자율주행 서비스 공유 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)

Autonomous Ride-Sharing Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1892714

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

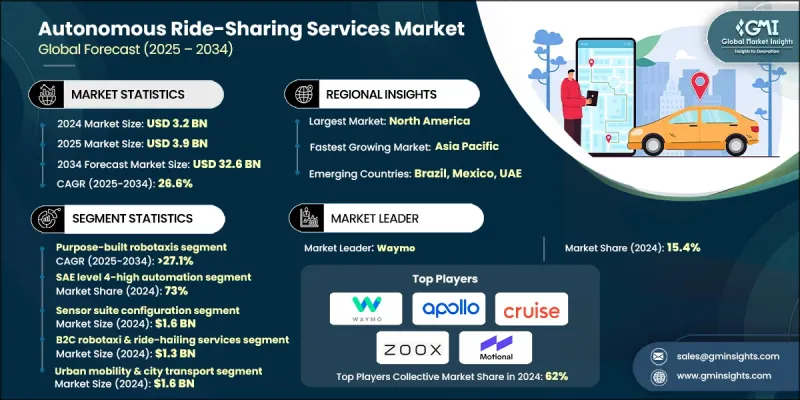

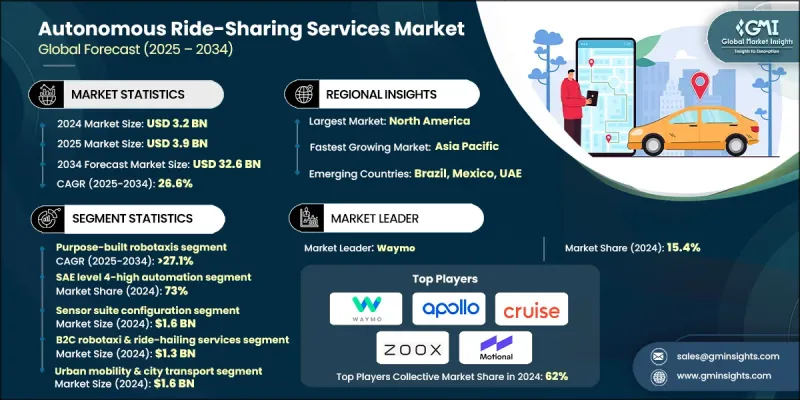

세계의 자율주행 서비스 공유 시장은 2024년 32억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 26.6%를 나타내 326억 달러에 이를 것으로 예측됩니다.

이러한 성장은 자율주행 시스템의 급속한 혁신, 경제적인 도시 교통 수단에 대한 수요 증가 및 지능형 교통 네트워크에 대한 투자 확대로 추진되고 있습니다. 도시가 교통 압력을 줄이고 배출 가스를 줄이고 이동 효율을 높이기 위해 노력하면서 자율 주행 라이드 쉐어 플랫폼은 향후 교통 수단의 확장 가능한 기반이되고 있습니다. AI 기반의 지각 기술, 고급 자동화 기능, 연결된 센서, 고속 네트워크, 실시간 차량 그룹 인텔리전스의 융합이 자동 운전 차량 그룹의 기능을 재구성하고 있습니다. 이러한 기술은 정확한 조종, 예측 라우팅, 충돌 회피 판단 프로세스 및 차량 성능의 지속적인 모니터링을 지원합니다. 적응 학습 모델, 경로 시뮬레이션 환경, 클라우드 연계형 플릿 툴을 통해 사업자는 안전성 향상, 운영 장애 감소, 보다 빠르고 안정적인 온디맨드 이동 서비스 제공을 실현하고 있습니다. 자율주행 라이드 서비스 플랫폼의 확대, 통합형 플릿 관리 시스템, 통합형 MaaS(Mobility as a Service) 프레임워크, 자동배차 기술의 진전에 따라 도입도 가속화되고 있습니다. 이러한 솔루션은 사용자의 온보딩을 간소화하고, 응답성 있는 가격 설정을 지원하고, 도로 인프라와의 연계를 강화하며, 여러 이동 수단 간의 원활한 조정을 가능하게 합니다. 모빌리티 제공업체, 기술 개발자, 교통기관 간의 협력을 통해 공유 및 개인형 이동 환경에서의 자율주행 모빌리티는 더욱 진화하고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 가치

32억 달러

예측 금액

326억 달러

CAGR

26.6%

전용 설계의 로봇 택시 카테고리는 2024년에 48%의 점유율을 차지했고 2034년까지 27.1%의 성장이 전망되고 있습니다. 이 부문이 주도적인 지위에 있는 이유는 자율주행 전용으로 설계된 차량으로, 고중복 감지 기술, 공유 이용에 최적화된 인테리어, 효율적인 전기 기반을 갖추고 있기 때문입니다. 운영 비용 절감, 높은 가동률, 확장성이 높은 전개를 실현하는 능력이 주요 도시권에서의 우위성을 강화하고 있습니다.

SAE 레벨 4(고도자동운전) 부문은 2024년에 73%의 점유율을 차지했으며, 2025년부터 2034년까지 26.2%를 나타낼 전망입니다. 이 범주가 주도적인 지위에 있는 이유는 사전정의된 운용구역 내에서 완전자동운전 서비스를 실현하여 구조화된 환경하에서 신뢰성이 높은 상용 차량군을 가능하게 하기 때문입니다. 사업자는 안정적인 성능, 인적 감시에 대한 의존도 감소, 기존의 이동성 인프라와의 호환성 등, 레벨 4 시스템을 선택하는 경향이 강해지고 있습니다.

미국의 자율주행 서비스 공유 시장은 2024년에 88%의 점유율을 차지하여 11억 달러의 수익을 창출했습니다. 이 지역의 견고한 지위는 우수한 디지털 능력, 고도로 발전한 이동성 생태계, 자율 기술의 조기 도입을 반영합니다. 지원 규제 프레임워크, 광범위한 시험 프로그램, 대규모 플릿 배포에 많은 투자가 북미를 세계 리더로 자리매김하고 있으며, 보다 안전하고 깨끗하고 효율적인 이동성 선택에 대한 사용자 관심 증가가 이를 뒷받침하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 현황

이익률

비용 구조

각 단계별 부가가치

밸류체인에 영향을 주는 요인

파괴적 혁신

업계에 미치는 영향요인

성장 촉진요인

자율주행 기술의 급속한 진전

비용 효율적인 도시 이동성에 대한 수요 증가

정부에 의한 스마트 교통 및 저배출 모빌리티 추진

기술 대기업 및 이동성 사업자에 의한 투자 증가

업계의 잠재적 위험 및 과제

자율주행차대 도입의 고비용

규제 및 안전면에서의 불확실성

시장 기회

스마트 시티 및 mobility-as-a-service(MaaS) 전개

전기자동운전 차량군의 도입

기업·캠퍼스·폐쇄 환경에 있어서 모빌리티

기술적 진보와 AI 통합

성장 가능성 분석

규제 상황

연방규제(NHTSA, FMCSA, FTA 지침)

주 수준의 허가 및 시험 요건

지방 조례(연석 관리, 지오펜싱, 영업 시간)

ADA 준거 및 접근성 요건

안전기준과 자발적인 자기평가

책임과 보험의 틀

데이터 프라이버시 및 사이버 보안 규제

국제적인 규제의 조화

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 전망

센서 기술의 진화(LiDAR, 레이더, 카메라, 융합 기술)

지각·위치 특정 알고리즘

운동 계획·제어 시스템

고정밀 매핑 및 맵리스 내비게이션 기법

V2X 통신과 협조자동운전

원격 조작 및 원격 조작 시스템

사이버 보안 및 데이터 프라이버시 기술

액세서블 차량 설계 및 자동화 고정 시스템

가격 동향

지역별

제품별

코스트 내역 분석

특허 분석

지속가능성과 환경적 측면

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

최상의 시나리오

특허 및 지적재산 분석

기술 분야별 특허 출원 동향

주요 특허 보유 기업(Waymo, Cruise, Zoox, Motional, Aurora)

센서 퓨전 및 지각 기술의 특허 동향

운동계획·제어에 관한 특허 클러스터

고정밀 매핑 및 위치 지정 기술(IP)

특허소송과 라이선싱 동향

투자·자금 조달 분석

벤처캐피탈 및 프라이빗 주식 투자 동향

기업 전략적 투자

연방 조성 프로그램

공공시장에서의 활동

개발단계별 자금조달

투자의 지리적 분포

운영 설계 영역(ODD) 분석

지리적 ODD 제약(지오펜싱, 도시 커버율)

도로 유형별 운용 조건(ODD)(도시 간선 도로, 고속도로, 주택 도로)

속도 범위 ODD

기상 및 환경 ODD

ODD 확장 전략과 타임라인

액세서빌러티 및 유니버설 디자인 실시 기준

자율주행 라이드 쉐어링에 있어서 ADA 준거 요건

액세서블 차량 설계 요건

액세서블 휴먼 머신 인터페이스

경로 안내·내비게이션 지원

연방 정부에 의한 접근성 조사 및 자금 제공

자율주행 차량용 유니버설 디자인 원칙

컴플라이언스 모니터링 및 집행

원격조작·원격조작 인프라 분석

원격 조작 아키텍처 및 이용 사례

원격조작과 원격지원의 구별

원격조작의 안전성에 관한 NHTSA의 조사

네트워크 인프라 요건

원격조작센터 설계

원격 조작에 관한 규제 요건

경제적 고려 사항

인프라 의존성 및 생태계 준비도 평가

도로 인프라 요건

차량과 인프라 간의 통신(V2I)

전기자동운전 차량군용 충전 인프라

고정밀 매핑 인프라 및 유지 보수

연석 공간 관리 및 승강 존

통신 인프라

에코시스템 준비도 평가 프레임워크

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수합병

파트너십 및 협력

신제품 출시

사업 확대 계획과 자금 조달

제5장 시장 추계·예측 : 자동화 레벨별(2021-2034년)

주요 동향

SAE 레벨 4 - 고도 자동화

SAE 레벨 5 - 완전 자동화

제6장 시장 추계·예측 : 기술 플랫폼별(2021-2034년)

주요 동향

센서 스위트 구성

LiDAR 주요 시스템

레이더 진화 시스템

멀티모달 센서 융합

컴퓨팅 아키텍처

연결 유형

매핑 및 위치 파악 접근법

제7장 시장 추계·예측 : 서비스 모델별(2021-2034년)

주요 동향

B2C 로보택시 및 주행 공유

B2B 기업 및 캠퍼스 셔틀 서비스

B2G 지방자치단체 및 대중교통 연계 서비스

공항 및 전용 구간 셔틀

제8장 시장 추계·예측 : 차량별(2021-2034년)

주요 동향

전용 로봇택시

승용차 및 세단

밴 및 다목적 차량

저속 자동화 셔틀

대형 대중교통 버스(40피트 이상)

제9장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

도시 모빌리티 및 도시 교통

퍼스트/라스트 마일 대중교통 연결성

캠퍼스 및 폐쇄 환경 교통

농촌 및 서비스 취약 지역 이동성

보조 교통 및 접근성 서비스

제10장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

싱가포르

한국

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

아랍에미리트(UAE)

남아프리카

사우디아라비아

제11장 기업 프로파일

세계 기업

Cruise LLC

Geely/Zeekr

General Motors

Hyundai Motor Group

Jaguar Land Rover

Motional

Toyota Motor Corporation

Volkswagen Group

Waymo LLC

Zoox Inc.

지역 기업

Alphabet Inc.

Amazon

Aptiv PLC

Continental AG

EasyMile

Intel/Mobileye

May Mobility

New Flyer

NVIDIA Corporation

Qualcomm

신흥 기업

Aurora Innovation

Beep Inc.

Innoviz Technologies

Luminar Technologies

Perrone Robotics

KTH

영문 목차

영문목차

The Global Autonomous Ride-Sharing Services Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 26.6% to reach USD 32.6 billion by 2034.

Growth is fueled by fast-moving innovation in autonomous driving systems, increasing demand for affordable urban travel options, and expanding investment in intelligent transportation networks. As cities work toward reducing traffic pressure, cutting emissions, and improving mobility efficiency, autonomous ride-sharing platforms are becoming a scalable pillar of future transportation. The fusion of AI-based perception, advanced automation features, connected sensors, high-speed networks, and real-time fleet intelligence is reshaping how self-driving fleets function. These technologies support accurate maneuvering, predictive routing, collision-avoidance decision processes, and continuous monitoring of vehicle performance. Through adaptive learning models, route simulation environments, and cloud-coordinated fleet tools, operators improve safety outcomes, reduce operational disruptions, and deliver quicker and more dependable mobility on demand. Adoption is also gaining momentum with the expansion of autonomous ride-service platforms, orchestrated fleet management systems, integrated mobility-as-a-service frameworks, and automated dispatch technologies. These solutions streamline user onboarding, support responsive pricing, enhance communication with roadway infrastructure, and enable smoother coordination across multiple modes of travel. Collaboration among mobility providers, technology developers, and transportation agencies is further advancing autonomous mobility in both shared and private travel settings.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.2 Billion

Forecast Value

$32.6 Billion

CAGR

26.6%

The purpose-built robotaxis category held a 48% share in 2024 and is projected to grow at a 27.1% through 2034. This segment leads due to vehicles designed specifically for autonomous operation, engineered with high-redundancy sensing, optimized interiors for shared use, and efficient electric foundations. Their ability to achieve lower operating costs, higher utilization, and scalable deployment has reinforced their dominance across major metropolitan areas.

The SAE Level 4-High Automation segment accounted for a 73% share in 2024 and is set to grow at 26.2% from 2025 to 2034. This category leads because it supports fully autonomous service within predefined operating zones, enabling dependable commercial fleets across structured environments. Operators increasingly choose Level 4 systems due to their consistent performance, reduced reliance on human monitors, and compatibility with existing mobility infrastructure.

US Autonomous Ride-Sharing Services Market held an 88% share, generating USD 1.1 billion in 2024. The region's strong position reflects robust digital capabilities, a highly developed mobility ecosystem, and early adoption of autonomous technologies. Supportive regulatory pathways, extensive testing programs, and significant investment in large-scale fleet rollout have positioned North America as a global leader, strengthened by rising user interest in safer, cleaner, and more efficient mobility options.

Major companies active in the Autonomous Ride-Sharing Services Market include Hyundai Motor Group, Zoox, Cruise, Waymo, Baidu Apollo, Motional, General Motors, AutoX, Pony.ai, and Jaguar Land Rover. Companies in the Autonomous Ride-Sharing Services Market are enhancing their market foothold by accelerating development of autonomous driving stacks, investing in scalable electric fleet platforms, and expanding AI-based operational intelligence. Many firms focus on forming alliances with automakers, software developers, and mobility partners to secure technology integration and broaden deployment opportunities. Continuous testing across controlled environments helps improve system reliability and regulatory acceptance.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Automation level

2.2.3 Technology platform

2.2.4 Service model

2.2.5 Vehicle

2.2.6 Application

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rapid advancements in autonomous driving technologies

3.2.1.2 Rising demand for cost-efficient urban mobility

3.2.1.3 Government push for smart transportation & low-emission mobility

3.2.1.4 Increasing investments from tech giants & mobility operators

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of autonomous fleet deployment

3.2.2.2 Regulatory & safety uncertainty

3.2.3 Market opportunities

3.2.3.1 Expansion into smart cities & mobility-as-a-service (maas)

3.2.3.2 Adoption of electric autonomous fleets

3.2.3.3 Corporate, campus, and closed-environment mobility

3.2.3.4 Technological advancements and AI integration

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 Federal regulations (NHTSA, FMCSA, FTA guidance)