질화갈륨(GaN) 전기자동차 충전기 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Gallium Nitride (GaN) EV Charger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1885895

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

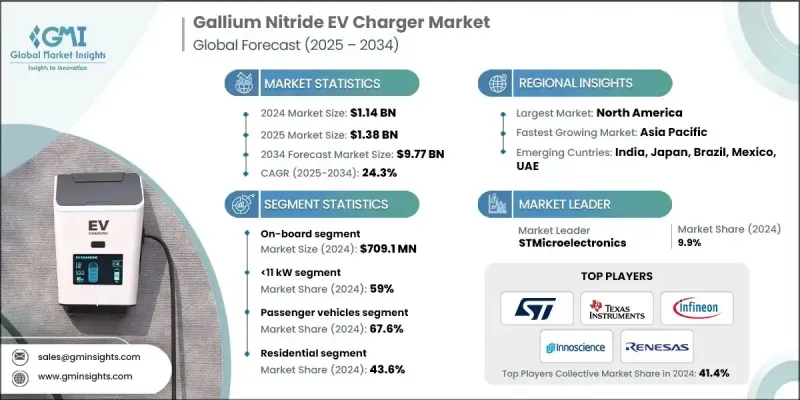

세계의 질화갈륨(GaN) 전기자동차 충전기 시장은 2024년에 11억 4,000만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 24.3%를 나타낼 것으로 예측되며 97억 7,000만 달러로 성장할 전망입니다.

시장은 독립형 개별 장치에서 GaN 스위치와 드라이버 및 보호 기능을 결합한 통합 하프 브리지 스테이지 및 모듈로 전환되고 있습니다. 이러한 통합은 레이아웃 민감도와 전자기 간섭(EMI)을 줄이면서 열 성능을 향상시킵니다. 공공-민간 협력 사업은 광대역갭(WBG) 기술의 상용화를 가속화하여 온보드 충전기(OBC) 및 전기차 전력 시스템용 통합 GaN 솔루션의 채택을 촉진하고 있습니다. 자동차 제조사들은 점점 더 높은 수준의 장치 통합을 지원하는 다기능 전력 도메인을 통합하고 있습니다. OBC 컨버터 시연 결과, GaN은 실리콘 기반 시스템 대비 전력 밀도를 170% 증가시키고 무게를 79% 감소시킬 수 있으며, 6.6kW 듀얼 액티브 브리지 프로토타입에서 99%의 최고 효율을 달성했습니다. GaN 소자는 실리콘보다 높은 주파수에서 낮은 전도 손실로 스위칭이 가능해, 고급 EV 컨버터에서 손실을 60-80% 줄이면서 더 작은 자기 부품 및 냉각 시스템을 사용할 수 있게 합니다. 설계 팀은 또한 컨버터 성능과 모터 기생 손실 간의 균형을 맞추기 위해 스위칭 주파수를 최적화하고 있습니다. 연구에 따르면 고-HfO2 게이트 유전체로 제작된 1.2kV GaN MOSFET은 매우 낮은 게이트 누설과 더 높은 전류 밀도를 달성합니다. 이는 기판 및 공정 기술이 성숙되면 수직 GaN 소자가 1.2kV 용도에서 SiC와 경쟁할 수 있는 위치에 있음을 의미합니다. 그러나 800V+ 및 150kW 트랙션 용도에 대한 자동차 인증은 비용 및 신뢰성 고려 사항으로 인해 2020년대 말까지 준비될 것으로 예상되며, 현재 개발 중입니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 가치

11억 4,000만 달러

예측 가치

97억 7,000만 달러

CAGR

24.3%

수평형 GaN 디바이스 부문은 70%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 16.1%의 성장률을 보일 것으로 예측됩니다. 수평형 GaN 장치는 650V까지의 OBC, DC-DC 컨버터 및 보조 시스템을 위한 EV 전력 전자 장치를 지배합니다. 실리콘 상의 AlGaN/GaN HEMT 구조는 높은 전자 이동도와 임계 전계 강도를 제공하여 실리콘 대비 높은 차단 전압에서 낮은 온 저항을 구현합니다.

중전압 부문(100-650V)은 2024년 67%의 점유율을 기록했으며, 2034년까지 연평균 16%의 성장률을 보일 것으로 예상됩니다. 중전압 GaN 소자는 대부분의 OBC(현재 400V, 향후 800V로 상승) 및 다수 DC-DC 컨버터가 이 범위에 속하기 때문에 광범위하게 적용됩니다. GaN의 고주파 성능은 6.6-19.2kW OBC 시스템의 역률 보정 및 LLC/공진 컨버터 단계에서 효율과 전력 밀도를 직접 향상시킵니다.

중국의 질화갈륨(GaN) 전기차 충전기 시장은 2024년 7,340만 달러 규모를 기록했습니다. 전 세계 전기차 판매량의 약 3분의 2를 차지하는 중국의 규모는 모든 전기차가 온보드 충전기, DC-DC 컨버터 및 호환 충전 인프라를 필요로 하기 때문에 GaN 장치에 대한 최대 잠재 시장을 창출합니다. 이러한 생산 규모로 중국은 일본, 한국, 인도 등 다른 지역 시장을 크게 앞지르고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정의 주요 동향

1차 조사와 검증

1차 정보

예측

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

전기자동차의 보급 확대

에너지 효율과 지속가능성

차량의 전동화

정부 정책 및 인센티브

GaN 기술의 진보

업계의 잠재적 위험 및 과제

높은 초기 비용

통합의 과제

시장 기회

재생에너지와의 통합

고출력 산업용 차량 충전

공공 충전 네트워크의 확대

스마트 충전 및 그리드 관리

성장 가능성 분석

규제 상황

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

신흥기술

GaN 디바이스의 아키텍처와 기술 변형

수평형 GaN HEMT 아키텍처(300-650V 상용)

수직형 GaN 개발 로드맵(목표 전압 1.2kV 초과)

양방향 GaN 스위치(BDS) 기술

와이드 밴드갭 반도체 기술의 최신 동향

실리콘(Si)의 기준 성능과 한계

GaN 기술의 개요와 장점

탄화규소(SiC) 기술 개요

GaN과 실리콘의 성능 비교

특허 분석

가격 동향 분석

컴포넌트별

지역별

비용 내역 분석

생산 통계

생산 거점

소비 거점

수출과 수입

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제조 공정과 비용 구조

GaN 디바이스의 제조 공정 흐름

에피택셜 성장(MOCVD, MBE)

웨이퍼 가공 및 리소그래피

다이싱 및 패키징

시험 및 품질 관리

제조 비용 내역($/kW)

열 관리에 관한 고려 사항

높은 스위칭 주파수의 방열 과제

방열판 설계 및 최적화

액체 냉각과 공냉의 비교

열전도 인터페이스 재료

접합부 온도 관리

전자 양립성(EMI/EMC)에의 적합과 대책

고전압차(DV/DT) 및 고전류차(DI/DT)의 과제

전도성 방출

방사 방출

GaN 충전기용 EMI 필터 설계

PCB 레이아웃 베스트 프랙티스

실드 및 접지 대책

신뢰성 및 인증 기준

AEC-Q101(자동차용 이산 반도체)

AEC-Q100(자동차용 집적 회로)

자동차용 인증 요건

장기 신뢰성 시험

게이트 산화막의 신뢰성

동적 온 저항 열화

무역분석과 수출입 동향

세계 GaN 디바이스의 무역 동향

주요 수출국(중국, 대만, 독일, 미국)

주요 수입국

관세 및 무역 장벽

무역정책의 영향(미중관계)

리쇼어링 및 니어 쇼어링의 동향

사례 연구와 실세계의 도입 사례

ORNL 6.6 kW GaN 차재 충전기 실증 시험

델타 일렉트로닉스사에 의한 GaN 충전기의 도입

인피니언사 300mm GaN 파일럿 생산

Navitas GaNFast IC의 자동차 설계 채택 실적

차지 포인트사제 GaN 대응 직류 급속 충전기

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 뉴스와 대처

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

주요 동향

차재 충전기

차재외 충전기

차량

상업용

공공/고출력

제6장 시장 추계 및 예측 : 충전 용량별(2021-2034년)

주요 동향

11kW 미만

11-22kW

22kW 초과

제7장 시장 추계 및 예측 : 차량별(2021-2034년)

주요 동향

승용차

해치백

세단

SUV

상용차

LCV

MCV

대형 상용차(HCV)

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

주택용

상업용

공공

산업용

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

주요 동향

OEM

애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

네덜란드

러시아

아시아태평양

중국

인도

일본

ANZ

싱가포르

태국

베트남

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계적 기업

ABB E-Mobility

Infineon Technologies

ON Semiconductor

Power Integrations

Renesas Electronics(Transphorm)

ROHM Semiconductor

Schneider Electric

Siemens eMobility

STMicroelectronics

Texas Instruments

지역 기업

BTC Power

ChargePoint

EVBox(Engie)

GaN Systems

Nexperia

Panasonic

Tritium

Wallbox

VisIC Technologies

Chanan

신흥 기업 및 디스랩터

Cambridge GaN Devices(CGD)

EPC

Innoscience Technology

Navitas Semiconductor

11.3.5 Odyssey Semiconductor Technologies

HBR

영문 목차

영문목차

The Global Gallium Nitride (GaN) EV Charger Market was valued at USD 1.14 billion in 2024 and is estimated to grow at a CAGR of 24.3% to reach USD 9.77 billion by 2034.

The market is transitioning from standalone discrete devices to integrated half-bridge stages and modules that combine GaN switches with drivers and protection features. This integration reduces layout sensitivity and EMI while improving thermal performance. Public-private initiatives have accelerated the commercialization of wide-bandgap (WBG) technologies, driving the adoption of integrated GaN solutions for onboard chargers (OBCs) and electric vehicle power systems. Automakers are increasingly integrating multifunctional power domains, which support higher levels of device integration. Demonstrations of OBC converters indicate that GaN can increase power density by 170% and reduce weight by 79% compared to silicon-based systems, achieving peak efficiencies of 99% in a 6.6 kW dual active bridge prototype. GaN devices can switch at higher frequencies with lower conduction losses than silicon, allowing smaller magnetics and cooling systems while reducing losses by 60-80% in advanced EV converters. Design teams are also optimizing switching frequencies to balance converter performance with motor parasitic losses. Research has shown that 1.2 kV GaN MOSFETs using high-HfO2 gate dielectrics achieve very low gate leakage and higher current density. This positions vertical GaN devices to compete with SiC for 1.2 kV applications once substrate and process technologies mature. However, automotive qualification for 800 V+ and 150 kW traction applications remains under development, with readiness expected toward the end of the decade due to cost and reliability considerations.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.14 Billion

Forecast Value

$9.77 Billion

CAGR

24.3%

The lateral GaN devices segment held 70% share and is forecasted to grow at a CAGR of 16.1% from 2025 to 2034. Lateral GaN devices dominate EV power electronics for OBCs, DC-DC converters, and auxiliary systems up to 650 V. Their AlGaN/GaN HEMT structure on silicon provides high electron mobility and critical field strength, delivering low on-resistance at high blocking voltages compared to silicon.

The medium voltage segment (100-650 V) accounted for a 67% share in 2024 and is projected to grow at a CAGR of 16% through 2034. Mid-voltage GaN devices are widely deployed because most OBCs (400 V today, rising to 800 V) and many DC-DC converters fall within this range. GaN's high-frequency performance directly boosts efficiency and power density in power factor correction and LLC or resonant converter stages in 6.6-19.2 kW OBC systems.

China Gallium Nitride (GaN) EV Charger Market generated USD 73.4 million in 2024. Accounting for nearly two-thirds of global EV sales, China's scale generates the largest addressable market for GaN devices, as every EV requires onboard chargers, DC-DC converters, and compatible charging infrastructure. This production volume positions China far ahead of other regional markets like Japan, South Korea, and India.

Key players in the Global Gallium Nitride (GaN) EV Charger Market include Transphorm, Navitas, Texas Instruments, GaN Systems, EPC, STMicroelectronics, ROHM Semiconductor, Infineon Technologies, Innoscience, and Power Integrations. Companies are strengthening their position by investing in R&D to improve GaN device performance, efficiency, and reliability. Strategic collaborations with automakers and charger manufacturers accelerate adoption. Expanding product portfolios with medium- and high-voltage solutions, securing automotive qualification certifications, and developing integrated modules enhances market penetration. Firms also focus on reducing costs through substrate innovations, scaling production capacity, and optimizing supply chains.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Product

2.2.2 Charging capacity

2.2.3 Vehicle

2.2.4 Application

2.2.5 Distribution channel

2.2.6 Regional

2.3 TAM Analysis, 2026-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising EV adoption

3.2.1.2 Energy efficiency and sustainability

3.2.1.3 Electrification of fleets

3.2.1.4 Government policies and incentives

3.2.1.5 Technological advancements in GaN

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial cost

3.2.2.2 Integration challenges

3.2.3 Market opportunities

3.2.3.1 Integration with renewable energy

3.2.3.2 High-power industrial fleet charging

3.2.3.3 Expansion of public charging networks

3.2.3.4 Smart charging and grid management

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle east and Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technology

3.7.2 Emerging technology

3.7.3 GaN device architectures & technology variants

3.7.3.1 Lateral GaN hemt architecture (300-650v commercial)

3.7.3.2 Vertical GaN development roadmap (>1.2 kv target)