동물사료용 프로바이오틱스 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)

Animal Feed Probiotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892858

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

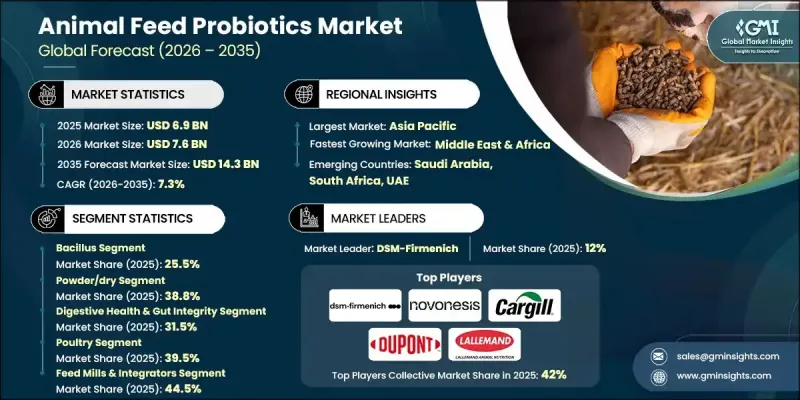

세계의 동물사료용 프로바이오틱스 시장은 2025년에 69억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.3%로 성장하여 143억 달러에 이를 것으로 예측됩니다.

이러한 성장은 동물 영양학에서 항생제 사용을 제한하는 규정의 변화로 뒷받침되고 있으며, 생산자들이 대체 건강 관리 방법을 채택하도록 장려하고 있습니다. 사료 제조업체들은 장내 균형과 동물의 종합적인 성능을 지원하는 영양 기반 솔루션에 대한 의존도를 높이고 있습니다. 프로바이오틱스는 의료적으로 중요한 화합물에 의존하지 않고 건강 효과를 향상시키는 미생물 군집에 초점을 맞춘 성분으로 이러한 전환의 필수적인 요소입니다. 전 세계 사료 생산 규모가 매우 크기 때문에 도입 수준이 낮더라도 큰 영향을 미칠 수 있습니다. 시장에서의 수용성은 생산 시스템 전체에서 관찰되는 일관된 성능 향상(성장 효율 향상, 질병 압력 감소, 생산 품질 개선 등)에 의해 강화되고 있습니다. 이러한 장점은 프로바이오틱스를 사후 대응적 치료 모델이 아닌 예방적 동물 건강 전략으로 자리매김하게 합니다. 지속가능성에 대한 관심도 수요를 더욱 촉진하고 있으며, 프로바이오틱스는 영양 이용 효율을 높이고 환경 부하를 줄이는 데 기여함으로써 생산자가 기후 변화 대응 약속과 진화하는 조달 기준을 충족할 수 있도록 돕습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 시장 규모

69억 달러

예측 금액

143억 달러

CAGR

7.3%

2025년 기준, 바실러스 속 프로바이오틱스 부문은 25.5%의 점유율을 차지하고 있으며, 2035년까지 연평균 6.6%의 성장률을 보일 것으로 예측됩니다. 높은 가공 온도와 까다로운 보관 조건에서도 안정성을 유지하는 특성으로 인해 상업용 사료 제조에 광범위하게 사용되고 있습니다. 이러한 특성은 생산 스트레스 상황에서도 소화 균형과 효소 활성을 유지하는 신뢰할 수 있는 솔루션입니다.

분말 및 건조 제제 부문은 2025년에 38.8%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 6.2%의 성장률을 보일 것으로 예측됩니다. 취급의 용이성, 균일한 혼합성, 장기보관성, 높은 비용효율성으로 대규모 사료사업에서 지속적으로 채택을 촉진하고 있습니다.

북미 동물사료용 프로바이오틱스 시장은 2025년 29%의 점유율을 차지할 것으로 예측됩니다. 선진적인 생산 시스템, 강력한 규제 모니터링, 항생제 무항생제 사료 프로그램의 광범위한 채택이 시장 확대를 뒷받침하고 있습니다. 정밀 영양학 및 지속가능성 이니셔티브에 대한 지역적 리더십은 프로바이오틱스 개발 및 공급 방식에 대한 지속적인 혁신을 촉진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계별 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품 유형별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

주요 동향

바실러스

락토바실러스

사카로마이세스 (효모 기반)

비피도박테리움

엔테로코커스

포스트바이오틱스

스트렙토코커스

기타

제6장 시장 추산 및 예측 : 형태별, 2022-2035

주요 동향

분말/건조 유형

마이크로 캡슐화

액체/수용성

과립

기타

제7장 시장 추산 및 예측 : 기능별, 2022-2035

주요 동향

소화기 건강 및 장관 건전성

면역 지원 및 조절

성장 촉진 및 사료 효율

병원체 제어 및 경쟁 배제

스트레스 관리

기타

제8장 시장 추산 및 예측 : 축산별, 2022-2035

주요 동향

가금류

브로일러

채란계

종축

기타

돼지

새끼 돼지(이유 전 및 이유 후)

성장기 돼지

비육기 돼지

기타

소(반추동물)

젖소

육우

양식업

연어

송어

새우

잉어

기타

반려동물 사료

개

고양이

말

기타

제9장 시장 추산 및 예측 : 유통 채널별, 2022-2035

주요 동향

사료 공장 및 통합 업자

수의용 의약품 도매업체

직접 판매(제조업체로부터 농장에)

온라인/전자상거래

기타

제10장 시장 추산 및 예측 : 최종 용도별, 2022-2035

주요 동향

상업 및 산업형 농장

소규모/가정 채소밭 규모 농업

기타

제11장 시장 추산 및 예측 : 지역별, 2022-2035

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트(UAE)

기타 중동 및 아프리카

제12장 기업 개요

DSM-Firmenich

Chr. Hansen(Novonesis)

Cargill Animal Nutrition

DuPont Nutrition &Biosciences(IFF)

Lallemand Animal Nutrition

Alltech

Kemin Industries

Evonik Industries

Novus International

Lesaffre Group

Angel Yeast

Biomin

Nutreco

MicroSynbiotiX

LSH

영문 목차

영문목차

The Global Animal Feed Probiotics Market was valued at USD 6.9 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 14.3 billion by 2035.

Growth is supported by regulatory shifts that limit the use of antibiotics in animal nutrition, encouraging producers to adopt alternative health management approaches. Feed manufacturers increasingly rely on nutrition-based solutions that support gut balance and overall animal performance. Probiotics have become an integral part of this transition as microbiome-focused ingredients that enhance health outcomes without relying on medically important compounds. Even modest adoption levels have a significant impact due to the sheer scale of global feed production. Market acceptance is reinforced by consistent performance improvements observed across production systems, including better growth efficiency, reduced disease pressure, and improved output quality. These benefits align probiotics with preventive animal health strategies rather than reactive treatment models. Sustainability considerations further strengthen demand, as probiotics support improved nutrient utilization and contribute to lower environmental impact, helping producers meet climate commitments and evolving sourcing standards.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$6.9 Billion

Forecast Value

$14.3 Billion

CAGR

7.3%

The bacillus-based probiotics segment held a 25.5% share in 2025 and is expected to grow at a CAGR of 6.6% through 2035. Their stability under high processing temperatures and challenging storage conditions supports widespread use in commercial feed manufacturing. These characteristics make them a reliable solution for maintaining digestive balance and enzyme activity under production stress.

The powder and dry formulations segment held 38.8% share in 2025 and is forecast to grow at a CAGR of 6.2% from 2026 to 2035. Their ease of handling, uniform blending, long shelf life, and cost efficiency continue to drive adoption across large-scale feed operations.

North America Animal Feed Probiotics Market captured 29% share in 2025. Advanced production systems, strong regulatory oversight, and widespread adoption of antibiotic-free feeding programs continue to support market expansion. Regional leadership in precision nutrition and sustainability initiatives encourages ongoing innovation in probiotic development and delivery.

Key companies operating in the Global Animal Feed Probiotics Market include Chr. Hansen (Novonesis), DSM-Firmenich, Alltech, Cargill Animal Nutrition, Lallemand Animal Nutrition, Evonik Industries, Kemin Industries, DuPont Nutrition & Biosciences (IFF), Nutreco, Novus International, Lesaffre Group, Angel Yeast, Biomin, and MicroSynbiotiX. Companies in the Animal Feed Probiotics Market pursue focused strategies to strengthen their competitive position. Investment in research and strain development remains a priority to enhance efficacy and stability. Manufacturers expand product portfolios to address evolving regulatory and sustainability requirements. Strategic partnerships with feed producers support wider market penetration and application expertise. Firms emphasize quality assurance and traceability to build customer trust. Geographic expansion into high-growth regions improves scale and distribution reach.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product Type

2.2.3 Form

2.2.4 Function

2.2.5 Livestock

2.2.6 Distribution Channel

2.2.7 End Use

2.3 TAM Analysis, 2025-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Science-backed performance gains

3.2.1.2 Stewardship and trade requirements

3.2.1.3 Precision farming & stability tech

3.2.2 Industry pitfalls and challenges

3.2.2.1 Strain variability & dosing

3.2.2.2 Regulatory complexity

3.2.3 Market opportunities

3.2.3.1 Methane and nutrient management

3.2.3.2 Aquaculture and pet nutrition.

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By product type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Bacillus

5.3 Lactobacilli

5.4 Saccharomyces (Yeast-Based)

5.5 Bifidobacterium

5.6 Enterococcus

5.7 Postbiotics

5.8 Streptococcus

5.9 Others

Chapter 6 Market Estimates and Forecast, By Form, 2022-2035 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Powder/Dry

6.3 Microencapsulated

6.4 Liquid/Soluble

6.5 Granules

6.6 Others

Chapter 7 Market Estimates and Forecast, By Function, 2022-2035 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Digestive health & gut integrity

7.3 Immune support & modulation

7.4 Growth promotion & feed efficiency

7.5 Pathogen control & competitive exclusion

7.6 Stress management

7.7 Others

Chapter 8 Market Estimates and Forecast, By Livestock, 2022-2035 (USD Billion) (Kilo Tons)

8.1 Key trends

8.2 Poultry

8.2.1 Broilers

8.2.2 Layers

8.2.3 Breeders

8.2.4 Others

8.3 Swine

8.3.1 Piglets (pre-weaning & post-weaning)

8.3.2 Growers

8.3.3 Finishers

8.3.4 Others

8.4 Cattle (ruminants)

8.4.1 Dairy cattle

8.4.2 Beef cattle

8.5 Aquaculture

8.5.1 Salmon

8.5.2 Trout

8.5.3 Shrimp

8.5.4 Carp

8.5.5 Others

8.6 Pet food

8.6.1 Dogs

8.6.2 Cats

8.7 Equine

8.8 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

9.1 Key trends

9.2 Feed mills & integrators

9.3 Veterinary distributors

9.4 Direct sales (manufacturer to farm)

9.5 Online/e-commerce

9.6 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2022-2035 (USD Billion) (Kilo Tons)

10.1 Key trends

10.2 Commercial/industrial farms

10.3 Small-scale/backyard operations

10.4 Others

Chapter 11 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)