첨단 리소그래피용 포토레지스트 화학제품 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)

Photoresist Chemicals for Advanced Lithography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871100

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 192 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

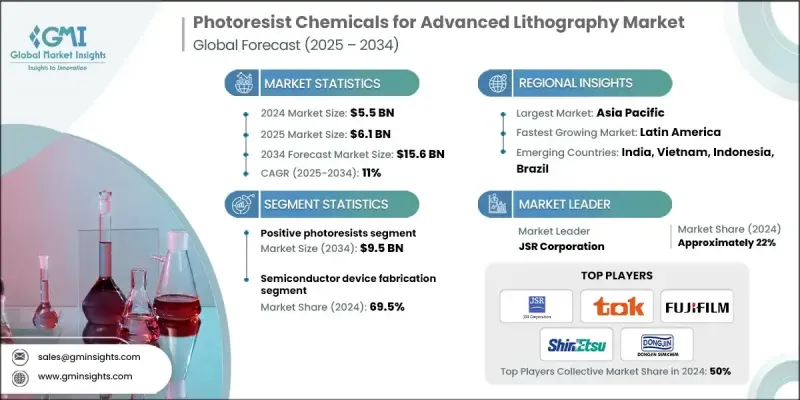

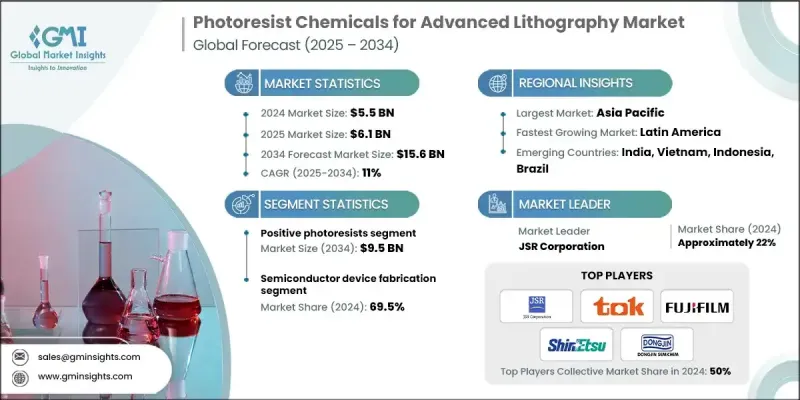

세계의 첨단 리소그래피용 포토레지스트 화학제품 시장은 2024년 55억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 11%로 성장하여 156억 달러에 이를 것으로 예측됩니다.

이 시장의 성장은 아시아태평양의 투자 증가, 높은 NA EUV 시스템의 상용화, 3D 패키징 기술의 발전으로 추진되고 있습니다. 7nm 미만 및 5nm 미만의 프로세스 노드 채용, EUV 리소그래피의 보급 확대, AI, 5G, 자동차용 고성능 칩 수요 증가가 이 변화를 견인하고 있습니다. 13.5nm 파장의 극자외선(EUV) 리소그래피 기술로 5nm의 선폭 패터닝이 가능해져 화학 증폭형 레지스트(CAR) 및 금속 산화물계 EUV 포토레지스트 수요가 대폭 증가하고 있습니다. 높은 NA EUV로의 진화, DUV와 EUV를 결합한 하이브리드 노광 기술, 지향성 자기 조직화(DSA) 기술의 발전은 레지스트의 화학 조성을 재구성하고 있습니다. JSR, TOK, Dongjin Semichem, Fujifilm 등 업계 리더 기업은 2nm 및 1.4nm 노드 대응을 위한 제품 로드맵을 정비하고 있어, 기존 KrF/i-line 레지스트로부터 EUV 중심의 플랫폼으로의 명확한 이행을 나타내고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

55억 달러

예측 금액

156억 달러

CAGR

11%

포지티브 포토레지스트 부문은 2024년 34억 달러 시장 규모를 기록했으며, CAGR 10.7%로 확대되어 2034년까지 95억 달러에 이를 것으로 전망됩니다. 이 부문에서는 화학 증감형 레지스트가 주류이며, 10nm 이하의 미세 구조에 대해 높은 감도를 제공하여 정밀한 프로세스 제어를 가능하게 하고 있습니다. 이 부문의 혁신은 에칭 내성의 향상, 모듈형 포토레지스트의 개발, EUV 리소그래피에서의 2차 전자 블러의 저감에 초점을 맞추고, 모두 미세화에서의 수율 극대화에 필수적인 요소입니다.

반도체 디바이스 제조 부문은 첨단 로직, 메모리, 아날로그, AI용 칩에 사용되는 고순도 및 고성능 포토레지스트 수요에 의해 2024년에는 69.5%의 점유율을 차지했습니다. 멀티패터닝의 복잡화와 높은 NA EUV의 채용이 진행되고 있는 가운데, 5nm, 3nm, 그리고 곧 2nm 프로세스로 제조되는 CPU, GPU, SoC등의 로직 디바이스가 포토레지스트 재료의 최대 소비 부문이 되고 있습니다.

미국의 첨단 리소그래피용 포토레지스트 화학제품 시장은 2024년 8억 1,740만 달러였고, 2034년까지 연평균 복합 성장률(CAGR) 10.8%로 성장해 23억 달러에 이를 것으로 예측되고 있습니다. 북미의 성장은 국내 반도체 생산을 촉진하는 입법을 포함한 반도체 진흥 정책에 의해 견인되고 있습니다. 주요 제조업체에 의한 신규 제조 시설의 설립에 따라, 이러한 정책은 현지 조달된 포토레지스트 및 첨단 리소그래피 재료 수요를 촉진하고 있습니다.

첨단 리소그래피용 포토레지스트 화학제품 시장의 주요 기업으로는 Merck KGaA, Brewer Science, Inc., Dow, Fujifilm Holdings Corporation, Inpria Corporation, Dongjin Semichem Co., Ltd., Eternal Materials Co., Ltd., Shin-Etsu Chemical Co., Ltd., JSR Corporation, Kayaku Advanced Materials, Tokyo Ohka Kogyo Co., Ltd., Micro Resist Technology GmbH, Sumitomo Chemical Company, Jiangsu Nata Opto-electronic Material Co., Ltd., Irresistible Materials Ltd 등을 들 수 있습니다. 주요 기업은 높은 NA EUV 및 5nm 이하의 공정 노드에 적합한 차세대 레지스트 화학물질을 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다. 반도체 제조업체와의 전략적 제휴는 제품 혁신을 상업적 리소그래피 요구사항에 맞추는 데 도움이 됩니다. 기업은 지역 수요 증가에 대응하기 위해 아시아태평양 및 북미의 생산 능력을 확대하고 있습니다. 일부 기업은 하이브리드 리소그래피 솔루션과 지향성 자기 조직화 기술에 주력하여 제품 적용 범위를 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 위험 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

유형별

미래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경적 측면

지속가능한 실천

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병

제휴 및 협력관계

신제품 발매

사업 확대 계획

제5장 시장 추계 및 예측 : 유형별, 2021-2034년

주요 동향

포지티브 포토레지스트

아크릴레이트계 포토레지스트

노볼락계(dnq) 시스템

폴리(메틸메타크릴레이트)(PMMA)

네거티브 포토레지스트

에폭시계

실리콘 함유 레지스트

금속계 레지스트

제6장 시장 추계 및 예측 : 리소그래피 기술별, 2021-2034년

주요 동향

DUV 리소그래피

248nm krf 리소그래피

193nm dry 리소그래피

193nm 액침 리소그래피(arfi)

극자외선(EUV) 리소그래피

EUV @ 13.5 nm

높은 NA EUV

I선 리소그래피(365nm)

나노임프린트 리소그래피(NIL)

전자선 리소그래피

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

주요 동향

반도체 디바이스 제조

로직 디바이스

메모리 디바이스

엣지 디바이스

이미지 센서

MEMS 디바이스

자동차용 MEMS

소비자용 전자 기기용 MEMS

산업 및 의료용 MEMS

디스플레이 전자기기 용도

액정 디스플레이 제조

OLED 디스플레이 제조

차세대 디스플레이

고급 패키징 응용

3D 패키징

시스템 인 패키지(SIP)

웨이퍼 레벨 패키징(WLP)

포토마스크 제조

EUV 마스크

DUV 마스크

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Brewer Science, Inc.

동진세미켐 Co., Ltd.

Dow

Eternal Materials Co., Ltd.

Fujifilm Holdings Corporation

Inpria Corporation

Irresistible Materials Ltd.

Jiangsu Nata Opto-electronic Material Co., Ltd.

JSR Corporation

Kayaku Advanced Materials

Merck KGaA

Micro Resist Technology GmbH

Shin-Etsu Chemical Co., Ltd.

Sumitomo Chemical Company

Tokyo Ohka Kogyo Co., Ltd.

Others

JHS

영문 목차

영문목차

The Global Photoresist Chemicals for Advanced Lithography Market was valued at USD 5.5 Billion in 2024 and is estimated to grow at a CAGR of 11% to reach USD 15.6 Billion by 2034.

The market is being propelled by rising investments in the Asia-Pacific region, the commercialization of High-NA EUV systems, and advancements in 3D packaging technologies. The adoption of sub-7nm and sub-5nm process nodes, growing use of EUV lithography, and increasing demand for high-performance chips in AI, 5G, and automotive applications are driving this transformation. Extreme Ultraviolet (EUV) lithography at 13.5 nm wavelengths is enabling the patterning of 5nm line widths, significantly boosting demand for chemically amplified resists (CARs) and metal-oxide-based EUV photoresists. The evolution toward High-NA EUV, hybrid lithography combining DUV and EUV, and directed self-assembly (DSA) is reshaping resist chemistries. Industry leaders like JSR, TOK, Dongjin Semichem, and Fujifilm are aligning product roadmaps with 2nm and 1.4nm node readiness, marking a clear shift from traditional KrF/i-line resists to EUV-focused platforms.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$5.5 Billion

Forecast Value

$15.6 Billion

CAGR

11%

The positive photoresists segment generated USD 3.4 Billion in 2024 and is expected to reach USD 9.5 Billion by 2034, growing at a CAGR of 10.7%. Chemically amplified resists dominate this segment, offering high sensitivity for sub-10nm geometries and enabling precise process control. Innovations in this space focus on improving etch resistance, developing modular photoresist options, and minimizing secondary electron blur in EUV lithography, all critical to maximizing yields at small dimensions.

The semiconductor device fabrication segment held a 69.5% share in 2024 owing to its need for high-purity, high-performance photoresists used in advanced logic, memory, analog, and AI-focused chips. Increasing multi-patterning complexity and High-NA EUV adoption make logic devices, including CPUs, GPUs, and SoCs produced at 5nm, 3nm, and soon 2nm nodes, the largest consumers of photoresist materials.

U.S. Photoresist Chemicals for Advanced Lithography Market generated USD 817.4 million in 2024 and is expected to grow at a CAGR of 10.8% to reach USD 2.3 Billion by 2034. North America's growth is being fueled by semiconductor revitalization policies, including legislation encouraging domestic chip production. These policies are driving the demand for locally sourced photoresist and advanced lithography materials as new fabrication facilities are established by major manufacturers.

Key players in the Photoresist Chemicals for Advanced Lithography Market include Merck KGaA, Brewer Science, Inc., Dow, Fujifilm Holdings Corporation, Inpria Corporation, Dongjin Semichem Co., Ltd., Eternal Materials Co., Ltd., Shin-Etsu Chemical Co., Ltd., JSR Corporation, Kayaku Advanced Materials, Tokyo Ohka Kogyo Co., Ltd., Micro Resist Technology GmbH, Sumitomo Chemical Company, Jiangsu Nata Opto-electronic Material Co., Ltd., and Irresistible Materials Ltd. Leading companies are investing heavily in R&D to develop next-generation resist chemistries suitable for High-NA EUV and sub-5nm process nodes. Strategic collaborations with semiconductor manufacturers help align product innovations with commercial lithography requirements. Firms are expanding production capacities in Asia-Pacific and North America to meet rising regional demand. Some players focus on hybrid lithography solutions and directed self-assembly technologies to broaden product applicability.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Lithography technology

2.2.4 End use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Price trends

3.7.1 By region

3.7.2 By type

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics ( Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and Environmental Aspects

3.12.1 Sustainable Practices

3.12.2 Waste Reduction Strategies

3.12.3 Energy Efficiency in Production

3.12.4 Eco-friendly Initiatives

3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million) (Tons)

5.1 Key trends

5.2 Positive photoresists

5.2.1 Acrylate-based photoresists

5.2.2 Novolac-based (dnq) systems

5.2.3 Poly (methyl methacrylate) (PMMA)

5.3 Negative photoresists

5.3.1 Epoxy-based

5.3.2 Silicon-containing resists

5.3.3 Metal-based resists

Chapter 6 Market Estimates and Forecast, By Lithography Technology, 2021 - 2034 (USD Million) (Tons)

6.1 Key trends

6.2 Duv lithography

6.2.1 248nm krf lithography

6.2.2 193nm dry lithography

6.2.3 193nm immersion lithography (arfi)

6.3 Extreme ultraviolet (euv) lithography

6.3.1 Euv @ 13.5 nm

6.3.2 High-na euv

6.4 I-line lithography (365 nm)

6.5 Nanoimprint lithography (nil)

6.6 E-beam lithography

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Tons)

7.1 Key trends

7.2 Semiconductor device fabrication

7.2.1 Logic devices

7.2.2 Memory devices

7.2.3 Edge devices

7.2.4 Image sensors

7.3 Mems devices

7.3.1 Automotive mems

7.3.2 Consumer electronics mems

7.3.3 Industrial & healthcare mems

7.4 Display electronics applications

7.4.1 LCD manufacturing

7.4.2 OLED display production

7.4.3 Next-generation displays

7.5 Advanced packaging applications

7.5.1 3d packaging

7.5.2 System-in-package (SIP)

7.5.3 Wafer-level packaging (WLP)

7.6 Photomask manufacturing

7.6.1 EUV mask

7.6.2 DUV mask

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 UK

8.3.3 France

8.3.4 Spain

8.3.5 Italy

8.3.6 Rest of Europe

8.4 Asia Pacific

8.4.1 China

8.4.2 India

8.4.3 Japan

8.4.4 Australia

8.4.5 South Korea

8.4.6 Rest of Asia Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.5.4 Rest of Latin America

8.6 Middle East and Africa

8.6.1 Saudi Arabia

8.6.2 South Africa

8.6.3 UAE

8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

9.1 Brewer Science, Inc.

9.2 Dongjin Semichem Co., Ltd.

9.3 Dow

9.4 Eternal Materials Co., Ltd.

9.5 Fujifilm Holdings Corporation

9.6 Inpria Corporation

9.7 Irresistible Materials Ltd.

9.8 Jiangsu Nata Opto-electronic Material Co., Ltd.