Walk-in Coolers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892825

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

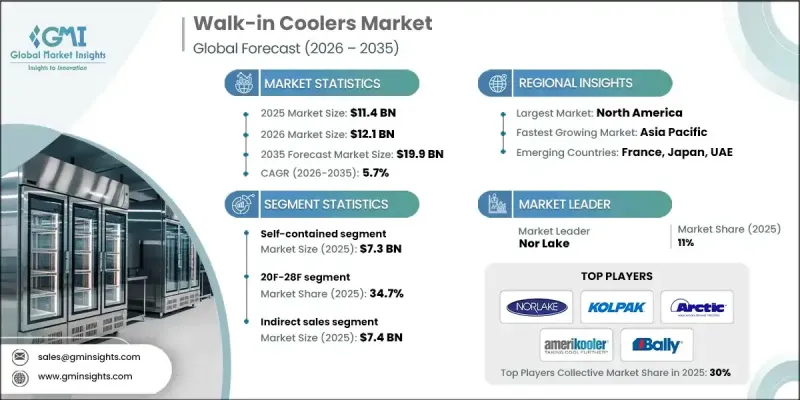

세계의 워크인 쿨러 시장은 2025년에 114억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 5.7%로 성장하여 199억 달러에 이를 것으로 예측됩니다.

육류, 해산물, 유제품 등 신선식품에 대한 수요 증가와 더불어 퀵서비스 레스토랑과 클라우드 키친 증가로 인해 신뢰할 수 있는 냉장 보관 솔루션의 필요성이 가속화되고 있습니다. 워크인 쿨러는 온도 관리와 정확한 재고 추적을 가능하게 함으로써 사업자가 식품의 안전성을 유지할 수 있도록 도와줍니다. 이러한 추세는 가처분 소득이 높고, 조리된 식품을 선호하는 경향이 높은 도시 지역에서 특히 두드러지며, 처음부터 조리하는 기존 방식보다 조리된 식품을 더 많이 채택하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 시장 규모

114억 달러

예측 금액

199억 달러

CAGR

5.7%

세계화된 식품 공급망은 보관 및 유통의 복잡성을 증가시켜 강력한 콜드체인 인프라의 중요성을 높이고 있습니다. 소매업체, 외식업체, 제조업체들은 장거리 운송과 변화무쌍한 기후 조건에서도 제품 품질을 유지할 수 있는 첨단 냉장 시스템에 투자하고 있습니다. 환경 문제에 대한 우려로 인해 친환경 냉매를 사용하는 에너지 절약형 쿨러에 대한 수요가 증가하고 있으며, 제조업체들은 규제 요건을 충족시키면서 기술 혁신을 통해 차별화를 꾀할 수 있는 수단을 얻게 되었습니다.

20°F-28°F(약 -6.7℃--2.2℃)의 온도대는 2025년 34.7%의 점유율을 차지할 것으로 예측됩니다. 이 온도 범위는 육류, 해산물, 유제품, 냉동식품, 통조림 식품의 보존에 적합하며, 소비 시 품질과 안전성을 유지합니다. 전문 소매점, 정육점, 식당은 식품 안전 기준을 준수하면서 제품의 유통기한을 연장하기 위해 이 온도대에 의존하고 있습니다.

간접 판매 부문은 2025년 74억 달러의 수익을 창출했습니다. 제3의 유통업체나 도매업체를 통한 판매를 통해 제조업체는 기존 네트워크를 활용하여 시장 범위를 확장하고, 직접 판매만 하는 경우보다 다양한 시장에 보다 효율적으로 접근할 수 있습니다.

미국 워크인 쿨러 시장은 2025년 31억 달러 규모로 79.6%의 점유율을 차지할 것으로 예측됩니다. 중국의 성숙한 외식 산업, 대규모 소매 네트워크, 엄격한 위생 규제가 안정적이고 에너지 절약형 냉장 설비에 대한 수요를 주도하고 있습니다. 클라우드 키친의 등장으로 미국 전역에서 고품질 워크인 쿨러 및 냉장 솔루션에 대한 필요성이 더욱 커지고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계별 부가가치

밸류체인에 영향을 미치는 요인

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

기회

성장 가능성 분석

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

가격 동향

지역별

제품 유형별

규제 상황

규격 및 컴플라이언스 요건

지역별 규제 구조

인증 기준

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추산 및 예측 : 제품 유형별, 2022-2035

주요 동향

자립형

리모트 응축식

멀티플렉스 워크인

제6장 시장 추산 및 예측 : 온도 범위별, 2022-2035

주요 동향

20F-28F

28F-32F

32F-35F

36F-40F

제7장 시장 추산 및 예측 : 소비전력별, 2022-2035

주요 동향

1 kWh 이하

2-3 kWh

4-5 kWh

5 kWh 이상

제8장 시장 추산 및 예측 : 저장 용량별, 2022-2035

주요 동향

2톤 이하

3-5톤

6-10톤

10톤 이상

제9장 시장 추산 및 예측 : 커튼 유형별, 2022-2035

주요 동향

스트립 커튼

에어 커튼

제10장 시장 추산 및 예측 : 용도별, 2022-2035

주요 동향

식품 및 음료

의료 및 의료시설

의약품

화훼

소매

기타(농업, 장의장 등)

제11장 시장 추산 및 예측 : 유통 채널별, 2022-2035

주요 동향

직접 판매

간접 판매

제12장 시장 추산 및 예측 : 지역별, 2022-2035

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

제13장 기업 개요

ABN Refrigeration Manufacturing

American Panel

Amerikooler

Arctic Walk-in Coolers &Walk-in Freezers

Bally Refrigerated Boxes

Canadian Curtis Refrigeration

Everidge

Hussmann

Imperial Brown

Kolpak

KPS Global

Master-Bilt

Nor-Lake

Thermo-Kool

U.S. Cooler

LSH

영문 목차

영문목차

The Global Walk-in Coolers Market was valued at USD 11.4 billion in 2025 and is estimated to grow at a CAGR of 5.7% to reach USD 19.9 billion by 2035.

Rising demand for perishable goods such as meat, seafood, and dairy, combined with the growing number of quick-service restaurants and cloud kitchens, is fueling the need for reliable cold storage solutions. Walk-in coolers help operators maintain food safety by controlling temperature and enabling accurate inventory tracking. This trend is particularly strong in urban areas, where higher disposable income and a preference for ready-to-eat meals are driving the adoption of pre-prepared foods over traditional cooking from scratch.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$11.4 Billion

Forecast Value

$19.9 Billion

CAGR

5.7%

Globalized food supply chains have also heightened the complexity of storage and distribution, increasing the importance of robust cold chain infrastructure. Retailers, foodservice operators, and manufacturers are investing in advanced refrigeration systems that preserve product quality during long-distance transportation and variable climate conditions. Environmental concerns are pushing demand for energy-efficient coolers that use eco-friendly refrigerants, offering manufacturers a way to differentiate themselves through technological innovation while meeting regulatory requirements.

The 20°F-28°F segment accounted for a 34.7% share in 2025. This temperature range is ideal for storing meat, seafood, dairy, frozen, and canned items, preserving their quality and safety for consumption. Specialty retailers, butcheries, and restaurants rely on this range to comply with food safety standards while extending the shelf life of their products.

The indirect sales segment generated USD 7.4 billion in 2025. Selling through third-party distributors or wholesalers allows manufacturers to leverage established networks, expand market reach, and access diverse markets more efficiently than direct sales alone.

U.S Walk-in Coolers Market held a 79.6% share, generating USD 3.1 billion in 2025. The country's mature foodservice industry, large retail network, and strict health regulations drive demand for reliable and energy-efficient refrigeration. The rise of cloud kitchens has further increased the need for quality walk-in coolers and refrigeration solutions across the U.S.

Key players in the Walk-in Coolers Market include Hussmann, KPS Global, Canadian Curtis Refrigeration, Master-Bilt, Thermo-Kool, U.S. Cooler, ABN Refrigeration Manufacturing, American Panel, Kolpak, Everidge, Imperial Brown, Bally Refrigerated Boxes, Arctic Walk-in Coolers & Walk-in Freezers, Nor-Lake, and Amerikooler. Companies in the walk-in cooler market are strengthening their presence through product innovation, focusing on energy-efficient designs and eco-friendly refrigerants that meet strict regulatory standards. Many are expanding their portfolios with modular and customizable cooler solutions to suit restaurants, retail chains, and cloud kitchens. Strategic partnerships with distributors and wholesalers help extend market reach and improve penetration in regional and urban centers. Companies are also investing in advanced temperature control and monitoring technologies, providing customers with smart, connected solutions that enhance operational efficiency and reduce food waste.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product type

2.2.3 Temperature range

2.2.4 Power consumption

2.2.5 Storage capacity

2.2.6 Curtain type

2.2.7 Application

2.2.8 Distribution channel

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Expansion of food & beverage industry

3.2.1.2 Pharmaceutical & healthcare needs

3.2.1.3 Urbanization & retail expansion

3.2.2 Industry pitfalls & challenges

3.2.2.1 High initial investment

3.2.2.2 Energy management & operational cost pressures

3.2.3 Opportunities

3.2.3.1 Smart & connected cooling solutions

3.2.3.2 Customization & modular designs

3.3 Growth potential analysis

3.4 Future market trends

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Price trends

3.6.1 By region

3.6.2 By product type

3.7 Regulatory landscape

3.7.1 Standards and compliance requirements

3.7.2 Regional regulatory frameworks

3.7.3 Certification standards

3.8 Porter's analysis

3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East and Africa

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

5.1 Key trends

5.2 Self-contained

5.3 Remote condensing

5.4 Multiplex walk-ins

Chapter 6 Market Estimates and Forecast, By Temperature Range, 2022 - 2035 (USD Billion) (Thousand Units)

6.1 Key trends

6.2 20F - 28F

6.3 28F - 32F

6.4 32F - 35F

6.5 36F - 40F

Chapter 7 Market Estimates and Forecast, By Power Consumption, 2022 - 2035 (USD Billion) (Thousand Units)

7.1 Key trends

7.2 Up to 1 KWH

7.3 2 to 3 KWH

7.4 4 to 5 KWH

7.5 Above 5 KWH

Chapter 8 Market Estimates and Forecast, By Storage Capacity, 2022 - 2035 (USD Billion) (Thousand Units)

8.1 Key trends

8.2 Up to 2 tons

8.3 3 to 5 tons

8.4 6 to 10 tons

8.5 Above 10 tons

Chapter 9 Market Estimates and Forecast, By Curtain Type, 2022 - 2035 (USD Billion) (Thousand Units)

9.1 Key trends

9.2 Strip curtain

9.3 Air curtain

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

10.1 Key trends

10.2 Food and beverage

10.3 Healthcare & medical facilities

10.4 Pharmaceuticals

10.5 Floral

10.6 Retail

10.7 Others (agriculture, mortuary, etc.)

Chapter 11 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

11.1 Key trends

11.2 Direct sales

11.3 Indirect sales

Chapter 12 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)