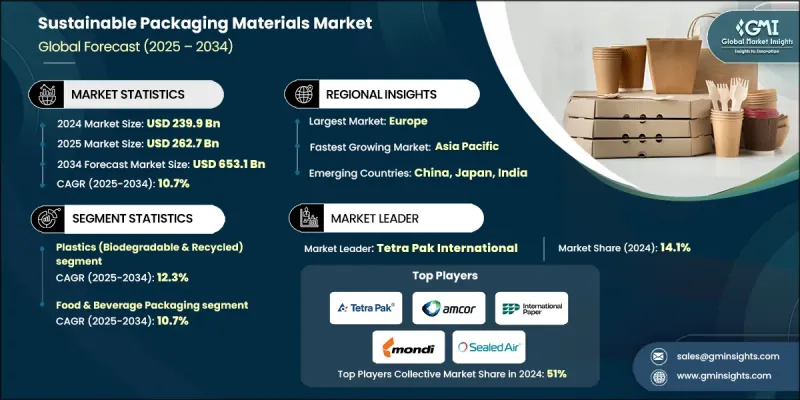

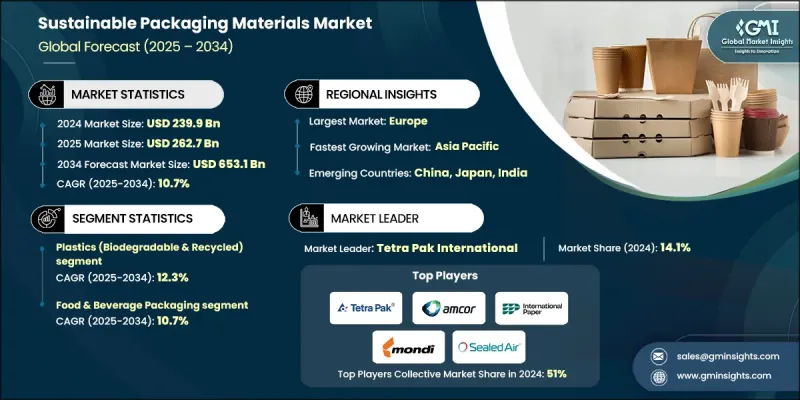

세계의 지속가능 포장 재료 시장은 2024년 2,399억 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 10.7%를 나타내 6,531억 달러에 이를 것으로 예측됩니다.

시장 성장은 주로 포장 폐기물을 최소화하기 위한 규제 강화와 세계 지속가능성 이니셔티브에 의해 추진되고 있습니다. 세계 각국의 정부는 환경정책을 강화하고 확대생산자책임(EPR), 일회용 플라스틱의 금지, 포장재에 대한 재생재 사용의무화 등의 조치를 도입하고 있습니다. 이러한 규제는 제조업체가 환경 친화적인 규제 준수 패키지 솔루션으로의 전환을 강요합니다. 또한 재료 과학의 지속적인 진화로 지속가능 재료의 성능, 확장 성 및 저렴한 가격이 향상되었습니다. 선별 기술에 대한 인공지능(AI)과 머신러닝의 통합은 재활용 및 회수 프로세스를 최적화하는 반면 생산 기술의 혁신은 생분해성 재료의 비용 효율성을 향상시킵니다. 첨단 바이오플라스틱과 재생가능한 복합재료를 포함한 바이오베이스 및 퇴비화가능한 재료의 기술적 진보는 내구성, 강도, 가격 설정에 대한 전통적인 한계를 극복하는 데 기여하고 있습니다. 이러한 혁신은 환경 목표와 기업의 지속가능성에 대한 노력에 따라 세계 산업에서 지속가능 포장 대체품의 급속한 보급의 기반을 마련하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 2,399억 달러 |

| 예측 금액 | 6,531억 달러 |

| CAGR | 10.7% |

플라스틱 분야는 2024년에 34%의 점유율을 차지했고 2025년부터 2034년에 걸쳐 CAGR 12.3%를 나타낼 것으로 예측됩니다. 이 카테고리에는 재생가능한 자원에서 생산되는 바이오플라스틱, 재생플라스틱 포장, 지속가능성과 성능의 균형을 맞추는 하이브리드 복합재료가 포함됩니다. 이러한 재료에 대한 수요 증가는 기존 플라스틱과 동등한 기능적 특성을 제공하면서 폐기시 환경 이점을 향상시키는 능력에 의해 추진되고 있습니다. 식품 포장, 퍼스널케어 제품, 전자상거래의 배송 자재 등 폭넓은 분야에서의 사용은 환경 목표를 달성하면서 제품의 안전성과 소비자의 편리성을 유지하는 데 있어서 적응성과 중요성을 뒷받침하고 있습니다.

식품 및 음료 포장 용도는 2024년에 50%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 10.7%를 나타낼 것으로 예측됩니다. 이 이점은 식품의 안전성을 확보하고, 보존 기간을 연장하고, 사용 용이성을 향상시키는 포장의 중요성으로 인해 발생합니다. 이 분야에서는 식품 접촉과 장벽 특성에 대한 엄격한 요구 사항이 부과되어 지속가능 재료의 선택에 영향을 미칩니다. 친환경 식품 포장에 대한 규제 모니터링 강화와 소비자 수요 증가는 안전과 지속가능성 기준을 모두 충족하는 소재의 지속적인 혁신을 촉진하고 있습니다. 제조업체는 품질과 기능성을 유지하면서 환경 부하를 줄이는 에코 효율적인 포장 옵션 개발을 적극적으로 추진하고 있습니다.

미국의 지속가능 포장 재료 시장은 2024년에 531억 달러에 이르렀으며, 주 수준의 강력한 규제, 기업의 지속가능성에 대한 노력 강화, 환경문제에 대한 소비자 의식 증가를 배경으로 2034년까지 1,402억 달러에 이를 것으로 예측됩니다. 이 지역은 정비 된 재활용 인프라와 지속가능 재료의 혁신을 지원하는 견고한 생태계의 혜택을 누리고 있습니다. 지속적인 기술 진보와 순환 경제 프로그램의 확대는 북미 전역 시장 성장을 더욱 강화하고 있습니다.

세계의 지속가능 포장 재료 시장에서 사업을 전개하는 주요 기업으로는 스토어 엔소 오이, 일본 제지 주식회사, 암코르 plc, 시일드 에어 코퍼레이션, 소노코 제품 회사, DS 스미스 plc, 테트라 팩 인터내셔널, 크로네스 AG, 몬디 그룹, 국제 페이퍼 컴퍼니 등이 있습니다. 지속가능 포장 재료 시장의 주요 기업은 경쟁 우위를 강화하기 위해 혁신, 협업, 순환 경제에 대한 노력에 주력하고 있습니다. 많은 기업들이 규제와 환경 기준을 충족하는 고성능 생분해성, 재활용 가능, 퇴비화 가능한 소재를 개발하기 위해 연구 개발 투자를 확대하고 있습니다. 소비자 브랜드 및 재활용 기술 기업과의 전략적 제휴는 지속가능 공급망과 폐쇄 루프 시스템의 확대에 기여하고 있습니다. 또한 기업은 경량화 전략을 채택하여 재료 사용량 삭감과 비용 효율성 향상을 도모하고 있습니다. 세계적인 제조 능력의 확대와 재활용 인프라의 통합 개선은 더욱 확장성을 지원하는 기반이 되고 있습니다.

The Global Sustainable Packaging Materials Market was valued at USD 239.9 Billion in 2024 and is estimated to grow at a CAGR of 10.7% to reach USD 653.1 Billion by 2034.

Market growth is propelled primarily by escalating regulatory mandates and global sustainability initiatives aimed at minimizing packaging waste. Governments across the world are tightening environmental policies and introducing measures such as extended producer responsibility (EPR), bans on single-use plastics, and mandatory recycled content in packaging. These regulations are compelling manufacturers to transition toward eco-friendly and compliant packaging solutions. The ongoing evolution of material science is also enhancing the performance, scalability, and affordability of sustainable materials. Integration of artificial intelligence and machine learning in sorting technologies is optimizing recycling and recovery processes, while innovations in production techniques are improving the cost efficiency of biodegradable materials. Breakthroughs in bio-based and compostable materials, including advanced bioplastics and renewable composites, are helping overcome previous limitations related to durability, strength, and pricing. These innovations are setting the stage for the rapid adoption of sustainable packaging alternatives across global industries, aligning with both environmental goals and corporate sustainability commitments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $239.9 Billion |

| Forecast Value | $653.1 Billion |

| CAGR | 10.7% |

The plastics segment held a 34% share in 2024 and is projected to grow at a CAGR of 12.3% during 2025-2034. This category encompasses bioplastics made from renewable resources, recycled plastic packaging, and hybrid composites that balance sustainability with performance. The growing demand for these materials is driven by their ability to match the functional properties of traditional plastics while offering enhanced end-of-life environmental benefits. Their widespread use across food packaging, personal care products, and e-commerce shipping materials underscores their adaptability and importance in maintaining product safety and consumer convenience while meeting environmental objectives.

The food & beverage packaging application held a 50% share in 2024 and is forecasted to grow at a CAGR of 10.7% through 2034. This dominance stems from the critical need for packaging that ensures food safety, preserves shelf life, and enhances usability. The sector faces stringent food contact and barrier property requirements, which influence the choice of sustainable materials. Growing regulatory oversight and consumer demand for environmentally friendly food packaging have encouraged continuous innovation in materials that meet both safety and sustainability standards. Manufacturers are actively developing eco-efficient packaging options that maintain quality and functionality while reducing environmental impact.

United States Sustainable Packaging Materials Market reached USD 53.1 Billion in 2024 and is projected to reach USD 140.2 Billion by 2034, driven by robust state-level regulations, heightened corporate sustainability initiatives, and increasing consumer awareness regarding environmental issues. The region benefits from a well-developed recycling infrastructure and a strong ecosystem for innovation in sustainable materials. Continuous technological advancements and expanding circular economy programs are further supporting market growth across North America.

Key companies operating in the Global Sustainable Packaging Materials Market include Stora Enso Oyj, Nippon Paper Industries, Amcor plc, Sealed Air Corporation, Sonoco Products Company, DS Smith plc, Tetra Pak International, Krones AG, Mondi Group, and International Paper Company. Leading companies in the Sustainable Packaging Materials Market are focusing on innovation, collaboration, and circular economy initiatives to strengthen their competitive edge. Many are increasing R&D investments to develop high-performance biodegradable, recyclable, and compostable materials that meet regulatory and environmental standards. Strategic partnerships with consumer brands and recycling technology firms are helping expand sustainable supply chains and closed-loop systems. Companies are also adopting lightweighting strategies to reduce material use and enhance cost efficiency. Expanding global manufacturing capacities and improving recycling infrastructure integration are further supporting scalability.