 단열 배관, 모듈식 극저온 탱크, 스키드 마운트 시스템의 채용 확대에 의해 효율성과 유연성이 향상되고 있는 한편, IoT 대응 센서나 예지 보전 툴이 운용 신뢰성을 높이고 있습니다. 산업 및 석유화학 응용 분야에서 극저온 기화기, 컴프레서 및 유연한 용량 솔루션의 활용 증가는 설치 기술을 재정의하고 초저온 작동에서 혁신의 기회를 창출하고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 가치

214억 달러

예측 금액

370억 달러

CAGR

5.7%

밸브 부문은 스테인레스 스틸 및 니켈 합금의 채택 추세와 엄격한 성능 기준에 대한 적합성을 바탕으로 2035년까지 40억 달러 규모에 이를 것으로 예측됩니다. 제로 방출 운전에 중점을 둔 첨단 밸브 설계는 지속가능성 목표에 부합하며 극저온 유체의 보다 안전하고 효율적인 취급을 가능하게 합니다.

산소 부문은 2035년까지 연평균 복합 성장률(CAGR) 5.5%를 나타낼 것으로 예상됩니다. 산소 기화기 및 대용량 저장 시스템의 채택 확대는 항공우주 연료 공급 용도를 포함한 산업 공정을 지원합니다. 산소 극저온 펌프의 통합은 정밀하고 신뢰할 수 있는 저온 관리를 필요로 하는 틈새 응용 분야를 더욱 추진하고 있습니다.

미국의 극저온 장비 시장은 2025년 42억 달러를 창출해 85.7%의 점유율을 차지했습니다. 극저온 탱크의 적극적인 도입과 피크 면도 장비의 조합은 계절적인 전력 수요 관리를 지원합니다. IoT 대응 극저온 펌프와 예지보전 솔루션의 도입 확대로 스마트하고 자동화된 플랜트 운영이 가능해 업계 전체의 효율성과 안전성이 향상되고 있습니다.

The Global Cryogenic Equipment Market was valued at USD 21.4 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 37 billion by 2035.

Market growth is driven by the increasing adoption of advanced liquefaction systems for natural gas storage and the rising integration of automated valve assemblies that optimize low-temperature operations. The growing deployment of cryogenic pumps for LNG bunkering, coupled with emission reduction initiatives across the marine sector, is shaping design priorities. Cryogenic equipment encompasses specialized devices and systems for producing, handling, storing, and transporting materials at extremely low temperatures, essential for liquefying gases such as nitrogen, oxygen, hydrogen, helium, and natural gas. Rising adoption of vacuum-insulated piping, modular cryogenic tanks, and skid-mounted systems is enhancing efficiency and flexibility, while IoT-enabled sensors and predictive maintenance tools are improving operational reliability. Increasing utilization of cryogenic vaporizers, compressors, and flexible capacity solutions in industrial and petrochemical applications is redefining installation practices and creating opportunities for innovation in ultra-low temperature operations.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$21.4 Billion

Forecast Value

$37 Billion

CAGR

5.7%

The valves segment is expected to reach USD 4 billion by 2035, driven by a preference for stainless steel and nickel alloys and adherence to stringent performance standards. Advanced valve designs focused on zero-emission operations are aligning with sustainability objectives, enabling safer and more efficient handling of cryogenic fluids.

The oxygen segment is projected to grow at a CAGR of 5.5% by 2035. Rising adoption of oxygen vaporizers and high-capacity storage systems is supporting industrial processes, including aerospace fueling applications. Integration of oxygen cryogenic pumps is further driving niche applications that demand precise and reliable low-temperature management.

U.S. Cryogenic Equipment Market held 85.7% share, generating USD 4.2 billion in 2025. Strong adoption of cryogenic tanks, coupled with peak shaving facilities, supports seasonal power demand management. Increasing deployment of IoT-enabled cryogenic pumps and predictive maintenance solutions is enabling smart and automated plant operations, improving efficiency and safety across the industry.

Major players active in the Global Cryogenic Equipment Market include Emerson Electric, Air Liquide, Chart Industries, Flowserve Corporation, Linde, Cryostar, Air Products and Chemicals, Kelvin International, IWI Cryogenic Vaporization Systems (India) Pvt. Ltd., Cryogas Equipment, CRYOSPAIN, BRUGG Pipes, Abhijit Enterprises, Cryoworld, Shell-n-Tube, Demaco, AIR WATER, Auguste Cryogenics, SLB, Cryogenic OGS, and Vacuum Barrier. Companies in the Cryogenic Equipment Market are focusing on multiple strategies to enhance their market presence and strengthen their competitive position. Key approaches include investing in R&D to develop next-generation, energy-efficient, and modular cryogenic solutions. Firms are pursuing strategic partnerships, joint ventures, and acquisitions to expand geographic reach and technological capabilities. Product differentiation through advanced materials, automated valve assemblies, and IoT-enabled monitoring systems is being emphasized to meet industry-specific requirements.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates and calculations

1.2.1 Base year calculation

1.2.2 Market estimates & forecast parameters

1.3 Forecast

1.3.1 Key trends for market estimates

1.3.2 Quantified market impact analysis

1.3.2.1 Mathematical impact of growth parameters on forecast

1.3.3 Scenario analysis framework

1.4 Primary research and validation

1.4.1 Some of the primary sources (but not limited to)

1.5 Data mining sources

1.5.1 Paid Sources

1.5.2 Sources, by region

1.6 Research trail & scoring components

1.6.1 Research trail components

1.6.2 Scoring components

1.7 Research transparency addendum

1.7.1 Source attribution framework

1.7.2 Quality assurance metrics

1.7.3 Our commitment to trust

1.8 Market definitions

Chapter 2 Executive Summary

2.1 Industry synopsis, 2022 - 2035

2.2 Business trends

2.3 Product trends

2.4 Cryogen type trends

2.5 Application trends

2.6 End use trends

2.7 Regional trends

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Raw material availability & sourcing analysis

3.1.2 Manufacturing capacity assessment

3.1.3 Supply chain resilience & risk factors

3.1.4 Distribution network analysis

3.2 Regulatory landscape

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.2 Industry pitfalls & challenges

3.4 Growth potential analysis

3.5 Porter's analysis

3.5.1 Bargaining power of suppliers

3.5.2 Bargaining power of buyers

3.5.3 Threat of new entrants

3.5.4 Threat of substitutes

3.6 PESTEL analysis

3.6.1 Political factors

3.6.2 Economic factors

3.6.3 Social factors

3.6.4 Technological factors

3.6.5 Legal factors

3.6.6 Environmental factors

3.7 Cost structure analysis of cryogenic equipment

3.8 Emerging opportunities & trends

3.9 Digitalization and IoT integration

3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis, by region, 2025

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.2.4 Middle East & Africa

4.2.5 Latin America

4.3 Strategic dashboard

4.3.1 Key partnerships & collaborations

4.3.2 Major M&A activities

4.3.3 Product innovations & launches

4.3.4 Market expansion strategies

4.4 Strategic initiatives

4.5 Competitive benchmarking

4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million)

5.1 Key trends

5.2 Tanks

5.3 Valves

5.4 Vaporizers

5.5 Pumps

5.6 Pipe

5.7 Others

Chapter 6 Market Size and Forecast, By Cryogen Type, 2022 - 2035 (USD Million)

6.1 Key trends

6.2 Nitrogen

6.3 Oxygen

6.4 Natural gas

6.5 Argon

6.6 Other cryogens

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

7.1 Key trends

7.2 Storage

7.3 Distribution

Chapter 8 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

8.1 Key trends

8.2 O&G industry

8.3 Power

8.4 Food & beverage

8.5 Chemical

8.6 Rubber & plastics

8.7 Metallurgy

8.8 Healthcare

8.9 Shipping

8.10 Agriculture, forestry & fishing

8.11 Other industries

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

9.1 Key trends

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.2.3 Mexico

9.3 Europe

9.3.1 UK

9.3.2 Germany

9.3.3 Italy

9.3.4 Spain

9.3.5 France

9.3.6 Poland

9.3.7 Norway

9.3.8 Netherlands

9.4 Asia Pacific

9.4.1 China

9.4.2 India

9.4.3 Japan

9.4.4 Indonesia

9.4.5 Thailand

9.4.6 Malaysia

9.4.7 Philippines

9.4.8 South Korea

9.4.9 Australia

9.5 Middle East & Africa

9.5.1 Saudi Arabia

9.5.2 UAE

9.5.3 Kuwait

9.5.4 Oman

9.5.5 Turkey

9.5.6 Qatar

9.5.7 Egypt

9.5.8 South Africa

9.6 Latin America

9.6.1 Brazil

9.6.2 Argentina

9.6.3 Peru

Chapter 10 Company Profiles

10.1 Abhijit Enterprises

10.2 Air Liquide

10.3 Air Products and Chemicals

10.4 AIR WATER

10.5 Auguste Cryogenics

10.6 BRUGG Pipes

10.7 Chart Industries

10.8 Cryogas Equipment

10.9 Cryogenic OGS

10.10 CRYOSPAIN

10.11 Cryostar

10.12 Cryoworld

10.13 Demaco

10.14 Emerson Electric

10.15 Flowserve Corporation

10.16 Hypro

10.17 INOXCVA

10.18 IWI Cryogenic Vaporization Systems (India) Pvt. Ltd.