자동차 디지털 공장 자동화 시장 기회, 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)

Automotive Digital Factory Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1876548

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

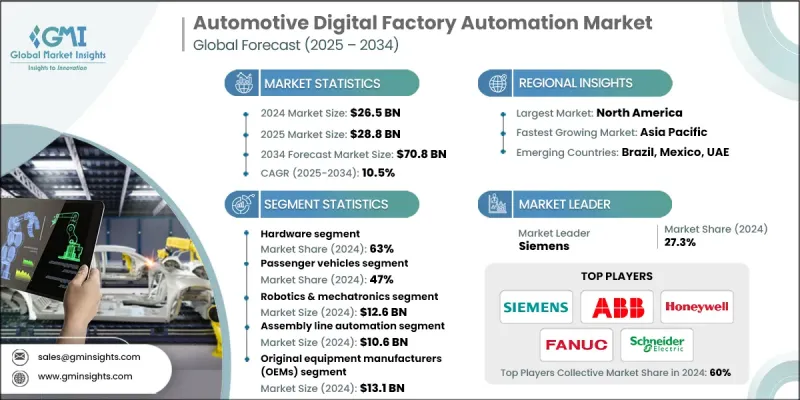

세계의 자동차 디지털 공장 자동화 시장은 2024년에 265억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 10.5%를 나타내 708억 달러에 달할 것으로 예측되고 있습니다.

자동차 업계가 스마트 제조와 디지털 전환을 적극적으로 도입하면서 시장은 강한 성장세를 보이고 있습니다. 제조업체 각사는 급속하게 변화하는 환경하에서 경쟁력을 유지하기 위해, 업무 효율화, 실시간 데이터 분석, 유연한 생산 시스템의 구축을 우선 과제로 하고 있습니다. 인더스트리 4.0 기술, 인공지능, IoT 대응 감시 플랫폼의 통합으로 기존의 자동차 시설은 지능적이고 데이터 구동형 생산 환경으로 변모하고 있습니다. 이러한 디지털 공장 시스템은 예측 유지 보수와 자동화된 프로세스 제어를 통해 생산성 최적화, 장비 가동 중지 시간 절감 및 품질 보증 강화를 실현합니다. 디지털 트윈 시뮬레이션, 로보틱스, AI 기반 분석 및 IoT 연결성을 결합하여 기업은 생산주기 전반에 걸쳐 완벽한 협력을 실현하고 있습니다. 이 융합은 지속가능성 목표와 에너지 효율을 지원할 뿐만 아니라 전체 라이프사이클의 시각화, 컴플라이언스 향상, 제조 탄력성 향상을 가능하게 합니다. 상호 연결성, 적응성 및 투명성을 갖춘 제조 네트워크에 대한 수요 증가는 세계 OEM 제조업체와 공급업체 모두에서 디지털 공장 자동화에 대한 지속적인 투자를 추진하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 가치

265억 달러

예측 금액

708억 달러

CAGR

10.5%

하드웨어 부문은 2024년에 시장의 약 63%를 차지했고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 10.8%를 나타낼 것으로 예측됩니다. 하드웨어는 자동차 디지털 공장 자동화의 기반이며 생산 라인 전체에서 실시간 추적, 데이터 수집 및 기계 제어를 실현하는 데 중요한 역할을 합니다. 주요 하드웨어 요소에는 원활한 운영, 예보 유지, 높은 생산성을 보장하는 IoT 센서, PLC, RFID 시스템, 임베디드 컨트롤러, 머신 비전 장치 등이 포함됩니다. 자동차 제조업체와 공급업체는 이러한 시스템에 따라 정밀도를 유지하고, 오류를 줄이고, 생산 성능을 최적화하는 동시에 시설 전반에서 확장 가능한 디지털 변환을 실현합니다.

승용차 부문은 2024년에 47%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 11.3%를 나타낼 것으로 예측됩니다. 전기자동차 및 하이브리드차에 대한 수요 증가와 보다 엄격한 환경규제가 함께 승용차 생산에 있어서 자동화 투자가 가속화되고 있습니다. 자동차 제조업체는 로봇 공학, 클라우드 통합 플랫폼, AI를 활용한 분석 등의 디지털 팩토리 솔루션을 활용하여 공정 정확도 향상, 컴플라이언스 확보, 생산 효율 향상을 도모하고 있습니다. 이러한 기술은 생산 지표에 대한 실시간 가시성을 제공하여 다운타임을 최소화하면서 복잡하고 대량의 조립 작업을 관리할 수 있는 능력을 강화합니다.

2024년 기준 미국의 자동차 디지털 공장 자동화 시장은 88%의 점유율을 차지하며 85억 달러 규모에 이르렀습니다. 일본의 견고한 제조거점과 디지털 기술 및 AI 기술의 급속한 도입이 결합되어 자동차 공장의 대규모 현대화를 추진하고 있습니다. 첨단 로보틱스, IoT 지원 모니터링, 디지털 트윈 기술이 생산 및 공급망 시스템에 점점 통합되고 있습니다. 이 확장은 자원의 더 나은 활용, 폐기물 감소, 제품 품질 향상을 지원하는 동시에 업계의 지속가능성과 혁신 목표를 강화합니다.

세계 자동차 디지털 공장 자동화 시장의 주요 기업으로는 Mitsubishi Electric, Schneider Electric, FANUC, Siemens, ABB, Emerson Electric, Honeywell International, JR Automation Technologies, Rockwell Automation, Yokogawa Electric 등이 있습니다. 세계 자동차 디지털 공장 자동화 시장의 주요 기업은 시장의 존재감을 강화하기 위해 기술 혁신, 전략적 제휴, 세계 전개에 주력하고 있습니다. 정밀성 향상과 제조 공정의 효율화를 도모하기 위해 첨단 로보틱스, 디지털 트윈 기술, AI 구동형 분석 기술에 많은 투자를 하고 있습니다. 자동화 제공업체와 자동차 OEM 제조업체 간의 협력을 통해 맞춤형 엔드 투 엔드 자동화 에코시스템을 구축할 수 있습니다. 또한 에너지 효율적인 하드웨어 통합과 스마트 모니터링 시스템을 통한 자원 활용 최적화를 통해 지속가능성에 중점을 둡니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

노동력 부족 대책의 요건

품질과 일관성 향상에 대한 요청

생산 유연성과 맞춤형 요구

비용 절감과 업무 효율화의 압력

업계의 잠재적 위험 및 과제

초기 자본 투자 요건의 높이

레거시 시스템 통합의 과제

시장 기회

공장에서의 5G 네트워크 도입

엣지 컴퓨팅 및 실시간 분석

공급망의 추적성을 위한 블록체인

AI를 활용한 예측 유지보수 확대

성장 가능성 분석

규제 상황

안전과 품질 기준

환경 및 지속가능성에 관한 규제

데이터 프라이버시와 사이버 보안

업계 고유 기준

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

제조업의 5G 네트워크 통합

엣지 컴퓨팅 및 실시간 분석

공급망 투명화를 위한 블록체인

증강현실(AR) 및 가상현실(VR)의 응용

산업 시스템에서 사이버 보안의 진화

휴먼 머신 인터페이스의 진보

디지털 트윈의 진화와 메타버스 통합

자율형 공장의 개념

가격 동향

지역별

제품별

생산 통계

생산 거점

소비 거점

수출입

코스트 내역 분석

특허 분석

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

위험 평가 프레임워크

사이버 보안 리스크 관리

업무 리스크 평가

재무위험분석

공급망 위험 완화

최상의 시나리오

미래 전망과 전략적 제안

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

인수 및 합병

파트너십 및 협력

신제품 발매

사업 확장 계획과 자금 조달

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

주요 동향

하드웨어

산업용 로봇

제어 시스템

센서 및 비전 시스템

휴먼 머신 인터페이스(HMI)

기타

소프트웨어

제조 실행 시스템(MES)

디지털 트윈 및 시뮬레이션 소프트웨어

예측 유지보수 및 분석 플랫폼

AI 및 머신러닝 플랫폼

ERP/클라우드 통합

서비스

설치 및 시운전

유지보수 및 지원

컨설팅 및 시스템 통합

개조 및 현대화 서비스

교육 및 인력 개발

제6장 시장 추계·예측 : 차량별(2021-2034년)

주요 동향

승용차

해치백

세단

SUV

상용차

소형 상용차(LCV)

중형 상용차(MCV)

대형 상용차(HCV)

이륜차

제7장 시장 추계·예측 : 기술별(2021-2034년)

주요 동향

로봇공학 및 메카트로닉스

산업용 IoT 및 센서

인공지능(AI) 및 머신러닝

디지털 트윈 및 시뮬레이션

클라우드 및 엣지 컴퓨팅

제8장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

조립 라인 자동화

용접 및 접합 작업

도장 및 코팅 공정

품질관리 및 검사

자재 취급 및 물류

제9장 시장 추계·예측 : 최종 용도별(2021-2034년)

주요 동향

OEM

Tier 1 공급업체

Tier 2 공급업체

애프터마켓

제10장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

싱가포르

한국

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

아랍에미리트(UAE)

남아프리카

사우디아라비아

제11장 기업 프로파일

Global Player

ABB

Bosch Rexroth

Emerson Electric

FANUC

General Electric

Honeywell International

Rockwell Automation

Schneider Electric

Siemens

Regional Player

Festo

JR Automation Technologies

Keyence

KUKA

Mitsubishi Electric

Omron

UL Solutions

Vention

Yokogawa Electric

신흥기업

Augury Systems

Bright Machines

MachineMetrics

Path Robotics

Sight Machine

Standard Bots

Tulip Interfaces

KTH

영문 목차

영문목차

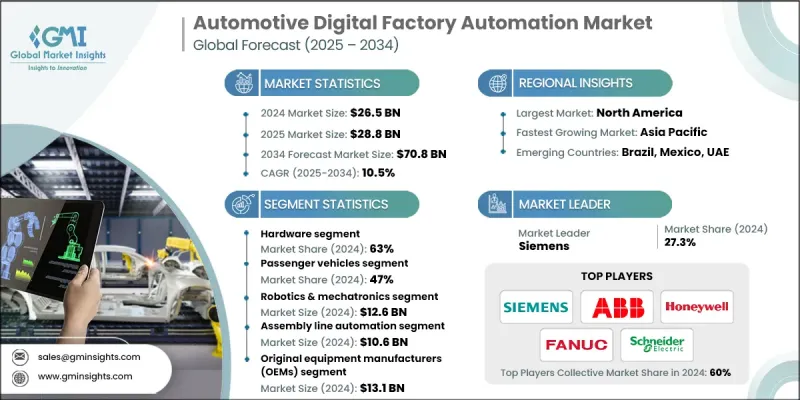

The Global Automotive Digital Factory Automation Market was valued at USD 26.5 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 70.8 billion by 2034.

The market is experiencing strong momentum as the automotive industry increasingly embraces smart manufacturing and digital transformation. Manufacturers are prioritizing operational efficiency, real-time data insights, and flexible production systems to stay competitive in a rapidly evolving landscape. The integration of Industry 4.0 technologies, artificial intelligence, and IoT-enabled monitoring platforms is transforming traditional automotive facilities into intelligent, data-driven production environments. These digital factory systems optimize productivity, reduce equipment downtime, and enhance quality assurance through predictive maintenance and automated process control. By combining digital twin simulations, robotics, AI-based analytics, and IoT connectivity, companies are achieving seamless coordination across the entire production cycle. This convergence not only supports sustainability goals and energy efficiency but also enables full lifecycle visibility, improved compliance, and greater manufacturing resilience. The growing need for interconnected, adaptive, and transparent manufacturing networks is driving continued investment in digital factory automation across both OEMs and suppliers worldwide.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$26.5 Billion

Forecast Value

$70.8 Billion

CAGR

10.5%

The hardware segment accounted for about 63% of the market in 2024 and is anticipated to expand at a CAGR of 10.8% from 2025 to 2034. Hardware remains the foundation of automotive digital factory automation, playing a critical role in enabling real-time tracking, data collection, and machine control throughout production lines. Key hardware elements include IoT sensors, PLCs, RFID systems, embedded controllers, and machine vision devices that ensure seamless operation, predictive maintenance, and high productivity. Automakers and suppliers depend on these systems to maintain precision, reduce errors, and optimize production performance while enabling scalable digital transformation across facilities.

The passenger vehicle segment held 47% share in 2024 and is expected to grow at a CAGR of 11.3% between 2025 and 2034. Rising demand for electric and hybrid vehicles, coupled with stricter environmental regulations, is accelerating automation investments in passenger vehicle production. Automotive manufacturers are leveraging digital factory solutions such as robotics, cloud-integrated platforms, and AI-powered analytics to improve process accuracy, ensure compliance, and increase output efficiency. These technologies provide real-time visibility into production metrics and enhance the ability to manage complex, high-volume assembly operations with minimal downtime.

U.S. Automotive Digital Factory Automation Market held 88% share and generated USD 8.5 billion in 2024. The nation's strong manufacturing base, combined with rapid adoption of digital and AI technologies, is fueling large-scale modernization of automotive plants. Advanced robotics, IoT-enabled monitoring, and digital twin technologies are being increasingly integrated into production and supply chain systems. This expansion supports better resource utilization, reduced waste, and improved product quality while reinforcing the industry's sustainability and innovation goals.

Key players operating in the Global Automotive Digital Factory Automation Market include Mitsubishi Electric, Schneider Electric, FANUC, Siemens, ABB, Emerson Electric, Honeywell International, JR Automation Technologies, Rockwell Automation, and Yokogawa Electric. Leading companies in the Global Automotive Digital Factory Automation Market are focusing on technological innovation, strategic partnerships, and global expansion to strengthen their market presence. They are investing heavily in advanced robotics, digital twin technologies, and AI-driven analytics to enhance precision and streamline manufacturing processes. Collaborations between automation providers and automotive OEMs are enabling the creation of customized, end-to-end automation ecosystems. Companies are also emphasizing sustainability by integrating energy-efficient hardware and optimizing resource utilization through smart monitoring systems.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Component

2.2.3 Vehicle

2.2.4 Technology

2.2.5 Application

2.2.6 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Labor shortage mitigation requirements

3.2.1.2 Quality & consistency improvement demands

3.2.1.3 Production flexibility & customization needs