Cold Plates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1876803

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

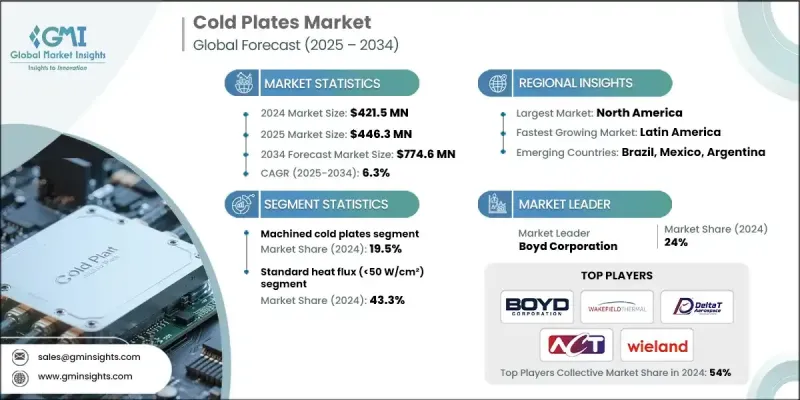

세계의 콜드 플레이트 시장은 2024년에 4억 2,150만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 6.3%로 성장하여 7억 7,460만 달러에 이를 것으로 예측됩니다.

이러한 성장은 효율적인 열 관리 솔루션을 필요로 하는 전기자동차(EV), 재생 에너지 시스템 및 첨단 컴퓨팅 용도의 채택 증가에 의해 주도되고 있습니다. 콜드 플레이트는 파워 일렉트로닉스, 배터리, 반도체 부품에서 과도한 열을 제거하여 시스템의 신뢰성과 성능을 보장하는 데 필수적입니다. 고성능 컴퓨팅, 5G 인프라, 에너지 저장에 대한 투자 증가로 인해 혁신적인 액체 냉각 기술에 대한 수요가 증가하고 있습니다. 제조업체들은 자동차, 항공우주, 산업 분야의 요구에 부응하기 위해 알루미늄, 구리 등의 소재를 이용한 소형, 경량, 고효율 냉각 시스템 개발에 주력하고 있습니다.

시장 범위

개시 연도

2024년

예측 기간

2025-2034년

시작 금액

4억 2,150만 달러

예측 금액

7억 7,460만 달러

CAGR

6.3%

2024년 열전달 등급이 50W/cm2 미만인 표준 열유속 용량 부문은 43.3%의 점유율을 차지했습니다. 이 카테고리는 주로 산업용 전자제품, 자동차 시스템 및 다양한 일반 열 관리 용도를 대상으로 합니다. 이 부문은 대규모 제조 체제를 구축하여 다양한 산업 분야에서 일상적인 사용에 특화된 비용 효율적인 솔루션을 제공합니다.

가공 냉판 부문은 2024년 19.5%의 점유율을 차지했으며, 2034년까지 연평균 6.4%의 성장률을 보일 것으로 전망됩니다. 이러한 솔루션은 정밀 CNC 가공과 특수 브레이징 공정을 통해 뛰어난 사용자 정의성을 제공합니다. 첨단 반도체, 클라우드 컴퓨팅, AI 기반 시스템 등 까다로운 환경에서 복잡한 유로 설계, 정밀한 장착 요구 사항, 열 전달 효율을 높이는 핀 인서트 통합에 적합합니다.

북미 콜드 플레이트 시장은 2024년 33.4%의 점유율을 차지했으며, 2034년까지 5.6%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이 지역의 우위는 첨단 기술 인프라와 항공우주, 데이터센터, 의료기기 등 주요 분야에서 열 관리 솔루션이 광범위하게 채택되고 있는 데서 기인합니다. 주요 산업 기업의 존재, 활발한 R&D 활동, 고성능 전자기기를 지원하는 고효율 냉각 시스템에 대한 수요 증가는 이 지역의 기술 혁신과 시장의 지속적인 확장을 주도하고 있습니다.

보이 코퍼레이션, 다나 주식회사, TE 테크놀로지, 가와소 텍셀, 메르센, 팬트로닉스 인도, 웨이크필드 써멀 솔루션즈, 빌랜드 써멀 솔루션즈, 테시오, QATS, 켐파 테크, 델타 T 에어로스페이스, ACT, 어드밴스드 쿨링 테크놀로지스 등 Delta T Aerospace, Advanced Cooling Technologies(ACT)와 같은 세계 콜드 플레이트 시장의 주요 기업들은 시장에서의 입지를 강화하기 위해 기술 혁신, 전략적 제휴, 생산 능력 확대에 주력하고 있습니다. 이들 기업은 설계 유연성과 열 성능을 향상시키기 위해 적층 가공 및 정밀 가공과 같은 첨단 제조 공정에 투자하고 있습니다. 전기자동차 제조업체, 항공우주 기업, 데이터센터 사업자와의 전략적 제휴를 통해 고성능 냉각 요구사항에 맞는 맞춤형 솔루션을 제공할 수 있게 되었습니다. 또한, 환경 부하를 줄이기 위해 지속가능성을 중시하고, 경량화 및 재활용이 가능한 소재와 친환경 냉각제 개발에 힘쓰고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

이익률

각 단계 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

소재 유형별

향후 시장 동향

기술과 혁신 동향

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병(M&A)

제휴·협력 관계

신제품 발매

사업 확대 계획

제5장 시장 추산·예측 : 재질별, 2021-2034

주요 동향

구리

알루미늄

스테인리스 스틸

하이브리드

기타

제6장 시장 추산·예측 : 기술별, 2021-2034

주요 동향

프레스 가공 콜드 플레이트

기계 가공 콜드 플레이트

마이크로채널 콜드 플레이트

성형 튜브 콜드 플레이트

플랫 튜브 콜드 플레이트

심부 드릴링 콜드 플레이트

제7장 시장 추산·예측 : 열류속용량별, 2021-2034

주요 동향

Standard heat flux (<50 W/cm²)

High heat flux (50-200 W/cm²)

Very high heat flux (200-500 W/cm²)

Ultra-high heat flux (>500 W/cm²)

제8장 시장 추산·예측 : 용도별, 2021-2034

주요 동향

데이터센터

전기자동차

항공우주 및 방위

산업용 전자기기

의료기기

통신장비

기타

제9장 시장 추산·예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카공화국

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 개요

Advanced Cooling Technologies(ACT)

Boyd Corporation

Dana Incorporated

DeltaT Aerospace

Kawaso Texcel

KenFa Tech.

Mersen

Pantronics India

QATS

TE Technology, Inc

Tesio

Wakefield Thermal Solutions

Wieland Thermal Solutions

LSH

영문 목차

영문목차

The Global Cold Plates Market was valued at USD 421.5 million in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 774.6 million by 2034.

The growth is driven by the rising adoption of electric vehicles (EVs), renewable energy systems, and advanced computing applications that require efficient thermal management solutions. Cold plates are essential for removing excess heat from power electronics, batteries, and semiconductor components, ensuring system reliability and performance. Increasing investments in high-performance computing, 5G infrastructure, and energy storage are boosting demand for innovative liquid-cooled technologies. Manufacturers are focusing on developing compact, lightweight, and high-efficiency cooling systems using materials such as aluminum and copper to meet the needs of automotive, aerospace, and industrial sectors.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$421.5 Million

Forecast Value

$774.6 Million

CAGR

6.3%

In 2024, the standard heat flux capacity segment, requiring a heat transfer rating below 50 W/cm2, held a 43.3% share. This category primarily serves industrial electronics, automotive systems, and a range of general thermal management applications. Owing to its well-established large-scale manufacturing, this segment delivers cost-effective solutions tailored for everyday use across diverse industries.

The machined cold plates segment captured a 19.5% share in 2024 and is projected to grow at a CAGR of 6.4%. These solutions offer superior customization capabilities through precision CNC machining and specialized brazing processes. They are ideal for intricate flow path designs, precise mounting requirements, and the integration of fin inserts that enhance heat transfer efficiency in demanding environments such as advanced semiconductors, cloud computing, and AI-based systems.

North America Cold Plates Market held 33.4% share in 2024 with a CAGR of 5.6% through 2034. The region's dominance is supported by its advanced technological infrastructure and widespread adoption of thermal management solutions across key sectors, including aerospace, data centers, and medical equipment. The presence of leading industry players, strong R&D activities, and the growing need for high-efficiency cooling systems to support high-performance electronics are driving innovation and continued market expansion in the region.

Leading players in the Global Cold Plates Market, such as Boyd Corporation, Dana Incorporated, TE Technology, Inc., Kawaso Texcel, Mersen, Pantronics India, Wakefield Thermal Solutions, Wieland Thermal Solutions, Tesio, QATS, KenFa Tech., DeltaT Aerospace, Advanced Cooling Technologies (ACT), are focusing on technological innovation, strategic partnerships, and capacity expansion to strengthen their market position. These companies are investing in advanced manufacturing processes like additive manufacturing and precision machining to enhance design flexibility and thermal performance. Strategic collaborations with EV manufacturers, aerospace firms, and data center operators are enabling customized solutions tailored to high-performance cooling requirements. Firms are emphasizing sustainability, developing lightweight recyclable materials, and eco-friendly coolants to reduce environmental impact.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Material type

2.2.3 Technology

2.2.4 Heat flux capacity

2.2.5 Application

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By material type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Million & Kilo Tons)

5.1 Key trends

5.2 Copper

5.3 Aluminum

5.4 Stainless steel

5.5 Hybrid

5.6 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million & Kilo Tons)

6.1 Key trends

6.2 Stamped cold plates

6.3 Machined cold plates

6.4 Microchannel cold plates

6.5 Formed tube cold plates

6.6 Flat tube cold plates

6.7 Deep drilled cold plates

Chapter 7 Market Estimates and Forecast, By Heat Flux Capacity, 2021-2034 (USD Million & Kilo Tons)

7.1 Key trend

7.2 Standard heat flux (<50 W/cm²)

7.3 High heat flux (50-200 W/cm²)

7.4 Very high heat flux (200-500 W/cm²)

7.5 Ultra-high heat flux (>500 W/cm²)

Chapter 8 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

8.1 Key trends

8.2 Data centres

8.3 Electric vehicles

8.4 Aerospace & defense

8.5 Industrial electronics

8.6 Medical equipment

8.7 Telecommunication equipment

8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)