POC(Point of Care) 검사 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)

Point of Care Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871303

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 163 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

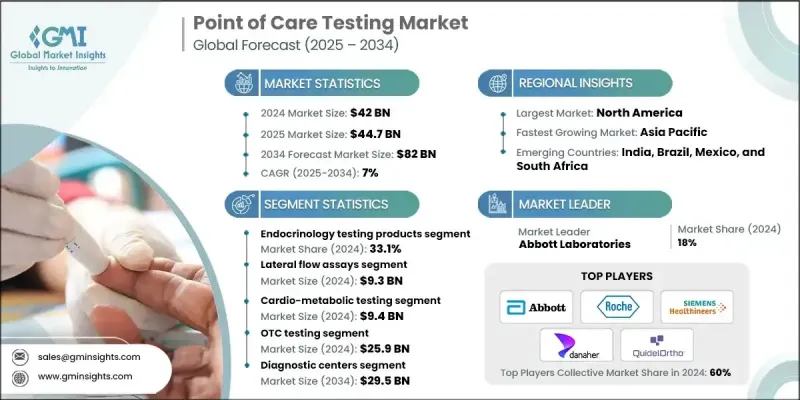

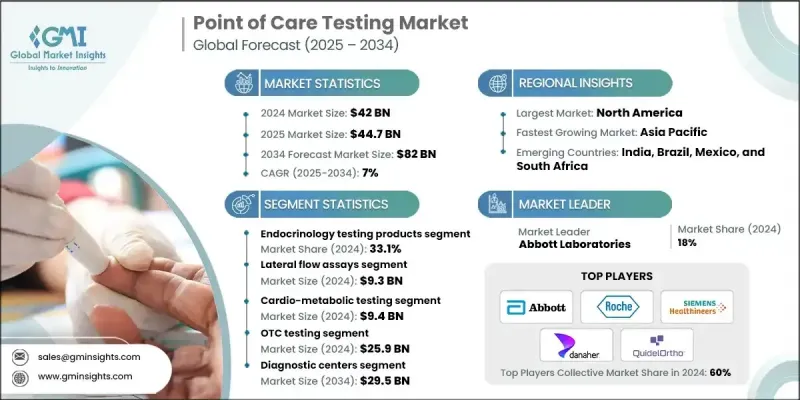

세계 POC(Point of Care) 검사 시장은 2024년에 420억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 7%로 성장하여 820억 달러에 이를 것으로 예측됩니다.

시장 확대의 배경으로는 개발도상국에서의 질병유병률 증가, 선진검사기술을 갖춘 진단검사실 증가, 연구개발에 많은 투자가 포함됩니다. 응급 의료 및 원격지에서 신속하고 정확한 진단 수요가 증가함에 따라 정부 및 의료 기관은 혁신적인 POC 검사 솔루션의 도입을 추진하고 있습니다. POC(Point of Care) 검사는 임상의가 환자가 있는 곳에서 직접 검사실 수준의 정확도를 정확하게 얻는 결과를 제공하므로 신속한 의료 판단을 가능하게 하고 중앙 검사실에 대한 의존도를 줄일 수 있습니다. 이 장치는 마이크로플루이딕스 플랫폼, 면역측정법, 횡류검사법과 같은 첨단 기술을 이용하여 혈액, 소변, 타액을 분석하고, 종종 몇 분 내에 결과를 제공합니다. 현대의 기기는 모바일 앱 및 전자 건강 기록과 통합되는 경우가 많으며, 지방이나 의료 서비스가 미치지 못하는 지역에서의 접근성을 향상시키고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034

시작 금액

420억 달러

예측 금액

820억 달러

CAGR

7%

내분비 검사 제품 부문은 2024년에 33.1%의 큰 점유율을 차지했습니다. 이 부문은 당뇨병과 갑상선 관련 질환과 같은 신속하고 정확한 진단이 필요한 내분비 질환의 유병률이 증가함에 따라 꾸준히 성장하고 있습니다. 바이오센서, 면역측정법 및 마이크로플루이딕스 기술의 발전으로 검사의 효율성과 정밀도가 향상되었습니다. 혈당 측정기 및 HbA1c 분석기와 같은 장비는 원격 모니터링 및 원격 의료 용도를 위해 모바일 앱과 연동되는 스마트 툴로 진화하고 있습니다.

2024년 라테랄 플로우 분석(LFA) 부문 시장 규모는 93억 달러로 평가되었습니다. LFA는 항체를 사용하여 액체 샘플에서 표적 물질을 검출하는 종이 기반 진단 장치입니다. 그것의 간편성, 신속성, 사용의 용이성에서 널리 이용됩니다. 감염증의 발생률 상승으로 의료 종사자가 환자의 신속한 스크리닝, 진단, 대응을 가능하게 하고, 치료 결정의 신속화와 치료 성과의 향상을 지원하는 LFA 수요가 가속화되고 있습니다.

미국의 POC 검사(Point of Care Testing) 시장은 2024년 125억 달러로 평가되었습니다. 이 성장은 특히 당뇨병과 같은 질병의 유병률 증가와 신속하고 기술을 활용하는 진단 솔루션의 채택 증가로 추진되고 있습니다. 미국의 의료 부문은 혁신성과 접근성에 중점을 두고 있기 때문에 POC(Point of Care) 검사 기술의 주요 시장으로 자리 잡고 있습니다.

세계 POC(Point of Care) 검사 시장의 주요 기업으로는 Meridian Bioscience, Abbott Laboratories, Bio-Rad Laboratories, LifeScan IP Holdings, LLC, Acon Laboratories, Becton, Dickinson, and Company, Danaher Corporation, BioMerieux SA, Dexcom, Inc., QuidelOrtho Corporation, Dragerwerk AG & Co. KGaA, F.Hoffmann-La Roche Ltd., Medtronic Plc, Nova Biomedical, Siemens Healthineers AG, and Sysmex Corporation 등을 들 수 있습니다. POC(Point of Care) 검사 시장의 기업은 시장에서의 존재감을 강화하기 위해 여러 전략을 활용하고 있습니다. 보다 빠르고 정확하며 연결성이 높은 진단 장비를 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다. 전략적 제휴, 파트너십 및 인수를 통해 기업은 제품 포트폴리오를 확대하고 새로운 지역 시장에 진출할 수 있습니다. 많은 기업들이 기술 혁신에 주력하고 AI, 연결성, 디지털 헬스 플랫폼을 기기에 통합함으로써 데이터 관리와 원격 의료의 능력 향상을 도모하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

개발도상국의 질병유병률 상승 동향

고도의 진단 기기를 갖춘 병리 검사실 및 서비스의 급증

POC(Point of Care) 검사에 있어서의 기술적 진보

R&D 투자 증가

업계의 잠재적 위험 및 과제

엄격한 규제 프레임워크

높은 제품 개발 비용

시장 기회

원격지 및 농촌지역에서 수요 증가

디지털 헬스 플랫폼과의 통합

성장 가능성 분석

규제 상황

북미

아시아태평양

유럽

기술 상황

장래 시장 동향

갭 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략 대시보드

주요 발전

인수합병

제휴 및 협력 관계

신제품 발매

확대 계획

제5장 시장 추정 및 예측 : 제품별, 2021-2034

주요 동향

내분비 검사 제품

혈당 모니터링

스트립

측정기

란셋

콜레스테롤 검사 제품

임신 검사 제품

불임 검사 제품

갑상선 기능 검사

심대사 검사 제품

심장 마커 검사 제품

hsTnI(고감도 트로포닌 I)

BNP(B형 나트륨 이뇨 펩티드)

D 다이머

CK-MB(크레아틴 키나아제-MB)

미오글로빈

기타 심장 마커 검사

혈액가스(폐기능)

대사물 검사 제품

전해질 검사

간 기능

빌리루빈

알라닌 트랜스아미나제(ALT)

신장 기능

크레아티닌

요소

요산

HBA1C 검사 제품

감염증 검사 제품

인플루엔자 검사 제품

HIV 검사 제품

C형 간염 검사 제품

성감염증(STD) 검사 제품

의료 관련 감염(HAI) 검사 제품

호흡기 감염증 검사 제품

열대병 검사 제품

기타 감염증 검사 제품

응고 검사 제품

PT/INR 검사 제품

활성화 응고 시간(ACT/APTT) 검사 제품

종양/암 마커 검사 제품

소변 검사 제품

혈액 검사 제품

약물 남용 검사 제품

변잠혈 검사 제품

기타 제품

제6장 시장추정 및 예측 : 기술별, 2021-2034

주요 동향

래터럴 플로우 분석

딥 스틱

미세유체공학

분자진단

면역 측정법

응집법

유통식

고상

바이오센서

전기화학식

광학

열

질량 감응형

기타 바이오 센서

제7장 시장 추정 및 예측 : 용도별, 2021-2034

주요 동향

심장 대사 검사

감염증 검사

신장병 검사

약물 남용 검사(DoA)

혈당 검사

임신 검사

암 바이오마커 검사

기타 용도

제8장 시장 추정 및 예측 : 처방전별, 2021-2034

주요 동향

일반의약품 검사

처방전에 기초한 검사

제9장 시장 추정 및 예측 : 최종 용도별, 2021-2034

주요 동향

병원

진단센터

연구기관

재택치료 환경

기타 최종 용도

제10장 시장추정 및 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

Abbott Laboratories

Acon Laboratories

Becton, Dickinson, and Company

BioMerieux SA

Bio-Rad Laboratories, Inc.

Danaher Corporation

Dexcom, Inc

Dragerwerk AG & Co. KGaA

F. Hoffmann-La Roche Ltd.

LifeScan IP Holdings, LLC

Medtronic Plc

Meridian Bioscience, Inc.

Nova Biomedical

QuidelOrtho Corporation

Siemens Healthineers AG

Sysmex Corporation

SHW

영문 목차

영문목차

The Global Point of Care Testing Market was valued at USD 42 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 82 billion by 2034.

The market's expansion is driven by increasing disease prevalence in developing nations, the growing number of diagnostic laboratories equipped with advanced testing technologies, and significant investments in research and development. Rising demand for rapid, accurate diagnostics in emergency care and remote locations is pushing governments and healthcare organizations to adopt innovative POC testing solutions. Point-of-care testing enables clinicians to obtain fast, lab-grade results directly at the patient's location, facilitating quick medical decisions and reducing dependence on central labs. Devices use advanced technologies such as microfluidic platforms, immunoassays, and lateral flow assays to analyze blood, urine, or saliva, often providing results within minutes. Modern devices often integrate with mobile apps or electronic health records, improving accessibility in rural and underserved areas.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$42 Billion

Forecast Value

$82 Billion

CAGR

7%

The endocrinology testing products segment held a substantial share of 33.1% in 2024. This segment is growing steadily due to the increasing prevalence of endocrine disorders, including diabetes and thyroid-related conditions, which demand rapid and accurate diagnostics. Advances in biosensors, immunoassays, and microfluidic technology have improved test efficiency and accuracy. Devices like glucose meters and HbA1c analyzers are evolving into smart tools connected to mobile apps for remote monitoring and telehealth applications.

The lateral flow assays segment was valued at USD 9.3 billion in 2024. LFAs are paper-based diagnostic devices that detect target substances in liquid samples using antibodies. They are widely used due to their simplicity, speed, and ease of use. Rising incidences of infectious diseases have accelerated the demand for LFAs, which allow healthcare providers to quickly screen, diagnose, and respond to patients, supporting faster treatment decisions and better outcomes.

U.S. Point of Care Testing Market was valued at USD 12.5 billion in 2024. Growth is being driven by increasing disease prevalence, particularly diabetes, and the rising adoption of fast, technology-enabled diagnostic solutions. The U.S. healthcare sector's focus on innovation and accessibility has positioned it as a leading market for point-of-care testing technologies.

Key players in the Global Point of Care Testing Market include Meridian Bioscience, Abbott Laboratories, Bio-Rad Laboratories, LifeScan IP Holdings, LLC, Acon Laboratories, Becton, Dickinson, and Company, Danaher Corporation, BioMerieux SA, Dexcom, Inc., QuidelOrtho Corporation, Dragerwerk AG & Co. KGaA, F. Hoffmann-La Roche Ltd., Medtronic Plc, Nova Biomedical, Siemens Healthineers AG, and Sysmex Corporation. Companies in the Point of Care Testing Market are leveraging multiple strategies to strengthen their market presence. They are heavily investing in R&D to develop faster, more accurate, and connected diagnostic devices. Strategic collaborations, partnerships, and acquisitions allow firms to expand product portfolios and enter new regional markets. Many are focusing on technological innovation, integrating AI, connectivity, and digital health platforms into devices to improve data management and telemedicine capabilities.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Products trends

2.2.3 Technology trends

2.2.4 Prescription trends

2.2.5 Application trends

2.2.6 End use trends

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Upward trend in disease prevalence among developing countries

3.2.1.2 Surging number of pathology labs and services equipped with advanced diagnostic equipment

3.2.1.3 Technological advancements in point of care tests

3.2.1.4 Increasing research and development investment

3.2.2 Industry pitfalls and challenges

3.2.2.1 Stringent regulatory framework

3.2.2.2 High cost of product development

3.2.3 Market opportunities

3.2.3.1 Growing demand in remote and rural areas

3.2.3.2 Integration with digital health platforms

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Asia Pacific

3.4.3 Europe

3.5 Technology landscape

3.6 Future market trends

3.7 Gap analysis

3.8 Porter's analysis

3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Strategy dashboard

4.7 Key developments

4.7.1 Mergers and acquisitions

4.7.2 Partnerships and collaborations

4.7.3 New product launches

4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Bn)