AI 기반 병리 분석 시스템 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

AI-Powered Pathology Analysis System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1885795

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 150 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

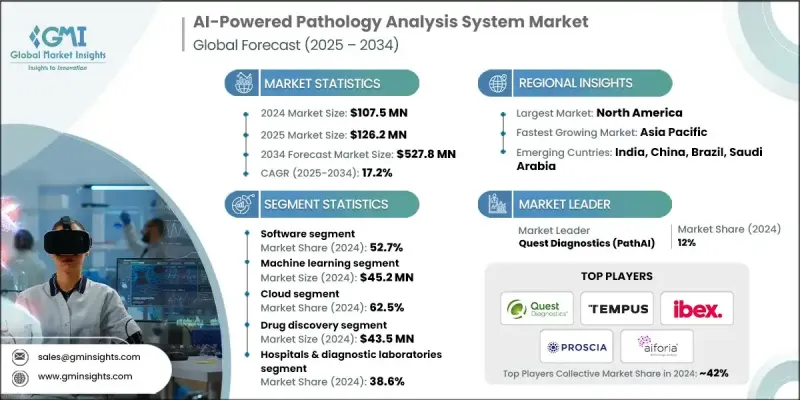

세계의 AI 기반 병리 분석 시스템 시장은 2024년에 1억 750만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 17.2%로 성장할 전망이며, 5억 2,780만 달러에 달할 것으로 예측되고 있습니다.

시장 확대의 주요 요인은 디지털 병리학 및 원격 병리 진단의 보급 확대, 보다 신속하고 정확한 진단 결과에 대한 수요 증가, 만성 질환의 유병률 상승, AI 알고리즘의 지속적인 진보를 포함합니다. 숙련 병리의 부족이 자동화 솔루션의 도입을 촉진하는 한편, AI와 유전체 데이터 및 멀티오믹스 데이터의 통합으로 진보된 진단 능력이 창출되고 있습니다. 디지털 병리학은 고해상도 슬라이드 이미지에 원격으로 액세스할 수 있게 하여 지역을 넘어서는 공동 작업을 촉진합니다. 원격 병리학은 전문가가 원격지에서 증례 상담을 할 수 있게 합니다. AI 기반 플랫폼은 이미지 분석을 강화하고 의사 결정을 지원하며 전문가가 검토하기 전에 실시간 품질 관리를 제공합니다. 이 시스템은 인공지능을 활용하여 의료 영상을 분석하고, 질병 패턴을 감지하며, 병리학자가 더 빠르고 일관성 있고 정밀한 진단을 달성할 수 있도록 지원합니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 시 가치

1억 750만 달러

예측 금액

5억 2,780만 달러

CAGR

17.2%

소프트웨어 부문은 임상시험에서 채용 증가를 배경으로 2024년에 52.7%의 점유율을 창출했습니다. 병원과 연구소에서는 워크플로우 자동화 및 전자건강기록(EHR) 시스템과의 통합을 목적으로 한 소프트웨어 솔루션의 도입이 확대되어 효율성과 생산성 향상에 기여하고 있습니다.

머신러닝 부문은 2024년 4,520만 달러로 평가되었습니다. 이는 컨벌루션 신경망(CNN)과 생성 적대 네트워크(GAN)와 같은 머신러닝 알고리즘이 복잡한 조직 병리학적 패턴을 분석하고 질병의 조기 발견을 지원하기 때문입니다.

북미의 AI 기반 병리 분석 시스템 시장은 2024년에 47.7%의 점유율을 차지했습니다. 이 지역은 첨단 의료 인프라, 디지털 병리의 높은 보급률, AI 연구에 많은 투자가 있다는 장점이 있습니다. TEMPUS, PHILIPS, PROSCIA 등 주요 미국 기업들은 병원 및 제약 기업과 협력하여 진단, 바이오마커 개발, 임상시험에서 AI 솔루션을 도입하고 있습니다. 규제의 명확화 및 전자건강기록(EHR) 시스템의 통합은 이 지역에서의 도입과 전개를 더욱 뒷받침하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

진단 결과의 신속화 및 정밀도 향상 수요 증가

만성 질환 증가 경향

AI 알고리즘의 진보

디지털 병리학 및 원격 병리 진단의 보급 확대

업계의 잠재적 위험 및 과제

규제 승인의 복잡성

데이터 프라이버시 및 보안에 대한 우려

시장 기회

암 검진 및 조기 발견 프로그램에 있어서 AI 통합에 대한 주목의 고조

클라우드 기반 AI 병리 플랫폼 개발

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

기술 및 혁신 동향

현재의 기술 동향

신흥 기술

새로운 용도 및 이용 사례

투자 및 자금 조달 환경

정책의 진화 및 변화

상환 시나리오

Porter's Five Forces 분석

PESTEL 분석

갭 분석

장래 시장 동향

제4장 경쟁 구도

서문

기업 매트릭스 분석

기업의 시장 점유율 분석

세계

북미

유럽

아시아태평양

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 공동 사업

신제품 발매

사업 확대 계획

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

주요 동향

소프트웨어

화상 해석 및 패턴 인식

예측 분석 도구

워크플로우 자동화 소프트웨어

진단 의사 결정 지원

하드웨어

전체 슬라이드 이미징(WSI) 스캐너

디지털 병리 시스템

현미경

스토리지 시스템

서비스

도입 및 통합

컨설팅 및 트레이닝

매니지드 AI 서비스

보수 및 서포트

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

머신러닝(ML)

컨벌루션 신경망(CNN)

생성적 적대 네트워크(GAN)

재귀형 신경망(RNNS)

기타 신경망

컴퓨터 비전에 기반한 이미지 분석

자연언어처리(NLP)

제7장 시장 추계 및 예측 : 도입 형태별(2021-2034년)

주요 동향

클라우드

온프레미스

제8장 시장 추계 및 예측 : 이용 사례별(2021-2034년)

주요 동향

창약

질병의 진단 및 예후

임상 워크플로우

연수 및 교육

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

병원 및 진단실험실

생명과학 기업

연구기관 및 학술센터

기타 최종 용도

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

aetherAI

aiforia

Aiosyn

deep bio

HOLOGIC

IBEX

indica labs

KFBIO

mindpeak

PHILIPS

PROSCIA

QRITIVE

Quest Diagnostics(PathAI)

Roche

TEMPUS

tribun HEALTH

VISIOPHARM

AJY

영문 목차

영문목차

The Global AI-Powered Pathology Analysis System Market was valued at USD 107.5 million in 2024 and is estimated to grow at a CAGR of 17.2% to reach USD 527.8 million by 2034.

The market expansion is driven by the rising adoption of digital pathology and telepathology, the growing need for faster and more accurate diagnostic results, the increasing prevalence of chronic diseases, and continuous advancements in AI algorithms. Shortages of skilled pathologists are encouraging the adoption of automated solutions, while integration of AI with genomic and multi-omics data is creating advanced diagnostic capabilities. Digital pathology enables remote access to high-resolution slide images, facilitating collaboration across geographies, and telepathology allows specialists to consult on cases from distant locations. AI-powered platforms enhance image analysis, support decision-making, and offer real-time quality control prior to expert review. These systems utilize artificial intelligence to analyze medical images, detect disease patterns, and assist pathologists in achieving faster, more consistent, and highly accurate diagnoses.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$107.5 Million

Forecast Value

$527.8 Million

CAGR

17.2%

The software segment held a 52.7% share in 2024, driven by rising adoption in drug discovery and clinical trials. Hospitals and laboratories are increasingly deploying software solutions to automate workflows and integrate with electronic health record (EHR) systems, enhancing efficiency and productivity.

The machine learning segment was valued at USD 45.2 million in 2024, as machine learning algorithms, including convolutional neural networks (CNNs) and generative adversarial networks (GANs), enable analysis of complex histopathological patterns, supporting early disease detection.

North America AI-Powered Pathology Analysis System Market held a 47.7% share in 2024. The region benefits from advanced healthcare infrastructure, high adoption of digital pathology, and substantial investments in AI research. Key US companies, including TEMPUS, PHILIPS, and PROSCIA, are collaborating with hospitals and pharmaceutical firms to deploy AI solutions in diagnostics, biomarker development, and clinical trials. Regulatory clarity and integration with EHR systems further support adoption and deployment in the region.

Leading companies in the AI-Powered Pathology Analysis System Market include IBEX, HOLOGIC, QRITIVE, Tribune Health, aiforia, Aiosyn, Mindpeak, VISIOPHARM, PathAI, Roche, Quest Diagnostics, PHILIPS, TEMPUS, Deep Bio, KFBIO, and Indica Labs. Market players are strengthening their position by investing in R&D to enhance algorithm accuracy and expand diagnostic capabilities. They are forming strategic partnerships with hospitals, laboratories, and pharmaceutical firms, while scaling software deployment and AI integration across clinical workflows. Geographic expansion, acquisitions, and collaborations are also central strategies, along with integrating platforms with EHR systems to improve interoperability. Companies focus on launching advanced analytics tools, machine learning-based solutions, and AI-powered workflow automation to solidify their market presence and accelerate adoption in diagnostics, drug development, and clinical research.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Component trends

2.2.3 Technology trends

2.2.4 Deployment mode trends

2.2.5 Use case trends

2.2.6 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing demand for faster diagnostic turnaround time with improved accuracy

3.2.1.2 Rising prevalence of chronic diseases

3.2.1.3 Advancements in AI algorithms

3.2.1.4 Growing adoption of digital pathology and telepathology

3.2.2 Industry pitfalls and challenges

3.2.2.1 Regulatory approval complexities

3.2.2.2 Data privacy & security concerns

3.2.3 Market opportunities

3.2.3.1 Increasing focus on AI integration in cancer screening and early detection programs

3.2.3.2 Development of cloud-based AI pathology platforms

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Emerging applications and use cases

3.7 Investment and funding landscape

3.8 Policy evolution and changes

3.9 Reimbursement scenario

3.10 Porter's analysis

3.11 PESTEL analysis

3.12 Gap analysis

3.13 Future market trends

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis

4.3.1 Global

4.3.2 North America

4.3.3 Europe

4.3.4 Asia Pacific

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers and acquisitions

4.6.2 Partnerships and collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

5.1 Key trends

5.2 Software

5.2.1 Image analysis & pattern recognition

5.2.2 Predictive analytics tools

5.2.3 Workflow automation software

5.2.4 Diagnostic decision support

5.3 Hardware

5.3.1 Whole slide imaging (WSI) scanners

5.3.2 Digital pathology systems

5.3.3 Microscopes

5.3.4 Storage systems

5.4 Services

5.4.1 Implementation & integration

5.4.2 Consulting & training

5.4.3 Managed AI services

5.4.4 Maintenance & support

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

6.1 Key trends

6.2 Machine learning (ML)

6.2.1 Convolutional neural networks (CNNS)

6.2.2 Generative adversarial networks (GANS)

6.2.3 Recurrent neural networks (RNNS)

6.2.4 Other neural networks

6.3 Computer vision-based image analysis

6.4 Natural language processing (NLP)

Chapter 7 Market Estimates and Forecast, By Deployment Mode, 2021 - 2034 ($ Mn)

7.1 Key trends

7.2 Cloud

7.3 On-premise

Chapter 8 Market Estimates and Forecast, By Use Case, 2021 - 2034 ($ Mn)

8.1 Key trends

8.2 Drug discovery

8.3 Disease diagnosis & prognosis

8.4 Clinical workflow

8.5 Training & education

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

9.1 Key trends

9.2 Hospitals & diagnostic laboratories

9.3 Life sciences companies

9.4 Research institutes & academic centers

9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)