Railway Telematics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892797

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 206 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

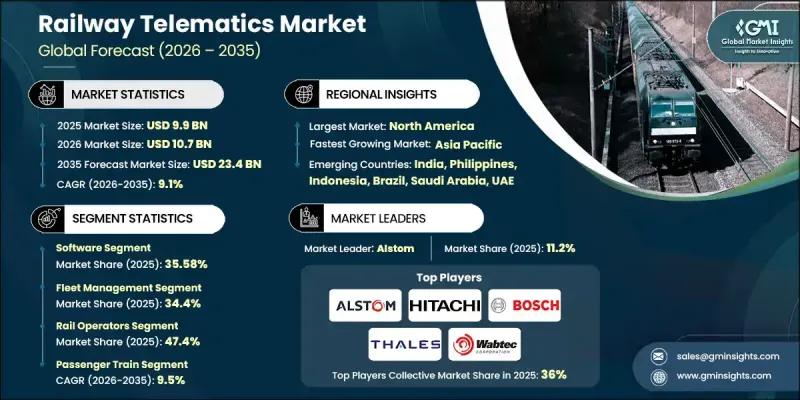

세계의 철도 텔레매틱스 시장은 2025년에 99억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.1%로 성장하여 234억 달러에 이를 것으로 예측됩니다.

세계 철도 산업의 급속한 디지털화는 사업자가 자산을 관리하고, 안전성을 높이고, 성능을 최적화하는 방식을 재구성하고 있습니다. 철도 네트워크는 GNSS 추적, IoT 기반 센서, FRMCS 또는 셀룰러 연결, AI 지원 분석을 통합하여 실시간 통찰력을 제공하는 첨단 텔레매틱스 플랫폼으로 전환하고 있습니다. 이 전환은 예지보전, 교통 조정 개선, 운행 지연 감소, 차량 수명주기 성과 향상에 도움이 될 것입니다. 스마트하고 상호 연결된 철도에 대한 수요가 증가함에 따라 업계는 멀티모달 운영, 원활한 국경 간 이동성, 고속철도의 자동화를 지원하는 소프트웨어 정의 텔레매틱스 아키텍처로의 전환을 가속화하고 있습니다. 커넥티비티 기술 제공업체, 철도 OEM 업체, 텔레매틱스 솔루션 개발업체들은 고대역폭 통신 시스템, 클라우드 분석, AI를 활용한 진단 기능을 강화하기 위해 투자를 확대하고 있습니다. 시스템 역량을 확대하기 위해 제조업체들은 다중 별자리 GNSS 모듈을 설계하고, 다중 대역 셀룰러 및 위성 링크를 채택하고, 장거리 화물 노선 및 원격 철도 회랑에서 끊김 없는 통신을 보장하는 에지 처리 장치를 도입하고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 시장 규모

99억 달러

예측 금액

234억 달러

CAGR

9.1%

소프트웨어 분야는 2024년 35.58%의 점유율을 차지하며 2035년까지 연평균 복합 성장률(CAGR) 10%를 보일 것으로 예측됩니다. 실시간 분석, 모니터링 도구, 지능형 의사 결정 엔진은 주요 철도 운영을 관리하기 위해 소프트웨어에 의존하고 있기 때문에 소프트웨어는 업계의 핵심으로 남아 있습니다. 현대의 텔레매틱스 시스템은 클라우드 기반 플랫폼, 머신러닝 진단, IoT 데이터 스트림을 활용하여 자산 가시성 향상, 장비 고장 예측, 경로 전략 수립, 전반적인 안전 강화를 실현합니다.

차량 관리 부문은 2025년 34.4%의 점유율을 차지할 것으로 예상되며, 2026년부터 2035년까지 연평균 복합 성장률(CAGR) 10.4%로 성장할 것으로 전망됩니다. 이 부문이 우위를 점하고 있는 배경에는 대규모 차량군에 대한 실시간 모니터링, 정확한 자산 운영 데이터 및 연동된 운영에 대한 요구가 증가하고 있기 때문입니다. 차량 관리 솔루션은 GPS 데이터, 적재량 및 동향 분석, 화물차 성능 진단, 센서 기반 지식을 통합하여 혼잡 완화, 스케줄 효율화, 처리 시간 단축을 실현합니다.

미국 철도 텔레매틱스 시장은 2024년 31억 2,000만 달러 규모로 85%의 점유율을 차지할 것으로 예측됩니다. 현대화 이니셔티브, 화물 운송 수요 증가, 첨단 제어 시스템 도입 확대로 인해 성장이 촉진되고 있습니다. 국내 사업자들은 광범위한 화물 네트워크의 실시간 모니터링 강화, 차량 효율성 극대화, 안전성 향상을 위해 텔레매틱스를 도입하고 있습니다. 정부 주도의 자동화, 원격 진단, 상태 기반 유지보수, 첨단 커넥티드 시스템에 대한 지원은 센서, GPS 지원 도구, 5G 통신 기술의 도입을 가속화하고 있습니다. 주요 화물 산업은 신뢰성 향상, 지연 감소, 공급망 성능 강화를 위해 텔레매틱스에 크게 의존하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률 분석

비용 구조

각 단계별 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재 기술 동향

신기술

특허 분석

비용 내역 분석

사업 계획과 투자수익률(ROI) 분석

총 소유비용(TCO) 프레임워크

투자수익률(ROI) 산출 방법

시행 스케줄과 주요 마일스톤

리스크 평가와 경감 전략

지속가능성과 환경 영향 분석

지속가능한 실천

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국에 관한 고려사항

전망과 기회

기술 로드맵과 진화 타임라인

새로운 응용 기회

투자 요건과 자금원

리스크 평가 및 경감 전략

시장 진출기업에의 전략적 제안

투자 및 자금조달 분석

정부의 인프라 투자

프라이빗 에퀴티 및 벤처캐피털 활동

M&A 거래 및 평가(2022-2025)

레일 펄스 연합 및 업계 컨소시엄

데이터 보안, 프라이버시 및 사이버 보안 프레임워크

사이버 보안 위협 상황

규제 및 컴플라이언스 프레임워크

데이터 프라이버시 규제

사이버 보안 아키텍처와 베스트 프랙티스

위협 감지 및 사고 대응

벤더 및 공급망 보안

신흥 사이버 보안 기술

제품 수명주기와 기술 진부화

철도 산업 기술 도입 사이클

하드웨어 수명주기 관리

소프트웨어 수명주기 관리

통신기술 진부화

인증 및 안전 인가 수명주기

진부화 관리 전략

신기술 채택 스케줄

신흥 비즈니스 모델과 서비스 혁신

기존 비즈니스 모델

구독 및 SaaS 모델

설비 서비스(EAAS) 및 관리 서비스

성과 연동형 계약 및 퍼포먼스 계약

종량제 및 종량 빌링 모델

에코시스템 및 플랫폼 비즈니스 모델

민관 제휴(PPP) 모델

혁신적인 서비스 제공 모델

철도 인프라 및 회랑 분석

세계 철도 네트워크 개요

전용 화물 회랑

여객 및 화물 공용 노선

고속 철도 회랑

도시 교통 네트워크 및 지하철 시스템

국경을 넘은 국제 회랑

인프라 용량과 이용률

인프라 현황과 현대화 필요성

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획과 자금조달

제5장 시장 추산 및 예측 : 컴포넌트별, 2022-2035

주요 동향

하드웨어

GPS 디바이스

센서

통신 모듈

차량내 장치(OBU)

텔레매틱스 제어 장치(TCU)

소프트웨어

플릿 관리

예지보전

데이터 분석과 보고서 작성

기타

서비스

설치 및 통합

유지보수 및 지원

제6장 시장 추산 및 예측 : 솔루션별, 2022-2035

주요 동향

플릿 관리

열차 추적 및 모니터링

승객 정보 시스템

안전 및 보안 시스템

예지보전

제7장 시장 추산 및 예측 : 열차별, 2022-2035

주요 동향

여객 열차

화물 열차

제8장 시장 추산 및 예측 : 최종 용도별, 2022-2035

주요 동향

철도 사업자

철도 물류 사업자

정부기관

제9장 시장 추산 및 예측 : 통신 분야별, 2022-2035

주요 동향

GPS/GNSS 기반 위치 측위 시스템

셀룰러 통신기술

위성통신

Wi-Fi 및 단거리 통신

CBTC 무선 시스템

IoT 및 센서 네트워크

제10장 시장 추산 및 예측 : 지역별, 2022-2035

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

아시아태평양

중국

인도

일본

호주

한국

필리핀

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

제11장 기업 개요

세계 기업

Alstom

Bosch

Hitachi Rail

Huawei Technologies

IBM

Knorr-Bremse

Siemens

Stadler Rail

Thales

Wabtec

지역 기업

Cisco Systems

Mitsubishi Electric

Nippon Signal

Progress Rail Services(Caterpillar)

Televic Rail

Trimble

신규 기업

DOT

EKE-Electronics

Intermodal Telematics BV(IMT)

Nexxiot

ORBCOMM

Rail Vision

Railnova

SAVVY Telematic Systems

Wi-Tronix

LSH

영문 목차

영문목차

The Global Railway Telematics Market was valued at USD 9.9 billion in 2025 and is estimated to grow at a CAGR of 9.1% to reach USD 23.4 billion by 2035.

Rapid digitalization across the global rail industry is reshaping how operators manage assets, enhance safety, and optimize performance. Rail networks are shifting toward advanced telematics platforms that merge GNSS tracking, IoT-driven sensors, FRMCS or cellular connectivity, and AI-enabled analytics to deliver real-time insights. This transition supports predictive maintenance, improved traffic coordination, reduced operational delays, and better lifecycle outcomes for rolling stock. As the demand for smart, interconnected railways accelerates, the industry is moving closer to software-defined telematics architectures that support multimodal operations, seamless cross-border mobility, and high-speed rail automation. Connectivity technology providers, rail OEMs, and telematics solution developers are enlarging their investments to strengthen high-bandwidth communication systems, cloud analytics, and AI-powered diagnostics. To expand system capabilities, manufacturers are designing multi-constellation GNSS modules, adopting multi-band cellular and satellite links, and deploying edge processing devices that ensure uninterrupted communication along long-distance freight routes and remote rail corridors.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$9.9 Billion

Forecast Value

$23.4 Billion

CAGR

9.1%

The software segment held a 35.58% share in 2024 and is anticipated to grow at a CAGR of 10% through 2035. Software remains central to the industry because real-time analytics, monitoring tools, and intelligent decision engines rely on it to manage key rail operations. Modern telematics systems depend on cloud-based platforms, machine learning diagnostics, and IoT data streams to boost asset visibility, forecast equipment failures, strategize routing, and enhance overall safety.

The fleet management segment held a 34.4% share in 2025 and is forecasted to grow at a CAGR of 10.4% from 2026 to 2035. This segment dominates due to the increased need for real-time supervision, accurate asset utilization data, and synchronized operations across large fleets. Fleet management solutions integrate GPS data, load and movement analytics, wagon performance diagnostics, and sensor-based insights to reduce congestion, streamline scheduling, and shorten turnaround durations.

U.S. Railway Telematics Market held an 85% share, generating USD 3.12 billion in 2024. Growth is fueled by modernization initiatives, rising freight transport demands, and increased adoption of advanced control systems. Operators in the country are implementing telematics to strengthen real-time oversight, maximize fleet efficiency, and improve safety across extensive freight networks. Government-driven support for automation, remote diagnostics, condition-based maintenance, and advanced connectivity systems is accelerating the deployment of sensors, GPS-enabled tools, and 5G communication technologies. Key freight industries rely heavily on telematics to boost reliability, reduce delays, and ensure stronger supply-chain performance.

Key companies operating in the Global Railway Telematics Market include Cisco Systems, Nexxiot, Wabtec, Siemens, Bosch, Alstom, Hitachi, Thales, Trimble, and Knorr-Bremse. Companies competing in the Railway Telematics Market strengthen their market position by expanding software capabilities, developing AI-driven analytics, and enhancing high-speed connectivity infrastructures. Many organizations invest in interoperable platforms that support seamless data exchange across rail networks, enabling unified fleet visibility and predictive diagnostics. Strategic collaborations with connectivity providers help integrate satellite, cellular, and GNSS technologies into telematics systems for uninterrupted coverage. Firms also prioritize modular designs, edge computing capabilities, and cloud-based telematics to deliver scalable, flexible solutions for operators.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2022 - 2035

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Solution

2.2.4 Train

2.2.5 End Use

2.2.6 Communication

2.3 TAM Analysis, 2026-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising digitalization and automation in rail operations

3.2.1.2 Government investments in smart rail infrastructure

3.2.1.3 Demand for enhanced fleet visibility and safety compliance

3.2.1.4 Growth in freight rail and cross-border logistics

3.2.2 Industry pitfalls and challenges

3.2.2.1 High capital costs and integration complexity

3.2.2.2 Network coverage limitations in remote rail corridors

3.2.3 Market opportunities

3.2.3.1 Expansion of predictive maintenance solutions

3.2.3.2 Integration with digital twins & rail automation

3.2.3.3 Growth in freight wagon & container telematics