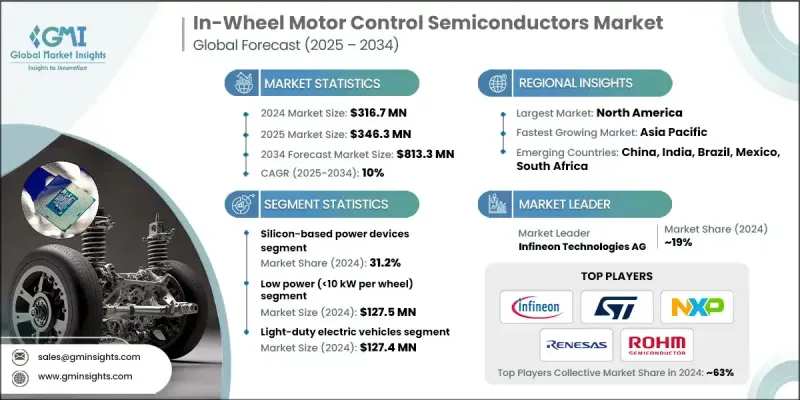

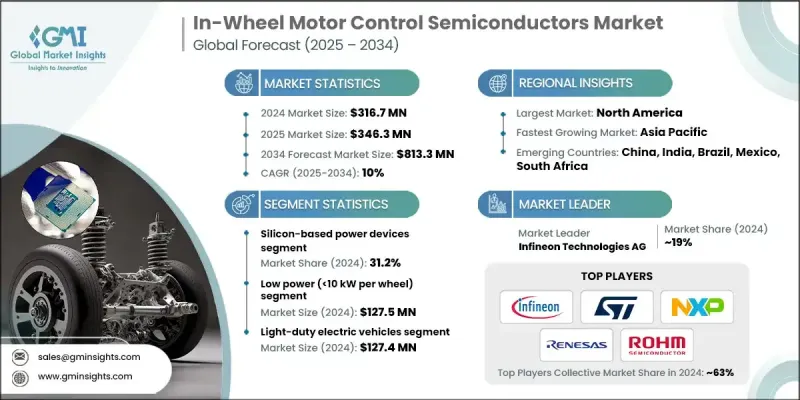

세계 휠 내장형 모터 제어용 반도체 시장은 2024년 3억 1,670만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10%로 성장하여 8억 1,330만 달러에 이를 것으로 예측됩니다.

전동 이동성으로의 전환이 진행되고 효율적이고 경량이고 컴팩트한 구동계 시스템에 대한 수요가 높아지고 있는 것이 본 시장의 확대를 견인하는 주요 요인입니다. 이러한 반도체는 전기자동차 내의 전력 분배를 제어·최적화하고, 토크 제어의 향상, 에너지 효율의 향상, 차량 성능의 강화를 실현하는데 있어서 필수적인 부품입니다. 지속가능한 교통수단과 에너지 효율적인 차량에 대한 관심 증가와 더불어, 파워 일렉트로닉스의 급속한 기술 혁신이 결합되어 시장 채용이 가속화되고 있습니다. 실리콘 카바이드(SiC)나 질화갈륨(GaN)과 같은 와이드 밴드갭 반도체 재료의 통합이 진행됨으로써 에너지 손실의 저감과 열 관리의 개선이 도모되어, 인휠 모터 시스템의 성능은 더욱 진화하고 있습니다. 전기자동차 업계의 강력한 추진력, 고성능 차량에 대한 소비자 기대의 진화, 모터 제어 기술의 지속적인 진보가 휠 내장형 모터 제어용 반도체 시장의 세계 전망을 형성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 3억 1,670만 달러 |

| 예측 금액 | 8억 1,330만 달러 |

| CAGR | 10% |

실리콘 기반 파워 기기 부문은 2024년 31.2%의 점유율을 차지했습니다. 이러한 장치는 비용 효율성, 입증된 신뢰성 및 확립된 생산 인프라를 통해 가장 널리 채택되고 있습니다. 실리콘 기반 반도체는 안정적인 성능, 통합의 용이성, 시장에서의 광범위한 가용성을 통해 자동차 제조업체들에게 선호되고 있으며, SiC 및 GaN과 같은 더 비싼 신흥 재료에 비해 신뢰할 수 있는 옵션이 되었습니다.

저전력(1륜당 10kW) 부문은 2024년에 1억 2,750만 달러 시장 규모를 창출했습니다. 이 카테고리가 주류가 되는 이유는 소형 전동 이동성 용도에 적합하기 때문입니다. 저전력 인휠 모터 제어 시스템은 컴팩트하고 가벼운 차량에 이상적이며 효율적인 에너지 공급, 발열량 감소, 저렴한 설계를 실현합니다. 공유 EV 및 소형 전동 모델을 포함한 도시형 이동성에 대한 적응성으로 인해 보급이 계속 추진되고 있습니다.

북미 휠 내장형 모터 제어용 반도체 시장은 2024년 28.5%의 점유율을 차지했습니다. 이 지역은 강력한 자동차 제조 능력, 조사 혁신, 전기 이동성 및 자율주행 차량 기술에 대한 투자 증가의 혜택을 누리고 있습니다. 경차 및 대형 차량의 두 범주에서 전기자동차 추진 시스템을 위한 첨단 반도체 솔루션에 대한 수요가 지속적으로 지역 시장의 성장을 지원하고 있습니다.

유럽의 휠 내장형 모터 제어용 반도체 시장은 2024년 6,790만 달러 규모를 창출했습니다. 이 지역은 전기자동차 도입의 주도적 입장 외에도 엄격한 배출 가스 규제와 첨단 자동차 엔지니어링 기술을 가지고 있어 컴팩트하고 효율적인 모터 제어 솔루션 수요를 견인하고 있습니다. 유럽의 주요 자동차 제조업체가 차세대 전기 구동 시스템에 대한 지속적인 투자가 시장의 추가 확대를 추진하고 있습니다.

세계의 휠 내장형 모터 제어용 반도체 시장에서 주요 진출기업으로는 Infineon Technologies AG, NXP Semiconductors NV, STMicroelectronics NV, Texas Instruments Incorporated, ON Semiconductor Corporation, Renesas Electronics Corporation, ROHM Semiconductor Co., Ltd., Mitsubishi A. Inc., Alegro MicroSystems, Inc., Melexis NV, Maxim Integrated Inc., Toshiba Corporation, Fuji Electric Co., Ltd., Continental AG, Robert Bosch GmbH, Valeo SA, Magna International Inc., BorgWarner Inc 등이 있습니다. 휠 내장형 모터 제어용 반도체 시장의 주요 기업은 시장에서의 지위를 강화하기 위해 혁신, 전략적 제휴, 기술적 확대에 주력하고 있습니다. 많은 기업들이 반도체의 효율성, 열 관리, 전력 밀도 향상을 도모하기 위해 연구 개발에 많은 투자를 하고 있습니다.

The Global In-Wheel Motor Control Semiconductors Market was valued at USD 316.7 million in 2024 and is estimated to grow at a CAGR of 10% to reach USD 813.3 million by 2034.

The growing transition toward electric mobility and the demand for efficient, lightweight, and compact drivetrain systems are key drivers behind this market's expansion. These semiconductors are essential components in controlling and optimizing power distribution within electric vehicles, ensuring better torque control, higher energy efficiency, and enhanced vehicle performance. The rising focus on sustainable transportation and energy-efficient vehicles, coupled with rapid innovation in power electronics, continues to accelerate market adoption. Increasing integration of wide-bandgap semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN) is further transforming the performance of in-wheel motor systems by reducing energy loss and improving heat management. The strong push from the electric vehicle industry, evolving consumer expectations for high-performance vehicles, and the ongoing advancements in motor control technology are shaping the global outlook for the in-wheel motor control semiconductors market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $316.7 Million |

| Forecast Value | $813.3 Million |

| CAGR | 10% |

The silicon-based power devices segment held a 31.2% share in 2024. These devices remain the most widely adopted due to their cost-effectiveness, proven dependability, and established production infrastructure. Silicon-based semiconductors are preferred by automakers for their stable performance, ease of integration, and broad market availability, making them a reliable option compared with more expensive emerging materials like SiC and GaN.

The low-power (10 kW per wheel) segment generated USD 127.5 million in 2024. This category dominates because of its suitability for smaller electric mobility applications. Low-power in-wheel motor control systems are ideal for compact and light-duty vehicles, offering efficient energy delivery, reduced heat generation, and affordable design. Their adaptability for urban mobility, including shared EVs and small electric models, continues to promote widespread deployment.

North America In-Wheel Motor Control Semiconductors Market held 28.5% share in 2024. The region benefits from strong automotive manufacturing capabilities, research innovation, and increasing investments in electric mobility and autonomous vehicle technologies. The demand for advanced semiconductor solutions in electric vehicle propulsion systems across both light-duty and heavy-duty categories continues to support regional market growth.

Europe In-Wheel Motor Control Semiconductors Market generated USD 67.9 million in 2024. The region's leadership in electric vehicle adoption, coupled with stringent emission standards and high automotive engineering expertise, is driving demand for compact and efficient motor control solutions. Continuous investment from leading European automakers in next-generation electric drivetrain systems is propelling further expansion of the market.

Key participants operating in the Global In-Wheel Motor Control Semiconductors Market include Infineon Technologies AG, NXP Semiconductors N.V., STMicroelectronics N.V., Texas Instruments Incorporated, ON Semiconductor Corporation, Renesas Electronics Corporation, ROHM Semiconductor Co., Ltd., Mitsubishi Electric Corporation, Wolfspeed, Inc., Analog Devices, Inc., Allegro MicroSystems, Inc., Melexis NV, Maxim Integrated Inc., Toshiba Corporation, Fuji Electric Co., Ltd., Continental AG, Robert Bosch GmbH, Valeo SA, Magna International Inc., and BorgWarner Inc. Leading companies in the In-Wheel Motor Control Semiconductors Market are focusing on innovation, strategic alliances, and technological expansion to strengthen their market position. Many are investing heavily in research and development to advance semiconductor efficiency, thermal management, and power density.