Analytical Instrumentation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892898

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 208 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

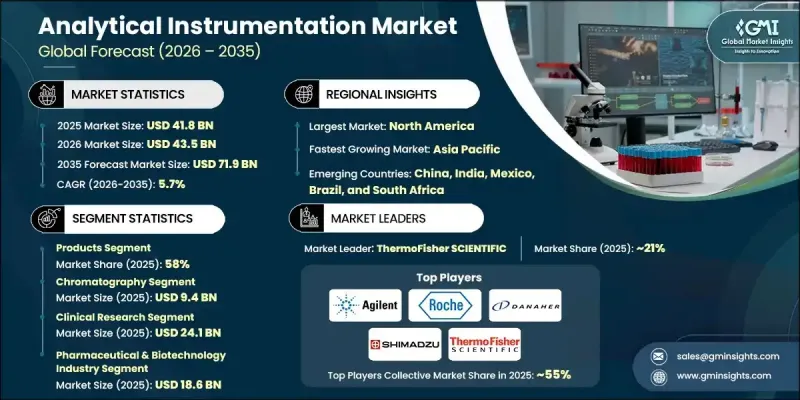

세계의 분석 기기 시장은 2025년 418억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 5.7%를 나타내 719억 달러에 이를 것으로 예측됩니다.

이 성장은 제약 및 바이오테크놀러지 분야에서의 R&D 투자 증가, 정밀의료용 분석 시스템의 보급 확대, 만성 질환·감염증의 만연, 검증된 분석 프로토콜에 준거를 촉진하는 규제 요건에 의해 추진되고 있습니다. 분석 기기는 실험실에서 고정밀 측정, 실시간 모니터링 및 고급 데이터 분석을 실현하여 증거 기반 임상 판단 및 최적화된 치료 전략을 지원합니다. 임상실, 기준검사기관, 조사에서 높은 처리량과 고감도 검사에 대한 수요가 증가함에 따라 이러한 시스템의 도입이 더욱 가속화되고 있습니다. 불순물 프로파일링, 생물학적 제형의 특성화, 배치 릴리즈 및 안정성 시험에 필수적인 이러한 장비는 과학자와 임상의가 시료의 화학적, 물리적, 분자적 특성을 비교할 수 없는 정확도로 분석할 수 있게 해주며 의료, 제약 및 산업 분야에서 매우 중요합니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 가치

418억 달러

예측 금액

719억 달러

CAGR

5.7%

제품 부문은 제약 연구 개발, 진단 및 산업 시험에서 고급 장비에 대한 강한 수요에 견인되어 2025년에 58%의 점유율을 차지했습니다. 이러한 이점은 지속적인 기술 혁신과 정밀하고 처리량이 높은 분석 도구에 대한 수요 증가로 더욱 강화되고 있습니다.

크로마토그래피 부문은 복잡한 화학 혼합물을 정확하게 분리, 확인 및 정량하는 능력을 통해 2025년에 94억 달러 시장 규모를 창출했습니다. 연구소에서는 품질 관리, 제제 개발, 안정성 시험, 불순물 프로파일링에 있어서 크로마토그래피에 크게 의존하고 있어 연구 집약형 워크플로우에 있어서 핵심적인 역할이 확고한 것이 되고 있습니다.

미국의 분석 기기 시장은 2025년 146억 달러에 달했고, 2035년까지 연평균 복합 성장률(CAGR) 5.8%를 나타낼 것으로 전망됩니다. 이 주도적 지위는 성숙한 제약, 생명공학, 임상 진단 생태계, 첨단 실험실 인프라, 엄격한 규제 요건에 기인합니다. FDA, USP, CDC, CMS/CLIA 등의 기관은 의약품 개발, 생물학적 제제 제조, 임상 진단에 있어서 엄격한 분석적 검증을 의무화하고 있으며, 연구 개발, 품질 관리, 임상 실험실에서 크로마토그래피, 분광법, 질량 분석, 분자 분석 플랫폼, 입자 특성 평가 툴을 포함한 고정밀 기기에 대한 지속적인 수요를 견인하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

제약업계 및 정부계 연구기관에 의한 연구개발비 증가

분석기기의 기술적 진보

정밀의료 용도용 분석 기기의 도입 확대

정확한 검사를 필요로 하는 만성 질환 및 감염증 증가 경향

규제 준수가 검증된 분석 시스템의 도입을 촉진

분자진단 및 PCR 기반 플랫폼의 확대에 의한 조기 검출

업계의 잠재적 위험 및 과제

기기의 고비용

숙련된 전문가의 부족

시장 기회

포인트 오브 케어 검사의 성장

창약·개발 활동의 급증

성장 가능성 분석

밸류체인 분석

파이프라인 분석

지역별 가격 분석(2025년)

수량 분석(2022-2035년)

향후 시장 동향

규제 상황

기술 동향

현행 기술

신흥 기술

갭 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업 매트릭스 분석

기업의 시장 점유율 분석

북미

유럽

아시아태평양

LAMEA

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병

파트너십 및 협력

신제품 출시

확대 계획

제5장 시장 추계·예측 : 제품 및 서비스별(2022-2035년)

제품

크로마토그래피 기기

분광 분석 기기

분자 분석 기기

입자 계수기 및 분석기

전기화학 분석 기기

기타 제품

서비스 및 소모품

제6장 시장 추계·예측 : 기술별(2022-2035년)

크로마토그래피

액체 크로마토그래피

가스 크로마토그래피

이온 크로마토그래피

분광학

중합효소 연쇄 반응

입자 분석

기타 기술

제7장 시장 추계·예측 : 용도별(2022-2035년)

임상 연구

임상 진단

제8장 시장 추계·예측 : 최종 용도별(2022-2035년)

제약 및 바이오테크놀러지 산업

연구 및 학술 기관

진단 센터

기타 최종 용도

제9장 시장 추계·예측 : 지역별(2022-2035년)

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

폴란드

스웨덴

네덜란드

아시아태평양

중국

일본

인도

호주

한국

태국

인도네시아

필리핀

라틴아메리카

브라질

멕시코

아르헨티나

콜롬비아

칠레

페루

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

이스라엘

튀르키예

이란

제10장 기업 프로파일

Agilent

Avantor

BIO RAD

BRUKER

Danaher

Eppendorf

HITACHI

Illumina

Malvern Panalytical(Spectris)

METTLER TOLEDO

Metrohm AG

Revvity

Roche

SARTORIUS

SHIMADZU

ThermoFisher SCIENTIFIC

Waters

ZEISS

KTH

영문 목차

영문목차

The Global Analytical Instrumentation Market was valued at USD 41.8 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 71.9 billion by 2035.

The growth is fueled by increased R&D investments in the pharmaceutical and biotech sectors, rising adoption of analytical systems for precision medicine, the growing prevalence of chronic and infectious diseases, and regulatory mandates driving compliance with validated analytical protocols. Analytical instrumentation enables laboratories to deliver highly accurate measurements, real-time monitoring, and advanced data analytics, supporting evidence-based clinical decision-making and optimized treatment strategies. The rising demand for high-throughput, sensitive testing in clinical, reference, and research laboratories is further accelerating the adoption of these systems, which are essential for impurity profiling, biologics characterization, batch release, and stability testing. These instruments allow scientists and clinicians to analyze chemical, physical, and molecular properties of samples with unmatched precision, making them critical across healthcare, pharmaceutical, and industrial applications.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$41.8 Billion

Forecast Value

$71.9 Billion

CAGR

5.7%

The products segment held 58% share in 2025, driven by strong demand for advanced instruments in pharmaceutical R&D, diagnostics, and industrial testing. This dominance is reinforced by continuous technological innovation and the growing need for precise, high-throughput analytical tools.

The chromatography segment generated USD 9.4 billion in 2025, due to its ability to separate, identify, and quantify complex chemical mixtures accurately. Laboratories heavily rely on chromatography for quality control, formulation development, stability testing, and impurity profiling, solidifying its central role in research-intensive workflows.

U.S. Analytical Instrumentation Market reached USD 14.6 billion in 2025 and is expected to grow at a CAGR of 5.8% through 2035. This leadership stems from a mature pharmaceutical, biotechnology, and clinical diagnostics ecosystem, advanced laboratory infrastructure, and stringent regulatory requirements. Agencies such as the FDA, USP, CDC, and CMS/CLIA enforce rigorous analytical validation for drug development, biologics manufacturing, and clinical diagnostics, driving sustained demand for high-precision instruments, including chromatography, spectroscopy, mass spectrometry, molecular analysis platforms, and particle characterization tools across research, quality control, and clinical laboratories.

Key players in the Global Analytical Instrumentation Market include Bruker, Waters, Eppendorf, Agilent, Illumina, Avantor, Revvity, Shimadzu, METTLER TOLEDO, Bio-Rad, Malvern Panalytical (Spectris), Roche, Sartorius, Hitachi, ThermoFisher Scientific, Metrohm AG, Zeiss, and Danaher. To strengthen their Analytical Instrumentation Market position, companies are focusing on product innovation, expanding instrument portfolios, and integrating advanced technologies such as AI, IoT, and automation into their analytical platforms. Strategic collaborations with pharmaceutical, biotech, and research institutions help accelerate the adoption of cutting-edge systems. Firms are investing in digital services, predictive maintenance, and cloud-enabled analytics to improve workflow efficiency and uptime. Global expansion into emerging markets, targeted marketing campaigns, and customized solutions for clinical, industrial, and research applications further reinforce brand presence and foster long-term client relationships.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Product & services trends

2.2.3 Technology trends

2.2.4 Application trends

2.2.5 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising R&D spending by the pharmaceutical industry and government research organizations

3.2.1.2 Technological advancements in analytical instruments

3.2.1.3 Increasing adoption of analytical instrumentation for precision medicine applications

3.2.1.4 Growing prevalence of chronic and infectious diseases requiring accurate testing

3.2.1.5 Regulatory compliance driving adoption of validated analytical systems

3.2.1.6 Expansion of molecular diagnostics and PCR-based platforms for early detection

3.2.2 Industry pitfalls & challenges

3.2.2.1 High cost of instruments

3.2.2.2 Lack of skilled professionals

3.2.3 Market opportunities

3.2.3.1 Growth in point-of-care testing

3.2.3.2 Surge in drug discovery and development activities

3.3 Growth potential analysis

3.4 Value chain analysis

3.5 Pipeline analysis

3.6 Pricing analysis, by region, 2025

3.6.1 North America

3.6.2 Europe

3.6.3 Asia Pacific

3.6.4 Latin America

3.6.5 MEA

3.7 Volume analysis, 2022 - 2035

3.7.1 North America

3.7.2 Europe

3.7.3 Asia Pacific

3.7.4 Latin America

3.7.5 MEA

3.8 Future market trends

3.9 Regulatory landscape

3.10 Technology landscape

3.10.1 Current technologies

3.10.2 Emerging technologies

3.11 Gap analysis

3.12 Porter's analysis

3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis

4.3.1 North America

4.3.2 Europe

4.3.3 Asia Pacific

4.3.4 LAMEA

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product & Services, 2022 - 2035 ($ Mn)

5.1 Key trends

5.2 Products

5.2.1 Chromatography instruments

5.2.2 Spectroscopy instruments

5.2.3 Molecular analysis instruments

5.2.4 Particle counters and analyzers

5.2.5 Electrochemical analysis instruments

5.2.6 Other products

5.3 Services & consumables

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 ($ Mn)

6.1 Key trends

6.2 Chromatography

6.2.1 Liquid chromatography

6.2.2 Gas chromatography

6.2.3 Ion chromatography

6.3 Spectroscopy

6.4 Polymerase chain reaction

6.5 Particle analysis

6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

7.1 Key trends

7.2 Clinical research

7.3 Clinical diagnostics

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

8.1 Key trends

8.2 Pharmaceutical & biotechnology industry

8.3 Research and academic institutes

8.4 Diagnostic centers

8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)