의료기기 정비 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Medical Equipment Maintenance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1885859

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 140 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

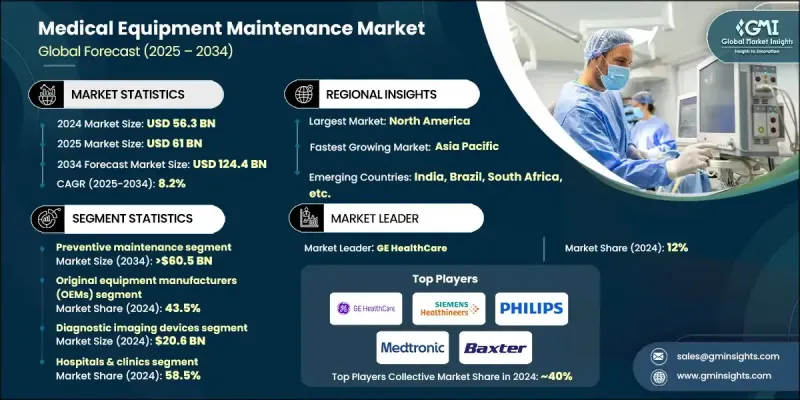

세계의 의료기기 정비 시장은 2024년 563억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 8.2%로 성장할 전망이며, 1,244억 달러에 달할 것으로 예측되고 있습니다.

시장 성장은 환자 안전 중시, 재생 의료기기 및 첨단 의료기기의 도입 증가, 만성 질환의 유병률 상승, 의료기기 유지 관리에 대한 엄격한 규제 요건에 의해 견인되고 있습니다. 병원 및 클리닉에서는 환자 관리 및 안전을 손상시킬 수 있는 장비 고장으로 인한 위험 최소화에 주력하고 있습니다. 예방 보전 프로그램은 장비가 안전한 매개 변수 내에서 작동하는지 확인하고 오류를 줄이고 규정 준수를 유지하기 위해 널리 채택되었습니다. 신뢰성, 운영 효율성 및 모니터링의 필요성이 증가함에 따라 의료 제공업체는 계획된 유지 보수 전략을 선택하고 시장 확대를 촉진하고 있습니다. 이 분야의 유지보수는 의료기기의 정기적인 점검, 정비, 수리, 교정을 포함하여 의료시설 전체에서 최적의 성능, 안전성, 기기의 수명 연장을 확보합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 시 가치

563억 달러

예측 금액

1,244억 달러

CAGR

8.2%

예방 보전 부문은 2024년 47.2%의 점유율을 차지했습니다. 이 부문의 성장은 소규모 의료 시설을 위해 설계된 비용 효율적인 유지 보수 솔루션에 의해 지원됩니다. 예방 유지 보수는 정기 점검, 교정 및 정비를 포함하여 예기치 않은 장비 고장을 줄이고 최상의 성능을 유지합니다. 잠재적인 문제를 조기에 파악하고 해결함으로써 가동 중지 시간을 최소화하고 장비 수명을 연장하며 환자의 안전을 향상시킵니다. 병원은 규제 준수 및 긴급 수리와 관련된 비용 절감을 위해 이러한 프로그램을 점차 채택하고 있습니다.

오리지널 장비 제조업체(OEM) 부문은 2024년 43.5%의 점유율을 차지했습니다. OEM은 주문을 받아서 만들어진 서비스, 규격에 근거한 부속 및 기술적인 전문 지식을 제공해서 주도권을 유지합니다. 이 전략에는 장기 서비스 계약, 예지 보전 및 원격 모니터링이 포함되며, 종종 디지털 플랫폼에 의해 지원됩니다. OEM의 유지 보수는 규제 준수 및 고품질 서비스를 보장하기 위해 중요하고 고가의 의료기기의 우선 공급자입니다.

북미의 의료기기 정비 시장은 2024년에 40.7%의 점유율을 획득했습니다. 이 지역의 첨단 의료 시스템, 신의료 기술의 높은 도입률, 엄격한 규제 기준이 예방 보전 및 예지 보전 수요를 견인하고 있습니다. 주요 OEM은 통합 서비스 계약 및 디지털 솔루션을 제공하는 반면, 독립 서비스 조직(ISO)은 비용 효율적인 외부 위탁 유지보수 옵션을 확대하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

고급 의료기기 도입 확대

만성질환의 급증

환자 안전 및 기기 가동 시간에 대한 주목의 고조

의료기기 정비에 있어서의 규제 준수 요건

재생 의료기기의 높은 채용률

업계의 잠재적 위험 및 과제

유지 보수 서비스 및 계약의 높은 비용

복잡한 기기에 대응할 수 있는 숙련 기술자의 부족

기회

AI와 IoT를 활용한 예지보전

비용 효율화를 위한 원격 모니터링 솔루션

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

LAMEA

기술과 혁신 동향

현재의 기술 동향

신흥 기술

서비스 계약 모델 전망

지속가능성 및 그린 유지관리의 대처

Porter's Five Forces 분석

PESTEL 분석

갭 분석

원격 감시 및 텔레 유지관리의 통합

장래 시장 동향

제4장 경쟁 구도

서문

기업 매트릭스 분석

기업의 시장 점유율 분석

세계

북미

유럽

아시아태평양

LAMEA

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신서비스의 개시

확대 계획

제5장 시장 추계 및 예측 : 서비스종별(2021-2034년)

주요 동향

예방 보전

수정 보전

운용 보수

제6장 시장 추계 및 예측 : 서비스 제공업체별(2021-2034년)

주요 동향

오리지널 장비 제조업체(OEM)

사내 보수

독립 서비스 조직(ISO)

제7장 시장 추계 및 예측 : 기기별(2021-2034년)

주요 동향

진단용 화상 장치

전기 의료기기

외과용기구

환자 모니터링 및 생명 유지 장치

치과용 기기

내시경 장치

검사기기

기타 기기

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원 및 진료소

진단 이미지 센터

외래수술센터(ASCs)

치과 진료소

투석 센터

기타 용도

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

Alliance Medical CORPORATION

ALTHEA

Aramark

Baxter

Drive DeVilbiss HEALTHCARE

FUJIFILM

GE HealthCare

GETINGE

Hitachi High-Tech

Medtronic

PHILIPS

Probo MEDICAL

Resmed

SIEMENS Healthineers

STERIS HEALTHCARE

AJY

영문 목차

영문목차

The Global Medical Equipment Maintenance Market was valued at USD 56.3 billion in 2024 and is estimated to grow at a CAGR of 8.2 % to reach USD 124.4 billion by 2034.

Market growth is driven by increasing emphasis on patient safety, rising adoption of refurbished and advanced medical devices, growing prevalence of chronic diseases, and stringent regulatory requirements for medical device upkeep. Hospitals and clinics are focusing on minimizing the risks posed by equipment failure, which can compromise patient care and safety. Preventive maintenance programs are being widely adopted to ensure devices operate within safe parameters, reduce errors, and maintain compliance with regulations. The need for reliability, operational efficiency, and oversight is pushing healthcare providers to opt for planned maintenance strategies, thereby fueling market expansion. Maintenance in this sector includes regular inspection, servicing, repair, and calibration of medical devices, ensuring optimal performance, safety, and longer equipment lifespan across healthcare facilities.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$56.3 Billion

Forecast Value

$124.4 Billion

CAGR

8.2%

The preventive maintenance segment held a 47.2% share in 2024. Growth in this segment is supported by cost-effective maintenance solutions designed for smaller healthcare facilities. Preventive maintenance involves routine inspections, calibration, and servicing to reduce unplanned device failures and maintain peak performance. By identifying and resolving potential issues early, it minimizes downtime, extends equipment life, and enhances patient safety. Hospitals increasingly adopt these programs to comply with regulations and reduce the costs associated with emergency repairs.

The original equipment manufacturers (OEMs) segment held a 43.5% share in 2024. OEMs maintain control by offering tailored service, specification-based parts, and technical expertise. Their strategies include long-term service agreements, predictive maintenance, and remote monitoring, often supported by digital platforms. OEM maintenance guarantees compliance with regulations and high-quality service, making them preferred providers for critical and high-value medical equipment.

North America Medical Equipment Maintenance Market captured 40.7% share in 2024. The region's advanced healthcare systems, high adoption of new medical technologies, and stringent regulatory standards drive demand for preventive and predictive maintenance. Major OEMs in the region provide integrated service contracts and digital solutions, while independent service organizations (ISOs) are increasingly offering cost-effective outsourced maintenance options.

Key players in the Global Medical Equipment Maintenance Market include FUJIFILM, Alliance Medical CORPORATION, Drive DeVilbiss HEALTHCARE, Baxter, Hitachi High-Tech, ALTHEA, STERIS HEALTHCARE, Philips, Aramark, Medtronic, GE Healthcare, Probo MEDICAL, ResMed, and GETINGE, SIEMENS Healthineers. Companies are strengthening their presence by investing in advanced digital maintenance platforms, predictive maintenance technologies, and remote monitoring solutions. Strategic partnerships, mergers, and acquisitions allow expansion into new regions and healthcare segments. Offering customized service contracts, including preventive and emergency maintenance packages, enhances customer loyalty. Firms focus on regulatory compliance, certifications, and training programs to build credibility and trust. Additionally, outsourcing solutions via ISOs provides cost-effective alternatives to hospitals, while innovation in maintenance solutions ensures reduced downtime, improved efficiency, and higher patient safety, reinforcing long-term market positioning.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Service type trends

2.2.3 Service provider trends

2.2.4 Equipment trends

2.2.5 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising adoption of advanced medical devices

3.2.1.2 Surging prevalence of chronic diseases

3.2.1.3 Growing focus on patient safety and equipment uptime

3.2.1.4 Regulatory compliance requirements for medical device maintenance

3.2.1.5 High adoption of refurbished medical equipment

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of maintenance services and contracts

3.2.2.2 Shortage of skilled technicians for complex devices

3.2.3 Opportunities

3.2.3.1 Predictive maintenance using AI and IoT

3.2.3.2 Remote monitoring solutions for cost efficiency

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 LAMEA

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Service contract models outlook

3.7 Sustainability and green maintenance initiatives

3.8 Porter's analysis

3.9 PESTEL analysis

3.10 Gap analysis

3.11 Integration of remote monitoring and tele-maintenance

3.12 Future market trends

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis

4.3.1 Global

4.3.2 North America

4.3.3 Europe

4.3.4 Asia Pacific

4.3.5 LAMEA

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New service launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service Type, 2021 - 2034 ($ Mn)

5.1 Key trends

5.2 Preventive maintenance

5.3 Corrective maintenance

5.4 Operational maintenance

Chapter 6 Market Estimates and Forecast, By Service Provider, 2021 - 2034 ($ Mn)

6.1 Key trends

6.2 Original equipment manufacturers (OEMs)

6.3 In-house maintenance

6.4 Independent service organizations (ISOs)

Chapter 7 Market Estimates and Forecast, By Equipment, 2021 - 2034 ($ Mn)

7.1 Key trends

7.2 Diagnostic imaging devices

7.3 Electromedical devices

7.4 Surgical instruments

7.5 Patient monitoring and life support devices

7.6 Dental equipment

7.7 Endoscopic devices

7.8 Laboratory equipment

7.9 Other equipment

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

8.1 Key trends

8.2 Hospitals & clinics

8.3 Diagnostic imaging centers

8.4 Ambulatory surgical centers (ASCs)

8.5 Dental clinics

8.6 Dialysis centers

8.7 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)