Ophthalmic Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892808

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 160 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

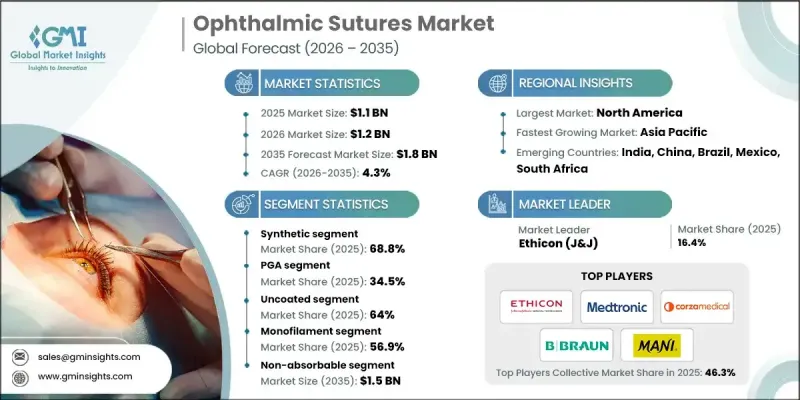

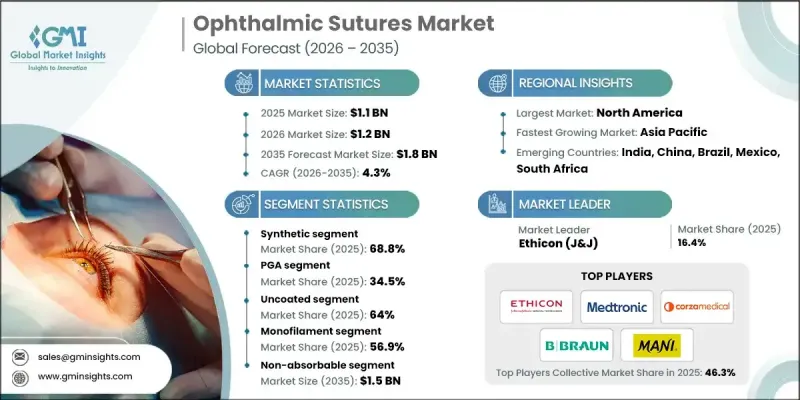

세계의 안과용 봉합사 시장은 2025년에 11억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.3%로 성장하여 18억 달러에 이를 것으로 예측됩니다.

시장 확대의 주요 요인으로는 안과 수술 건수 증가, 고령화, 기술 혁신, 안질환 유병률 증가, 양질의 의료서비스에 대한 접근성 확대 등을 꼽을 수 있습니다. 안과용 봉합사는 병원, 안과 전문 클리닉, 외래수술센터(ASC)에 중요한 수술 솔루션을 제공하여 백내장, 각막, 녹내장, 망막 수술에서 환자의 치료 성과, 정밀한 상처 관리, 수술 효율성 향상에 기여하고 있습니다. 고급 흡수성 및 비흡수성 옵션을 포함한 이 봉합사는 우수한 조작성, 최소의 조직 손상, 안정적인 수술 후 치유를 위해 설계되어 안과 의사가 섬세한 수술을 보다 정확하고 안전하게 수행할 수 있도록 도와줍니다. 미세 수술 기술의 발전과 외래 및 당일 안과 수술로의 전환 추세로 인해 염증을 줄이고 치유를 촉진하며 예측 가능한 회복 결과를 제공하는 봉합사에 대한 수요가 증가하고 있습니다. 신흥국의 의료 인프라 확충과 의료비 증가도 교정안과 수술에 대한 환자 접근성을 향상시켜 시장의 지속적인 성장을 뒷받침하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 시장 규모

11억 달러

예측 금액

18억 달러

CAGR

4.3%

합성 봉합사 부문은 높은 인장 강도, 예측 가능한 흡수성, 임상 현장에서의 광범위한 채택으로 인해 2025년 68.8%의 점유율을 차지할 것으로 예측됩니다. 폴리글락틴, 폴리글리콜산, 폴리디옥사논 등의 소재로 구성된 합성 봉합사는 조직 반응성이 낮고 감염 및 염증의 위험이 최소화되어 섬세한 안과 수술에 매우 적합합니다.

PGA 부문은 생분해성과 우수한 인장 강도로 인해 2025년 34.5%의 점유율(6억 7,000만 달러 상당)을 차지할 것으로 예측됩니다. PGA 봉합사는 체내에서 점진적으로 분해되어 봉합사 제거가 필요 없어 환자의 불편함을 줄이고, 특히 소아 및 노인 환자의 내원 횟수를 최소화할 수 있습니다.

북미 안과용 봉합사 시장은 선진화된 의료 인프라, 높은 의료비 지출, 안과 질환 증가 추세에 힘입어 2025년 38.1%의 점유율을 차지할 것으로 예측됩니다. 이 지역에는 백내장, 녹내장, 망막 수술을 많이 시행하는 병원, 외래수술센터(ASC), 전문 안과 클리닉의 광범위한 네트워크가 존재하여 안과용 봉합사에 대한 지속적인 수요를 보장합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

기술적 진보

현재 기술 동향

정밀 설계된 봉합바늘과 봉합사 편성

프리로드/즉시 사용 가능한 봉합 키트

저침습 마이크로 외과 봉합 기술

신기술

생체흡수성 봉합사 및 코팅 봉합사

첨단폴리머 및 복합재료

스마트 외과용 기구 및 로봇 지원 봉합

갭 분석

Porter's Five Forces 분석

PESTEL 분석

향후 시장 동향

디지털 수술 계획과 AI지원 마이크로 외과 수술 통합

바이오 엔지니어링 및 약제용출형 봉합사 개발

안과 의료 인프라가 발전하는 신흥 시장 확대

제4장 경쟁 구도

서론

기업 매트릭스 분석

기업의 시장 점유율 분석

세계

북미

유럽

아시아태평양

경쟁 포지셔닝 매트릭스

주요 시장 기업의 경쟁 분석

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추산 및 예측 : 유형별, 2022-2035

주요 동향

천연

합성

제6장 시장 추산 및 예측 : 재료별, 2022-2035

주요 동향

PGA

나일론

실크

폴리프로필렌

기타 소재

제7장 시장 추산 및 예측 : 코팅별, 2022-2035

주요 동향

코팅

비코팅

제8장 시장 추산 및 예측 : 소재 구조별, 2022-2035

주요 동향

모노필라멘트

멀티필라멘트/편조

제9장 시장 추산 및 예측 : 흡수성별, 2022-2035

주요 동향

흡수성

비흡수성

제10장 시장 추산 및 예측 : 용도별, 2022-2035

주요 동향

백내장 수술

각막이식 수술

녹내장 수술

유리체 절제술

눈 성형외과

기타 용도

제11장 시장 추산 및 예측 : 최종 용도별, 2022-2035

주요 동향

병원

외래수술센터(ASC)

기타 용도

제12장 시장 추산 및 예측 : 지역별, 2022-2035

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

제13장 기업 개요

Alcon

Assut Medical

Aurolab

Accutome

B Braun

Corza Medical

DemeTECH

Ethicon

FCI Ophthalmics

Geuder AG

Mani

Medtronic

Teleflex Incorporated

Unilene

LSH

영문 목차

영문목차

The Global Ophthalmic Sutures Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 1.8 billion by 2035.

Market expansion is driven by the rising number of ophthalmic surgeries, an aging population, technological innovations, and increased prevalence of eye disorders, alongside broader access to quality healthcare. Ophthalmic sutures provide crucial surgical solutions to hospitals, specialty eye clinics, and ambulatory surgical centers, enhancing patient outcomes, precise wound management, and surgical efficiency in cataract, corneal, glaucoma, and retinal procedures. These sutures, including advanced absorbable and non-absorbable options, are engineered for superior handling, minimal tissue trauma, and reliable postoperative healing, enabling ophthalmologists to perform delicate surgeries with greater precision and safety. Advancements in microsurgical techniques and the growing trend toward outpatient and ambulatory ophthalmic procedures have increased demand for sutures that reduce inflammation, accelerate healing, and provide predictable recovery outcomes. Expanding healthcare infrastructure and rising expenditure in emerging economies are also improving patient access to corrective eye surgeries, supporting consistent market growth.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.1 Billion

Forecast Value

$1.8 Billion

CAGR

4.3%

The synthetic segment held a 68.8% share in 2025, driven by high tensile strength, predictable absorption, and widespread clinical adoption. Synthetic sutures, composed of materials like polyglactin, polyglycolic acid, and polydioxanone, offer reduced tissue reactivity and minimal risk of infection or inflammation, making them highly suitable for delicate eye surgeries.

The PGA segment held a 34.5% share in 2025, valued at USD 607 million, due to its biodegradable properties and excellent tensile strength. PGA sutures degrade gradually in the body, eliminating the need for removal, reducing patient discomfort, and minimizing follow-up visits, particularly benefiting pediatric and geriatric patients.

North America Ophthalmic Sutures Market held a 38.1% share in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and growing prevalence of eye disorders. The region's extensive network of hospitals, ambulatory surgical centers, and specialty eye clinics performing a high volume of cataract, glaucoma, and retinal procedures ensures sustained demand for ophthalmic sutures.

Key players in the Global Ophthalmic Sutures Market include Teleflex Incorporated, Assut Medical, Aurolab, Ethicon, Alcon, Corza Medical, Accutome, Mani, DemeTECH, FCI Ophthalmics, Geuder AG, Medtronic, B Braun, and Unilene. Companies in the Ophthalmic Sutures Market are strengthening their position through continuous product innovation, developing sutures with improved handling, biodegradability, and tensile strength. Strategic partnerships with hospitals, clinics, and distributors enable wider reach and faster adoption of new solutions. Expanding global footprints and entering emerging markets allow manufacturers to capture rising demand in underserved regions. Investment in R&D, clinical training programs, and after-sales support enhances brand loyalty, while regulatory compliance and quality certifications build trust among healthcare providers. Marketing initiatives, educational outreach, and digital engagement strategies further solidify their market presence and competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Type trends

2.2.3 Material trends

2.2.4 Coating trends

2.2.5 Material structure trends

2.2.6 Absorption trends

2.2.7 Application trends

2.2.8 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing prevalence of eye diseases

3.2.1.2 Technological advancements

3.2.1.3 Rising prevalence of diabetes leading to ophthalmic disorders

3.2.1.4 Favorable government initiatives

3.2.1.5 Surging demand and preference for minimally invasive surgeries

3.2.2 Industry pitfalls and challenges

3.2.2.1 Postoperative complications associated with ophthalmic procedures

3.2.2.2 Lack of skilled ophthalmologist

3.2.3 Market opportunities

3.2.3.1 Rising adoption of specialty and premium sutures

3.2.3.2 Expansion in emerging markets with improving eye care infrastructure