농업기계 유지보수 서비스 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Agricultural Machinery Maintenance Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871166

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 250 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

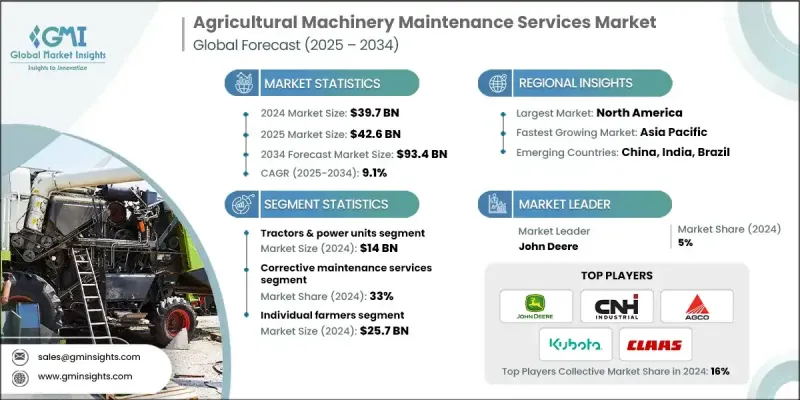

세계의 농업기계 유지보수 서비스 시장은 2024년 397억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 9.1%를 나타낼 것으로 예측되며 934억 달러에 달할 전망입니다.

노동 집약적인 농업 활동에서 기계화가 점점 더 필수화되면서 해당 산업은 급속히 확장되고 있습니다. 농민들은 생산성 향상을 위해 기계에 크게 의존하고 있어 정기적인 유지보수는 현대 농업 운영의 핵심 요소로 자리잡았습니다. 이 부문는 예측 및 예방적 유지보수 모델로 전환 중이며, 스마트 센서, 디지털 모니터링, 원격 제어 시스템이 고장 발생 전에 잠재적 장비 문제를 식별하도록 돕고 있습니다. 이러한 사전 대응적 접근은 농사 성수기 동안 비용이 많이 드는 가동 중단 시간을 최소화하고 전반적인 운영 효율성을 향상시킵니다. 개발도상 지역에서 농기계 사용이 증가함에 따라 유지보수 서비스 제공업체에게 새로운 기회가 열리고 있습니다. 농민들이 수동 노동을 트랙터, 수확기, 관개 시스템으로 대체함에 따라 디지털 플랫폼은 수리 일정 관리, 예비 부품 조달, 원격 기술 지원을 용이하게 합니다. 그러나 농촌 지역에서는 여전히 어려움이 존재합니다. 소규모 농가들은 종종 첨단 유지보수 도구를 구입할 자원이 부족하며 숙련된 기술자를 찾는 것도 쉽지 않습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

397억 달러

예측 금액

934억 달러

CAGR

9.1%

트랙터 및 동력 장치 부문은 2024년 140억 달러를 창출했습니다. 이 기계들은 여전히 농업 운영의 핵심이며, 정밀 농업 기술의 도입으로 그 복잡성과 중요성이 더욱 증가했습니다.

북미의 농업 기계 유지 보수 서비스 시장은 2024년에 77%의 점유율을 차지하고 121억 달러 규모를 기록했습니다. 북미의 우위는 선진화된 기계화, 견고한 서비스 인프라, 정밀농업의 광범위한 도입에 기인합니다. 해당 지역 농업기계 유지보수 시장은 지속적인 장비 업그레이드와 미국-캐나다 간 강력한 무역 관계의 혜택을 받고 있습니다.

세계의 농업 기계 유지 보수 서비스 시장의 주요 기업으로는 CLAAS 그룹, 존 디어, CNH 인더스트리얼 N.V., SDF 그룹, 쿠보타 코퍼레이션, 마힌드라 앤 마힌드라, 오토노머스 트랙터 코퍼레이션, 얀마 홀딩스, JCB, 프레시전 플랜팅, 팜와이즈, 에스코츠 쿠보타 리미티드, 스타라, 아이언 옥스가 있습니다. 기업들은 IoT, 센서, 원격 모니터링을 통합하여 예방 및 예측 유지보수 솔루션을 강조함으로써 장비 가동 중단 시간을 줄이고 있습니다. 농촌 및 신흥 시장에서 서비스 네트워크를 확장함으로써 신규 고객 기반 확보와 접근성 향상에 기여하고 있습니다. 기업들은 기술자 역량 강화를 위한 교육 프로그램에 투자하여 고품질 유지보수 지원을 보장하고 있습니다. 기계 제조사 및 유통업체와의 전략적 파트너십을 통해 묶음 서비스 제공이 가능해져 고객 충성도를 강화하고 있습니다. 수리 예약, 예비 부품 주문, 원격 진단을 위한 디지털 플랫폼은 운영 효율성과 고객 경험을 개선합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

업계에 미치는 영향요인

성장 촉진요인

개인화 및 큐레이션의 매력

전자상거래 및 소비자 직거래 모델의 성장

기업을 위한 반복 수익 모델

업계의 잠재적 억제요인 및 과제

높은 고객 이탈률

물류 및 주문 처리 복잡성

기회

지속가능성에 초점을 맞춘 포장 및 제품

틈새 시장으로의 확장

성장 가능성 분석

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

규제 상황

규격 및 규정 준수 요건

지역별 규제 프레임워크

인증기준

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추계 및 예측 : 기기 유형별(2021-2034년)

주요 동향

트랙터 및 동력 장치

수확기

경운 및 토양 준비 장비

식재 및 파종 장비

관개 시스템

살포 및 적용 장비

제6장 시장 추계 및 예측 : 소유 형태별(2021-2034년)

주요 동향

개인 농가

기업 농장

제7장 시장 추계 및 예측 : 사업 규모별(2021-2034년)

주요 동향

소규모 경영

중규모 농장

대규모 농장

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

작물

축산

제9장 시장 추계 및 예측 : 서비스별(2021-2034년)

주요 동향

예방적 유지보수 서비스

수정적 유지보수 서비스

예측적 유지보수 서비스

상태 모니터링 유지보수 서비스

긴급 유지보수 서비스

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

John Deere

CNH Industrial NV

AGCO Corporation

Kubota Corporation

CLAAS Group

Mahindra & Mahindra

Escorts Kubota Limited

SDF Group

JCB

Yanmar Holdings

Stara

Autonomous Tractor Corporation

FarmWise

Iron Ox

Precision Planting

HBR

영문 목차

영문목차

The Global Agricultural Machinery Maintenance Services Market was valued at USD 39.7 Billion in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 93.4 Billion by 2034.

The industry is expanding rapidly as mechanization becomes increasingly essential in labor-intensive agricultural activities. Farmers are heavily relying on machinery to boost productivity, making regular maintenance a critical part of modern farming operations. The sector is shifting toward predictive and preventive maintenance models, with smart sensors, digital monitoring, and remote-control systems helping farmers identify potential equipment issues before failures occur. This proactive approach minimizes costly downtime during peak farming periods and enhances overall operational efficiency. The growing use of farm machinery in developing regions has opened new opportunities for maintenance service providers. As farmers replace manual labor with tractors, harvesters, and irrigation systems, digital platforms facilitate repair scheduling, spare part procurement, and remote technical support. However, challenges persist in rural areas, where smallholders often lack resources for advanced maintenance tools, and finding skilled technicians can be difficult.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$39.7 Billion

Forecast Value

$93.4 billion

CAGR

9.1%

The tractors and power units segment generated USD 14 Billion in 2024. These machines remain central to agricultural operations, and the adoption of precision agriculture technology has further increased their complexity and importance.

The corrective maintenance services segment held a 33% share in 2024, holding the largest share due to the critical need for repair services during equipment failures. Despite the shift toward preventive solutions, corrective maintenance remains essential, especially during peak agricultural seasons.

North America Agricultural Machinery Maintenance Services Market held 77% share and generated USD 12.1 Billion in 2024. North America's dominance is driven by advanced mechanization, robust service infrastructure, and widespread adoption of precision agriculture. The region's agricultural machinery maintenance market benefits from continuous equipment upgrades and strong trade relations between the United States and Canada.

Key players in the Global Agricultural Machinery Maintenance Services Market include CLAAS Group, John Deere, CNH Industrial N.V., SDF Group, Kubota Corporation, Mahindra & Mahindra, Autonomous Tractor Corporation, Yanmar Holdings, JCB, Precision Planting, FarmWise, Escorts Kubota Limited, Stara, and Iron Ox. Firms are emphasizing preventive and predictive maintenance solutions by integrating IoT, sensors, and remote monitoring to reduce equipment downtime. Expanding service networks in rural and emerging markets helps capture new customer bases and improve accessibility. Companies are investing in training programs to upskill technicians, ensuring high-quality maintenance support. Strategic partnerships with machinery manufacturers and distributors enable bundled service offerings that strengthen customer loyalty. Digital platforms for scheduling repairs, ordering spare parts, and remote diagnostics improve operational efficiency and customer experience.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Equipment type

2.2.3 Ownership

2.2.4 Operational size

2.2.5 Application

2.2.6 Service type

2.3 CXO perspectives: strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Personalization and curation appeal

3.2.1.2 Growth of e-commerce and direct-to-consumer models

3.2.1.3 Recurring revenue model for businesses

3.2.2 Industry pitfalls & challenges

3.2.2.1 High customer churn rates

3.2.2.2 Logistics and fulfilment complexity

3.2.3 Opportunities

3.2.3.1 Sustainability-focused packaging and products

3.2.3.2 Expansion into niche segments

3.3 Growth potential analysis

3.4 Future market trends

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Regulatory landscape

3.6.1 Standards and compliance requirements

3.6.2 Regional regulatory frameworks

3.6.3 Certification standards

3.7 Porter's analysis

3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East and Africa

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Equipment Type, 2021 - 2034 (USD Billion)

5.1 Key trends

5.2 Tractors & power units

5.3 Harvester

5.4 Tillage & soil preparation equipment

5.5 Planting & seeding equipment

5.6 Irrigation systems

5.7 Spraying & application equipment

Chapter 6 Market Estimates and Forecast, By Ownership, 2021 - 2034 (USD Billion)

6.1 Key trends

6.2 Individual farmers

6.3 Corporate farms

Chapter 7 Market Estimates and Forecast, By Operational Size, 2021 - 2034 (USD Billion)

7.1 Key trends

7.2 Small-scale operations

7.3 Medium-sized farms

7.4 Large sized farms

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion)

8.1 Key trends

8.2 Crops

8.3 Livestock

Chapter 9 Market Estimates and Forecast, By Service Type, 2021 - 2034 (USD Billion)

9.1 Key trends

9.2 Preventive maintenance services

9.3 Corrective maintenance services

9.4 Predictive maintenance services

9.5 Condition-based maintenance services

9.6 Emergency maintenance services

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)