Marine Sealants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892788

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

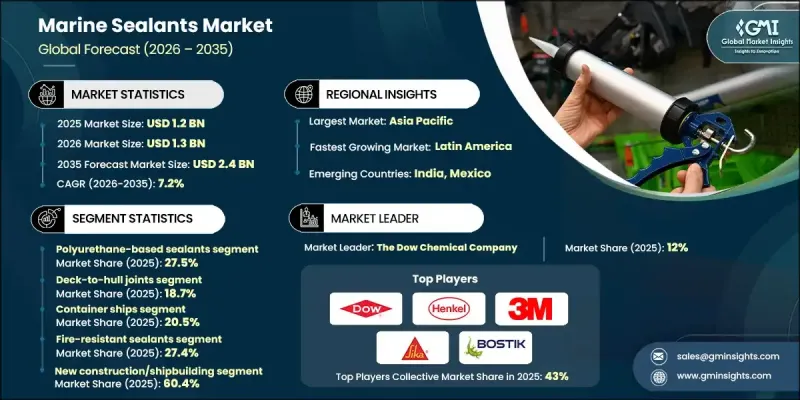

세계의 선박용 실란트 시장은 2025년에 12억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.2%로 성장하여 24억 달러에 이를 것으로 예측됩니다.

선박용 실란트는 틈새 제품에서 현대 해양 활동의 중요한 구성 요소로 진화해 왔습니다. 그 중요성은 기본적인 씰링 기능을 넘어 선박의 무결성 확보, 부식 방지, 장기적인 구조적 성능 향상에 이르기까지 그 중요성이 확대되고 있습니다. 지속가능성은 업계의 주요 원동력이 되고 있으며, 친환경 및 저배출 실란트는 선박 건조, 유지보수 및 개보수 과정에서 점점 더 중요시되고 있습니다. 하이브리드 폴리머 배합, 저휘발성 유기화합물(VOC) 시스템 등의 기술 혁신도 시장을 더욱 촉진하고 있습니다. 이들은 엄격한 환경 기준을 충족시키면서 가혹한 해양 환경에서도 뛰어난 성능을 발휘합니다. 지역별 우선순위와 현지 해양산업 기반은 세계 규제 요건과 탈탄소화 목표에 부합하는 혁신이 전개되는 가운데 이 시장의 성장 패턴에 큰 영향을 미치고 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 시장 규모

12억 달러

예측 금액

24억 달러

CAGR

7.2%

폴리우레탄계 실란트 부문은 2025년 27.5%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 6.8%의 성장률을 보일 것으로 전망됩니다. 높은 유연성과 동적 하중 하에서 우수한 접착력으로 선체 접합부 및 갑판 구조에 필수적입니다. 자외선과 염수에 대한 내성으로 잘 알려진 실리콘계 실란트는 열악한 해양 환경에서 외부용으로 선호되는 실란트입니다. 열악한 운영 환경에서 우수한 내화학성 및 내연료성으로 인해 폴리설파이드계 실란트 수요는 지속적으로 높은 수준을 유지하고 있습니다.

갑판과 선체 접합부 부문은 2025년 18.7%의 점유율을 차지할 것으로 예상되며, 2035년까지 연평균 6.9%의 성장률을 보일 것으로 예측됩니다. 이 용도의 실란트는 지속적인 운동으로 인한 동적 스트레스를 견뎌내야 합니다. 한편, 수상선상의 용도는 자외선 및 내후성이 요구되며, 수중선 아래의 씰링은 장기적인 성능 유지를 위해 고도의 접착력과 방수성이 요구됩니다.

북미 선박용 실란트 시장은 조선 활동, 레저용 보트의 성장, 해양 인프라 투자에 힘입어 2025년 15.4%의 점유율을 차지할 것으로 예측됩니다. 이 지역은 첨단 제조 기술, 강력한 안전 규제, 지속가능성에 대한 관심 등의 이점을 활용하여 고성능 선박용 실란트 기술에 대한 기회를 창출하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계별 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

화학 유형별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴 및 협업

신제품 발매

사업 확대 계획

제5장 시장 추산 및 예측 : 화학 유형별, 2022-2035

주요 동향

폴리우레탄계 실란트

실리콘계 실란트 (폴리실록산)

폴리설파이드 기반 실란트

하이브리드/변형 실란 폴리머 (ms 폴리머/stp)

에폭시 기반 실란트

부틸 기반 실란트

아크릴 기반 실란트

나노 하이브리드 스마트 실란트

바이오 기반/지속 가능한 제형

제6장 시장 추산 및 예측 : 용도별, 2022-2035

주요 동향

갑판과 선체 접합부

수선상 실링

수선하 실링

창문 및 현창 접착/직접 유리벽

구조용 접착 및 조립

해상 풍력발전 기초 실링

Monopile grout seals

Pre-piled jacket sealing

Post-piled jacket sealing

Skirt seals (non-grouted monopiles)

Flange seals (VW, VT types)

Airtight platform seals (CS-111/114, CS-80/70)

Nacelle & turbine component sealing

방화 및 내화 씰

밸러스트 탱크 코팅 및 밀봉

방음 씰

방오 용도

살생물제계 방오제

살생물제 무첨가 방오

제7장 시장 추산 및 예측 : 선박·구조물 유형별, 2022-2035

주요 동향

컨테이너선

벌크 캐리어

Capesize (≥100,000 dwt)

Panamax (65,000-99,999 dwt)

Handymax (40,000-64,999 dwt)

Handysize (10,000-39,999 dwt)

석유 및 화학제품 탱커

ULCC & VLCC (Ultra/Very Large Crude Carriers)

Suezmax Tankers

Aframax/LR2 Tankers

Panamax/LR1 Tankers

MR & Handy Tankers

Chemical Tankers (Specialized Sealing Requirements)

해상 풍력발전기 및 구조물

여객선

액화 가스 운반선

해군 및 방위 함정

해상 석유 및 가스 구조물

일반 화물선 및 다목적선

소형 선박 및 레크리에이션 선박

어선

제8장 시장 추산 및 예측 : 성능 특성별, 2022-2035

주요 동향

내화성 실란트

방식 실란트

자외선 내성 실란트

방오 실란트

고가동성 실란트

자기치유 실란트

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035

주요 동향

신규 건조 배 및 조선

수리 및 유지보수

개보수 및 현대화

해양 설비 설치 및 건설

제10장 시장 추산 및 예측 : 지역별, 2022-2035

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트(UAE)

기타 중동 및 아프리카

제11장 기업 개요

Sika AG

3M Company

Henkel AG &Co. KGaA

The Dow Chemical Company

PPG Industries, Inc.

The Sherwin-Williams Company

Trelleborg AB

Berger Maritiem

Chugoku Marine Paints, Ltd.

Jotun A/S

Hempel A/S

Feynlab

Sea-Shield

ITW Performance Polymers

Bostik(Arkema Group)

Wacker Chemie AG

Momentive Performance Materials

Evonik Industries AG

LSH

영문 목차

영문목차

The Global Marine Sealants Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 2.4 billion by 2035.

Marine sealants have evolved from being a niche product to becoming a crucial component in modern maritime operations. Their importance now extends beyond basic sealing to enhancing vessel integrity, corrosion protection, and long-term structural performance. Sustainability has become a major driver in the industry, as eco-friendly and low-emission sealants are increasingly favored in shipbuilding, maintenance, and retrofitting processes. The market is further fueled by technological advancements, including hybrid polymer formulations and low volatile organic compound (VOC) systems, which meet stringent environmental standards while delivering superior performance in harsh marine environments. Regional priorities and the strength of local maritime industries strongly influence growth patterns in this market, as innovation aligns with regulatory requirements and decarbonization goals worldwide.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$1.2 Billion

Forecast Value

$2.4 Billion

CAGR

7.2%

The polyurethane-based sealants segment held a 27.5% share in 2025 and is expected to grow at a CAGR of 6.8% through 2035. Their high flexibility and excellent adhesion under dynamic loads make them essential for hull joints and deck structures. Silicone-based sealants, known for UV and saltwater resistance, are preferred for exterior applications in challenging marine conditions. Polysulfide sealants remain in demand for their exceptional chemical and fuel resistance under harsh operational conditions.

The deck-to-hull joints segment held 18.7% share in 2025 and is expected to grow at a CAGR of 6.9% by 2035. Sealants in this application must withstand dynamic stresses from constant motion, while above-waterline applications demand UV and weather resistance, and below-waterline sealing requires advanced adhesion and water impermeability for long-term performance.

North America Marine Sealants Market accounted for a 15.4% share in 2025, driven by shipbuilding activities, recreational boating growth, and investments in offshore infrastructure. The region benefits from advanced manufacturing, robust safety regulations, and a focus on sustainability, creating opportunities for high-performance marine sealant technologies.

Key players operating in the Global Marine Sealants Market include Sika AG, 3M Company, Henkel AG & Co. KGaA, The Dow Chemical Company, PPG Industries, Inc., The Sherwin-Williams Company, Trelleborg AB, Berger Maritiem, Chugoku Marine Paints, Ltd., Jotun A/S, Hempel A/S, Feynlab, Sea-Shield, ITW Performance Polymers, Bostik (Arkema Group), Wacker Chemie AG, Momentive Performance Materials, and Evonik Industries AG. Companies in the Global Marine Sealants Market are employing several strategies to strengthen their market position. They are investing in research and development to create eco-friendly formulations with improved adhesion, UV resistance, and chemical durability. Strategic partnerships with shipbuilders, maintenance providers, and offshore operators expand market reach and ensure adoption of high-performance products. Firms are also focusing on regional expansion, particularly in emerging maritime markets, and optimizing distribution channels for faster product delivery.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Chemistry Type

2.2.3 Application

2.2.4 Vessel/Structure Type

2.2.5 Performance Characteristics

2.2.6 End use

2.3 TAM Analysis, 2025-2035

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rapid offshore wind energy expansion

3.2.1.2 Stringent IMO fire safety regulations

3.2.1.3 Global fleet expansion & modernization

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of advanced smart sealants

3.2.2.2 Skilled application requirements

3.2.3 Market opportunities

3.2.3.1 Self-healing & smart sealant technologies

3.2.3.2 Offshore wind foundation sealing specialization

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By Chemistry type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Chemistry Type, 2022-2035 (USD Million) (Kilo Tons)