스마트 윈도우용 서모크로믹 재료 시장 : 시장 기회, 성장 촉진요인, 업계 동향 분석, 예측(2025-2034년)

Thermochromic Materials for Smart Windows Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1876659

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

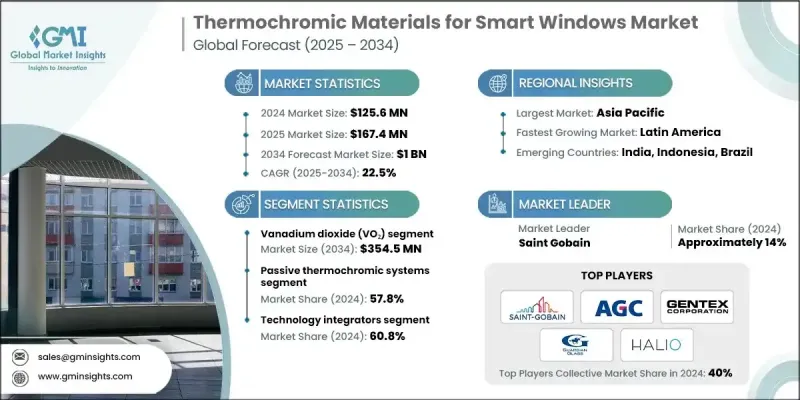

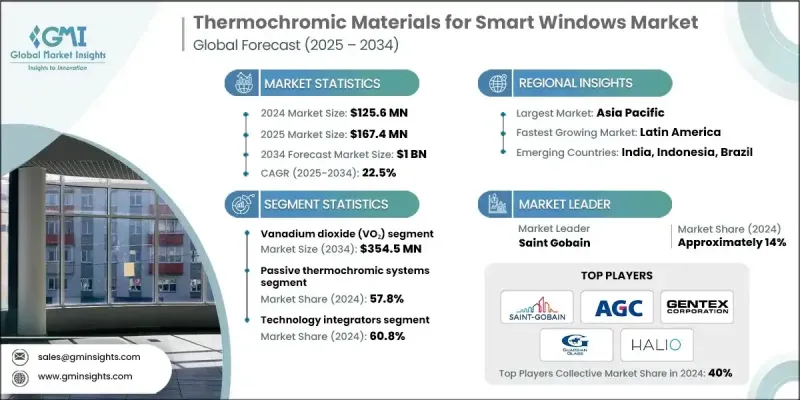

세계의 스마트 윈도우용 서모크로믹 재료 시장은 2024년 1억 2,560만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 22.5%로 성장할 전망이며, 10억 달러에 이를 것으로 예측됩니다.

이 급성장은 건축물의 에너지 규제 강화, 서모크로믹 화학 기술의 급속한 진보 및 지능형 건축 기술의 보급 확대를 반영합니다. 온도에 따라 색조를 변화시키는 스마트 윈도우는 실내 환경을 보다 효율적으로 조절하기 때문에 자동화 건축 플랫폼과의 조합이 점점 더 진행되고 있습니다. 이는 HVAC 시스템이 상업 시설의 에너지 소비량의 40%에서 60%를 차지할 수 있다는 점을 고려하면 큰 이점입니다. 넷 제로 에너지 건축을 추진하는 프로그램은 외부 전원을 필요로 하지 않고 표준 창 시스템에 비해 총 에너지 사용량을 대폭 줄일 수 있는 열변색성 유리를 지속적으로 추천하고 있습니다. 페로브스카이트 혼합물, VO2 코팅, 기타 조정가능한 필름 등 다층을 통합한 재료 플랫폼이 진화를 계속하고 있으며, 높은 가시광 투과율과 강화된 일사 제어를 실현하고 있습니다. 강력한 전년 대비 성장은 건축 기준의 갱신, 지속적인 재료 기술 혁신 및 신흥 하이브리드 기술에 기인합니다. 설문 조사는 계속 활발하게 진행되고 있으며, 내구성 향상과 전환 속도가 빨라짐에 따라 현대의 서모크로믹 필름은 보다 광범위한 상업용 수용을 위해 자리를 잡고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 금액

1억 2,560만 달러

예측 금액

10억 달러

CAGR

22.5%

이산화바나듐 부문은 2024년에 4,370만 달러의 수익을 창출하였고, 2034년까지 연평균 복합 성장률(CAGR) 22.3%로 성장할 전망이며, 3억 5,450만 달러에 이를 것으로 예측됩니다. 68℃ 부근에서 발생하는 천연의 금속-절연체 전이는 선택적 도핑에 의해 저온에서의 활성화가 가능하며, 현재는 확장 가능한 생산 기술에 의해 22℃ 부근에서의 전이를 실현하고 있습니다. 스퍼터링 기술의 발전으로 코팅의 안정성이 향상되고 다양한 기후 조건 하에서 장기 성능이 확대되고 있습니다.

수동형 서모크로믹 솔루션 부문은 2024년에 57.8%의 점유율을 차지하였으며, 2034년까지 연평균 복합 성장률(CAGR) 22.4%를 유지할 것으로 예측됩니다. 그 매력은 전력 불필요한 기능성과 최소한의 유지 보수성에 뿌리를 두고 있으며, 넷 제로 건축의 우선 사항과 일치합니다. 적절하게 설계되면 이러한 시스템은 HVAC 비용을 15%에서 25%까지 줄일 수 있음을 입증했으며 운영 비용 상승에 직면하는 소유자에게 점점 매력적인 선택이 되었습니다.

북미의 스마트 윈도우용 서모크로믹 재료 시장은 2024년에 큰 점유율을 차지했습니다. IECC 2021이나 ASHRAE 90.1 등의 규제 갱신에 의해 고효율 건축 외피가 강화되는 가운데, 스마트 윈도우의 채용이 진행되고 있습니다. 미국에서는 주요 건설 시장에서 요구 사항의 진화를 포함한 주 차원의 노력이 보급을 가속화하고 캐나다에서는 협조적인 정책이 장기적인 탄소 감축 목표를 지원하고 있습니다. 이 지역에서는 IoT 대응 빌딩 관리 플랫폼의 강력한 통합과 차세대 유리 시공에 숙련된 성숙한 설치 네트워크가 장점이 되고 있습니다.

스마트 윈도우용 서모크로믹 재료 시장의 주요 기업으로는 ChromeGenics AB, Guardian Glass LLC, View Inc., PPG Industries Inc., Kinestral Technologies, Saint-Gobain SA, AGC Inc., Nippon Sheet Glass Co. Ltd., Gentex Corporation, Halio Inc. 등이 있습니다. 이 시장에서 경쟁하는 기업은 시장에서의 지위를 강화하기 위해 몇 가지 전략적 기둥에 주력하고 있습니다. 많은 기업들이 현대 건축 요건과의 적합성을 높이기 위해 전이 온도, 재료 내구성 및 광학 투명도 향상을 위한 지속적인 연구개발 투자를 중시하고 있습니다. 제조 비용 절감 및 대규모 도입 지원으로 생산 기술의 효율화를 추진하는 기업이 증가하고 있습니다. 유리 제조업체와 스마트 빌딩 솔루션 제공업체와의 전략적 제휴는 상업 프로젝트 진출 기회 확대에 기여하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 리스크 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품 형태별

장래 시장 동향

특허 상황

무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성 및 환경적 측면

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협력관계

신제품 발매

사업 확대 계획

제5장 시장 추계 및 예측 : 재료 유형별(2021-2034년)

주요 동향

이산화바나듐(VO2)계

순수한 VO2계

텅스텐 첨가 VO2

몰리브덴 첨가 VO2

Co 공첨가 VO2계

코어 쉘 구조 VO2 나노 구조체

하이드로겔계

PNIPAM 하이드로겔

HPC(히드록시프로파일셀룰로오스)계

복합 하이드로겔

물리적 가교계

화학적으로 가교된 시스템

페로브스카이트 재료

할로겐화 페로브스카이트

메틸아민 가역성 시스템

수화 반응성 재료

액정계

열 트로픽 액정

콜레스테릭 액정

액정 폴리머 복합재료

유기 색소계

레우코 색소

스피로피란계

LETC(리간드 교환 서모크로미즘)계

제6장 시장 추계 및 예측 : 제품 형태별(2021-2034년)

주요 동향

박막 코팅

스퍼터링 필름

용액 처리 필름

CVD 필름

다층 적층 구조 및 패브리 페로 공진기

적층 중간막

PVB(폴리비닐부티랄) 중간막

EVA(에틸렌 비닐 아세테이트) 중간막

TPU(열가소성 폴리우레탄) 중간막

리트로핏 필름

자기 접착 필름

정전기 흡착 필름

액상 도포 필름

창 시스템 세트

단층 유리 유닛

복층 유리 유닛

삼중 유리 유닛

진공 유리 유닛

제7장 시장 추계 및 예측 : 기술 및 제어별(2021-2034년)

주요 동향

수동형 서모크로믹 시스템

고정 전이 온도

광범위한 스위칭

다단 스위칭

액티브 서모크로믹 시스템

전동 어시스트 시스템

IoT 대응 스마트 윈도우

센서 제어 시스템

하이브리드 시스템

써모크로믹 일렉트로크로믹

써모크로믹 포토볼타이크

써모크로믹 포토크로믹

제8장 시장 추계 및 예측 : 제조 공정별(2021-2034년)

주요 동향

진공 기반의 방법

마그네트론 스퍼터링

HIPIMS(고출력 펄스 마그네트론 스퍼터링)

펄스 레이저 증착법(PLD)

화학 기상 성장법(CVD)

원자층 증착법(ALD)

용액 베이스법

졸루겔법

수열 합성

스핀 코팅

롤 투 롤 코팅

적층 조형

잉크젯 인쇄

스크린 인쇄

3D 프린팅 기술

제9장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

건설 및 건축

종합 건설업자

유리공 사업자

건축설계 사무소

시설 관리 회사

자동차 제조

오리지널 익립먼트 제조업체(OEM)

Tier 1 부품 공급업체

애프터마켓 개수 서비스

유리 제조

플로트 유리 제조업체

코팅 유리 제조업체

적응 유리 제조업체

기술 통합 사업자

빌딩 자동화 시스템 제공 회사

스마트홈 기술기업

IoT 플랫폼 제공업체

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제11장 기업 프로파일

AGC Inc.

ChromoGenics AB

Gentex Corporation

Guardian Glass LLC

Halio Inc.

Heliotrope Technologies

Innovative Glass Corporation

Kinestral Technologies

Miru Smart Technologies

NEXT Energy Technologies

Nippon Sheet Glass Co. Ltd.

Pleotint LLC

Polytronix Inc.

PPG Industries Inc.

RavenWindow

Research Frontiers Inc.

Saint-Gobain SA

Scienstry Inc.

Smartglass International Ltd.

View Inc.

Others

AJY

영문 목차

영문목차

The Global Thermochromic Materials for Smart Windows Market was valued at USD 125.6 million in 2024 and is estimated to grow at a CAGR of 22.5% to reach USD 1 billion by 2034.

The rapid rise reflects stricter building-energy rules, accelerating advances in thermochromic chemistry, and expanding deployment of intelligent building technologies. Smart windows that shift tint based on temperature are increasingly paired with automated building platforms to regulate indoor conditions more efficiently, a major advantage given that HVAC systems can account for 40-60% of commercial facility energy consumption. Programs promoting net-zero energy buildings continue to encourage thermochromic glazing because it functions without external power and can significantly lower total energy use compared with standard window systems. Material platforms integrating multiple layers, such as perovskite blends, VO2 coatings, and other tunable films, are progressing, offering high visible light transmission and enhanced solar control. Strong year-over-year momentum is tied to updated building codes, continuous material breakthroughs, and emerging hybrid technologies. Research efforts remain intensive, with improved durability and faster switching speeds positioning modern thermochromic films for broader commercial acceptance.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$125.6 Million

Forecast Value

$1 Billion

CAGR

22.5%

The vanadium dioxide segment generated USD 43.7 million in 2024 and is expected to reach USD 354.5 million by 2034 at a 22.3% CAGR. The natural metal-insulator shift near 68°C can be re-engineered to activate at lower temperatures through selective doping, with scalable production now achieving transitions near 22°C. Advances in sputtering approaches are enhancing coating stability and extending long-term performance across different climates.

The passive thermochromic solutions segment accounted for a 57.8% share in 2024 and is anticipated to maintain a 22.4% CAGR through 2034. Their appeal is rooted in zero-power functionality and minimal upkeep, aligning with net-zero construction priorities. When designed correctly, these systems have demonstrated 15-25% HVAC savings, making them increasingly attractive for owners facing rising operational costs.

North America Thermochromic Materials for Smart Windows Market held a significant share in 2024. The smart window adoption, as regulatory updates such as IECC 2021 and ASHRAE 90.1 reinforce high-efficiency building envelopes. State-level initiatives, including evolving requirements across major construction markets, accelerate usage in the United States, while coordinated Canadian policies support long-term carbon-reduction goals. The region benefits from strong integration of IoT-enabled building management platforms and a mature installation network experienced with next-generation glazing.

Key companies in the Thermochromic Materials for Smart Windows Market include ChromoGenics AB, Guardian Glass LLC, View Inc., PPG Industries Inc., Kinestral Technologies, Saint-Gobain S.A., AGC Inc., Nippon Sheet Glass Co. Ltd., Gentex Corporation, and Halio Inc. Companies competing in the Thermochromic Materials for Smart Windows Market focus on several strategic pillars to reinforce their market standing. Many emphasize sustained R&D investment to enhance transition temperatures, material durability, and optical clarity, ensuring greater compatibility with modern building requirements. Firms increasingly streamline production technologies to reduce manufacturing costs and support large-scale deployment. Strategic partnerships with glazing manufacturers and smart-building solution providers help expand access to commercial projects.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Material type

2.2.3 Product form

2.2.4 Technology & control

2.2.5 Manufacturing process

2.2.6 End use industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product form

3.8 Future market trends

3.9 Patent Landscape

3.10 Trade statistics (Note: the trade statistics will be provided for key countries only)

3.10.1 Major importing countries

3.10.2 Major exporting countries

3.11 Sustainability and Environmental Aspects

3.11.1 Sustainable Practices

3.11.2 Waste Reduction Strategies

3.11.3 Energy Efficiency in Production

3.11.4 Eco-friendly Initiatives

3.12 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Million) (Tons)

5.1 Key trends

5.2 Vanadium dioxide (vo2) systems

5.2.1 Pure vo2 systems

5.2.2 Tungsten-doped vo2

5.2.3 Molybdenum-doped vo2

5.2.4 Co-doped vo2 systems

5.2.5 Core-shell vo2 nanostructures

5.3 Hydrogel-based systems

5.3.1 PNIPAM hydrogels

5.3.2 HPC (hydroxypropyl cellulose) systems

5.3.3 Composite hydrogels

5.3.4 Physically cross-linked systems

5.3.5 Chemically cross-linked systems

5.4 Perovskite materials

5.4.1 Halide perovskites

5.4.2 Methylamine-switchable systems

5.4.3 Hydration-responsive materials

5.5 Liquid crystal systems

5.5.1 Thermotropic liquid crystals

5.5.2 Cholesteric liquid crystals

5.5.3 Lc-polymer composites

5.6 Organic dye systems

5.6.1 LEUCO dyes

5.6.2 SPIROPYRAN systems

5.6.3 LETC (ligand exchange thermochromism) systems

Chapter 6 Market Estimates and Forecast, By Product Form, 2021 - 2034 (USD Million) (Tons)