Nanomaterials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871159

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

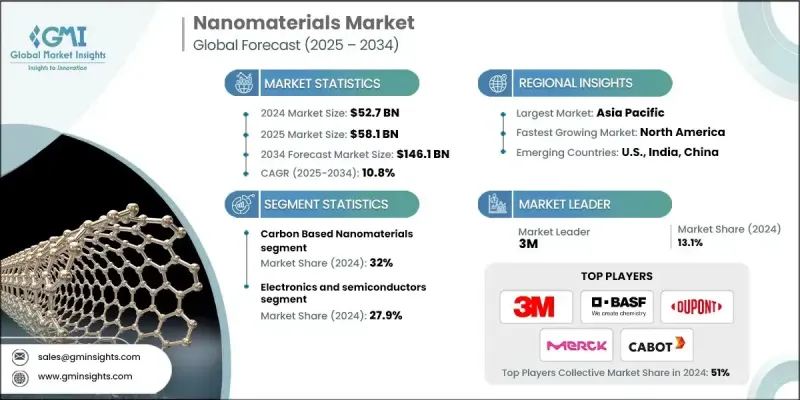

세계의 나노소재 시장은 2024년 527억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 10.8%를 나타낼 것으로 예측되며 1,461억 달러에 달할 것으로 예측되고 있습니다.

전자, 에너지, 의료, 환경 기술 등 다양한 부문에서 나노 규모 소재에 대한 수요가 급증하면서 시장 성장이 가속화되고 있습니다. 이러한 첨단 소재는 제품 설계와 성능에 혁신을 가져오고 있으며, 비용 및 인증과 관련된 문제점보다 이점이 더 큰 경우가 많습니다. 핵심 인프라, 재생 에너지 시스템, 첨단 치료제 부문에서 나노소재의 사용이 증가하면서 상업적 잠재력도 확대되고 있습니다. 다양한 응용 부문가 지속적으로 등장함에 따라 생산 역량에 대한 투자는 업계 전반에 걸쳐 강세를 유지할 것으로 예상됩니다. 특히 의료 및 의학 응용 부문의 규제 진전은 나노소재 채택을 가속화할 전망입니다. 또한 탄소 기반 및 양자 소재 부문의 획기적 발전은 시범 프로그램이 본격적 제조로 전환되면서 대규모 상용화를 주도하고 있습니다. 전반적으로 시장 진화는 다중 산업에 걸쳐 성능, 지속 가능성 및 기능성을 향상시키는 소재 혁신에 의해 뒷받침된다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

527억 달러

예측 금액

1,461억 달러

CAGR

10.8%

나노소재가 5G 네트워크, 인공지능, 고밀도 사물인터넷(IoT) 생태계와 같은 첨단 기술과 융합되면서 산업 지형이 재편되고 있습니다. 이러한 소재들은 차세대 기기에서 캐리어 이동도, 전도도 및 열 관리 개선에 필수적입니다. 고온에서 효율적으로 작동하는 능력은 반도체 미세화 및 열 방출 기술 발전을 뒷받침합니다. 의료 부문에서는 표적 약물 전달에 나노소재 사용이 증가하며, 치료제를 직접 영향을 받은 세포나 조직으로 운반함으로써 정밀 의학을 가능하게 합니다. 이러한 능력은 종양학, 면역학 및 감염성 질환 치료 부문에서 나노소재 채택 증가를 주도하고 있습니다.

탄소 기반 나노소재 부문은 2024년 32%의 점유율을 기록했습니다. 이 재료들은 반도체 제조, 복합재, 에너지 저장 시스템에서 광범위하게 활용되고 있습니다. 화학기상증착(CVD), 정렬 제어, 정제 등의 공정 기술 발전은 생산 비용과 불량률을 낮추면서 전기적·열적 특성을 크게 개선하고 있습니다. 그 결과 탄소 나노소재는 대량 전자 및 산업 제조에 점점 더 많이 활용되고 있습니다.

전자 및 반도체 부문은 2024년 27.9%의 점유율을 차지했습니다. 더 작고 빠르며 에너지 효율적인 전자 부품에 대한 수요로 인해 이 부문의 채택은 계속 증가하고 있습니다. 나노소재는 특히 5G, 에지 컴퓨팅 및 AI 기반 장치에서 회로의 소형화와 전도성 향상에 필수적입니다. 기존 구리나 실리콘을 대체하기보다는, 이러한 소재들은 차세대 전자 기기에 중요한 상호 연결 저항, 열 병목 현상, 유연성 요인 등의 한계를 해결함으로써 기존 아키텍처를 향상시킵니다.

미국의 나노소재 시장은 2024년 125억 달러로 평가되었고, 2034년까지 346억 달러에 달할 전망입니다. 이러한 성장세는 국가 차원의 이니셔티브를 통한 강력한 정부 조정과 산업 규모 확대를 촉진하는 활발한 자본 시장의 지원으로 뒷받침됩니다. 나노의학, 반도체, 첨단 소재 연구개발(R&D) 부문에서 이 지역의 선도적 입지는 실험실 혁신에서 대규모 상업 생산으로의 전환을 가속화했습니다. 캐나다에서는 청정 에너지 및 환경 응용 부문를 지원하는 지속 가능한 나노소재 솔루션에 초점을 맞추고 있으며, 이는 생태 효율적 기술로의 광범위한 추세를 반영합니다.

세계의 나노소재 시장의 주요 기업으로는 바스프(BASF), 3M, 듀폰 드 네무르(DuPont de Nemours), 캐봇 코퍼레이션(Cabot Corporation), 머크(Merck), 나노코 테크놀로지스(Nanoco Technologies), 나노시스(Nanosys) 등이 있습니다. 나노소재 업계 기업들은 시장 입지를 강화하기 위해 여러 전략적 접근법을 활용하고 있습니다. 이들은 제품 효율성 향상, 생산 비용 절감, 전자·의료·에너지 등 최종 사용 산업의 변화하는 요구 사항 충족을 위해 대규모 연구개발(R&D) 투자를 최우선 과제로 삼고 있습니다. 기업들은 제품 혁신과 상용화를 가속화하기 위해 기술 공급업체 및 연구 기관과 전략적 파트너십 및 협력을 체결하고 있습니다. 지속가능성과 규제 준수에 대한 관심도 높아지면서 친환경 소재와 더 안전한 생산 방법 개발이 촉진되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 억제요인 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경적 측면

지속가능한 대처

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 규모와 예측 : 제품 유형별(2021-2034년)

주요 동향

탄소 기반 나노소재

단일벽 탄소나노튜브

다중벽 탄소나노튜브

그래핀 및 그래핀 유도체

풀러렌 및 탄소 나노스피어

탄소 나노섬유

금속 산화물 나노 입자

이산화티탄(TiO2) 나노입자

산화아연(ZnO) 나노입자

이산화규소(SiO2) 나노입자

산화세륨(CeO2) 나노입자

산화철 나노입자

양자점 및 반도체 나노결정

고분자 나노입자

지질 기반 나노입자

제로가 금속 나노입자

제6장 시장 규모와 예측 : 용도별(2021-2034년)

주요 동향

전자기기 및 반도체

전도성 잉크 및 코팅

메모리 디바이스 및 데이터 스토리지

센서 및 검출기

디스플레이 기술

의료 및 바이오메디컬

약물 전달 시스템

의료 영상 진단

재생 의학

항균 용도

화장품 및 퍼스널케어

자외선 방지 및 선스크린

안티 에이징 스킨 케어

색조 화장품

에너지 및 환경

태양전지 및 태양광 발전

에너지 저장 시스템

촉매 및 연료전지

수처리 및 정화

코팅 및 표면 처리

보호 코팅

자기 세정 표면

항균 코팅

섬유 및 패브릭

기능성 섬유

스마트 패브릭

보호복

제7장 시장 규모와 예측 : 최종 용도별(2021-2034년)

주요 동향

화학 제조

특수 화학 제품

산업용 화학 제품

촉매 및 첨가제

전자기기 및 컴퓨터 제조

반도체 제조

전자부품

프린트 기판

의약품 및 생명공학

약제 제제 및 전달 기술

의료기기 제조

진단 시스템

자동차 및 운송

경량 재료

코팅 및 표면 처리

센서 및 전자 기기

건설 및 건축자재

콘크리트 시멘트 첨가제

단열재

보호 코팅

연구개발 서비스

제8장 시장 규모와 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

3M

BASF

DuPont de Nemours

Merck

Cabot Corporation

Nanosys

Nanoco Technologies

OCSiAl Group

Advanced Nano Products

Strem Chemicals

UbiQD

NN-Labs

Particular Materials

HBR

영문 목차

영문목차

The Global Nanomaterials Market was valued at USD 52.7 Billion in 2024 and is estimated to grow at a CAGR of 10.8% to reach USD 146.1 Billion by 2034.

The surging demand for nanoscale materials across sectors such as electronics, energy, healthcare, and environmental technology is fueling robust market growth. These advanced materials are revolutionizing product design and performance, with benefits that often outweigh the challenges associated with cost and certification. The growing use of nanomaterials in critical infrastructure, renewable energy systems, and advanced therapeutics is broadening their commercial potential. As diverse applications continue to emerge, investment in production capabilities is expected to remain strong across the industry. Regulatory progress, especially in healthcare and medical applications, is likely to accelerate the adoption of nanomaterials. Additionally, breakthroughs in carbon-based and quantum materials are driving mass-scale commercialization as pilot programs transition into full-scale manufacturing. Overall, the market's evolution is supported by material innovations that enhance performance, sustainability, and functionality across multiple industries.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$52.7 Billion

Forecast Value

$146.1 Billion

CAGR

10.8%

The convergence of nanomaterials with advanced technologies such as 5G networks, artificial intelligence, and dense Internet of Things (IoT) ecosystems is reshaping the industry landscape. These materials are essential for improving carrier mobility, conductivity, and thermal management in next-generation devices. Their ability to operate efficiently at high temperatures supports advancements in semiconductor scaling and heat dissipation. In healthcare, nanomaterials are increasingly used in targeted drug delivery, enabling precision medicine by transporting therapeutic agents directly to affected cells or tissues. Such capabilities are driving their growing adoption in oncology, immunology, and infectious disease treatment.

The carbon-based nanomaterials segment held a 32% share in 2024. These materials are finding widespread applications in semiconductor fabrication, composites, and energy storage systems. Technological advances in processes such as chemical vapor deposition, alignment control, and purification are significantly improving electrical and thermal properties while reducing production costs and defect rates. As a result, carbon nanomaterials are increasingly being utilized for high-volume electronic and industrial manufacturing.

The electronics and semiconductor segment held a 27.9% share in 2024. Their adoption continues to rise due to the demand for smaller, faster, and more energy-efficient electronic components. Nanomaterials are vital to the miniaturization and improved conductivity of circuits, particularly in 5G, edge computing, and AI-based devices. Rather than replacing traditional copper or silicon, these materials enhance existing architectures by addressing limitations in interconnect resistance, thermal bottlenecks, and flexibility factors critical to next-generation electronic devices.

U.S. Nanomaterials Market was valued at USD 12.5 Billion in 2024 and is estimated to reach USD 34.6 Billion by 2034. This momentum is supported by strong government coordination through national initiatives and an active capital market that promotes industrial scale-up. The region's leadership in nanomedicine, semiconductors, and advanced material R&D has accelerated the transition from laboratory innovation to large-scale commercial production. In Canada, the focus remains on sustainable nanomaterial solutions that support clean energy and environmental applications, reflecting a broader trend toward eco-efficient technologies.

Leading players in the Global Nanomaterials Market include BASF, 3M, DuPont de Nemours, Cabot Corporation, Merck, Nanoco Technologies, and Nanosys. To strengthen their market position, companies in the nanomaterials industry are employing several strategic approaches. They are prioritizing large-scale R&D investments to enhance product efficiency, reduce production costs, and meet the evolving requirements of end-use industries such as electronics, healthcare, and energy. Firms are entering strategic partnerships and collaborations with technology providers and research institutions to accelerate product innovation and commercialization. The focus on sustainability and regulatory compliance has also intensified, prompting the development of eco-friendly materials and safer production methods.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Product Type

2.2.2 Application

2.2.3 End Use

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Product Type, 2021-2034 (USD Billion)

5.1 Key trends

5.2 Carbon-based nanomaterials

5.2.1 Single-walled carbon nanotubes

5.2.2 Multi-walled carbon nanotubes

5.2.3 Graphene & graphene derivatives

5.2.4 Fullerenes & carbon nanospheres

5.2.5 Carbon nanofibers

5.3 Metal oxide nanoparticles

5.3.1 Titanium dioxide (TiO2) nanoparticles

5.3.2 Zinc oxide (ZnO) nanoparticles

5.3.3 Silicon dioxide (SiO2) nanoparticles

5.3.4 Cerium oxide (CeO2) nanoparticles

5.3.5 Iron oxide nanoparticles

5.4 Quantum dots & semiconductor nanocrystals

5.5 Polymeric nanoparticles

5.6 Lipid-based nanoparticles

5.7 Zero-valent metal nanoparticles

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion)

6.1 Key trends

6.2 Electronics & semiconductors

6.2.1 Conductive inks & coatings

6.2.2 Memory devices & data storage

6.2.3 Sensors & detectors

6.2.4 Display technologies

6.3 Healthcare & biomedical

6.3.1 Drug delivery systems

6.3.2 Medical imaging & diagnostics

6.3.3 Regenerative medicine

6.3.4 Antimicrobial applications

6.4 Cosmetics & personal care

6.4.1 UV protection & sunscreens

6.4.2 Anti-aging & skin care

6.4.3 Color cosmetics

6.5 Energy & environment

6.5.1 Solar cells & photovoltaics

6.5.2 Energy storage systems

6.5.3 Catalysts & fuel cells

6.5.4 Water treatment & purification

6.6 Coatings & surface treatments

6.6.1 Protective coatings

6.6.2 Self-cleaning surfaces

6.6.3 Antimicrobial coatings

6.7 Textiles & fabrics

6.7.1 Functional textiles

6.7.2 Smart fabrics

6.7.3 Protective clothing

Chapter 7 Market Size and Forecast, By End Use, 2021-2034 (USD Billion)

7.1 Key trends

7.2 Chemical manufacturing

7.2.1 Specialty chemicals

7.2.2 Industrial chemicals

7.2.3 Catalysts & additives

7.3 Electronics & computer manufacturing

7.3.1 Semiconductor fabrication

7.3.2 Electronic components

7.3.3 Printed circuit boards

7.4 Pharmaceutical & biotechnology

7.4.1 Drug formulation & delivery

7.4.2 Medical device manufacturing

7.4.3 Diagnostic systems

7.5 Automotive & transportation

7.5.1 Lightweight materials

7.5.2 Coatings & surface treatments

7.5.3 Sensors & electronics

7.6 Construction & building materials

7.6.1 Concrete & cement additives

7.6.2 Insulation materials

7.6.3 Protective coatings

7.7 Research & development services

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion)