보로펜(Borophene) 시장 : 시장 기회 및 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Borophene Applications Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1858884

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

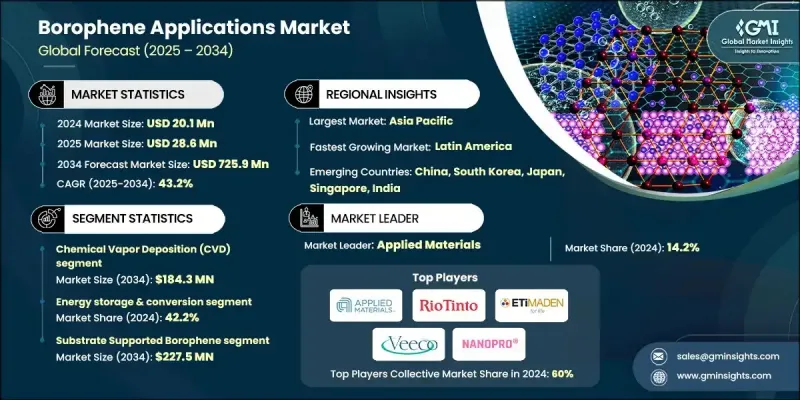

세계의 보로펜 시장은 2024년에 2,010만 달러로 평가되었고, CAGR 43.2%로 성장할 전망이며, 2034년에는 7억 2,590만 달러에 이를 것으로 추정되고 있습니다.

이 놀라운 성장은 보로펜의 독특한 전도성, 유연성 및 지향성의 조합으로 인해 첨단 분야에서 많은 기존 재료를 능가합니다. 신재생 에너지 발전과 전동 모빌리티를 둘러싼 세계적인 기운이 높아짐에 따라 차세대 배터리 부품 수요가 높아지고 있습니다. 보로펜은 리튬 이온 배터리 시스템에서 이론 용량이 매우 높고 슈퍼커패시터의 전극에 적합하기 때문에 높은 가능성을 지닌 후보로 부상하고 있습니다. 이 재료는 섬세한 합성이 요구되기 때문에 상업적 확장성은 여전히 과제이지만, 최근의 기술 진보로 제조 기술이 크게 개선되었습니다. 여기에는 화학 처리 및 박리 기술의 혁신이 포함되어 있어 대규모 전개에 대한 길이 열리고 있습니다. 현재의 연구에 따르면, 보로펜은 기존의 흑연 양극을 훨씬 능가하는 리튬 저장 잠재력을 가지고 있으며, 미래의 에너지 솔루션에서 획기적인 선택으로 자리매김하고 있습니다. 그 금속 특성과 조정 가능한 전자 거동을 결합하면 축전 시스템뿐만 아니라 전자, 센서 및 촉매 공정 전반에 변화의 잠재력을 제공합니다. 시장의 급 가속은 성능뿐만 아니라 재료 혁신에 대한 투자 증가를 반영합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

2,010만 달러

예측 금액

7억 2,590만 달러

CAGR

43.2%

화학 기상 성장(CVD) 기술은 안정적인 두께, 구조 및 우수한 품질의 보로펜 막을 생성하는 능력을 통해 2024년에는 520만 달러를 생산하였고, 2034년에는 1억 8,430만 달러에 이를 전망입니다. 이용 사례에서는 높은 재현성과 합성 변수의 정밀한 제어가 가능하며, 이는 고도의 용도에 적합한 특정 특성을 갖는 보로펜을 제조하는 데 매우 중요합니다. 이 공정은 기존의 반도체 제조 플랫폼과 원활하게 통합될 수 있기 때문에 전자 분야에서의 용도와 관련성이 높아집니다. 게다가 플라즈마 어시스트와 저온 CVD 접근법의 출현으로 제조 비용을 절감하면서 상업적으로 확장 가능한 공정이 되어 채용이 더욱 진행되고 있습니다.

에너지 저장 및 변환 분야는 2024년 42.2%의 점유율을 차지했습니다. 이 분야는 보로펜의 뛰어난 전도성, 높은 이론 에너지 용량, 고속 충방전 응답 특성으로부터 큰 혜택을 받고 있으며, 리튬 이온 배터리, 수소 시스템, 연료전지 부품에 대한 통합을 위한 연구가 활발히 이루어지고 있습니다. 보로펜을 청정에너지 인프라에 실용화하기 위한 연구개발을 가속화하기 위해 세계의 에너지 및 배터리 기술 기업이 많은 돈을 지원하고 있습니다.

북미의 보로펜 2024년 시장 규모는 560만 달러로 평가되었고, 2034년에는 1억 8,770만 달러에 이를 전망이며, CAGR 42%로 성장할 것으로 예측됩니다. 이 지역은 학술기관, 첨단 재료 신흥기업, 벤처 캐피탈 등 확립된 생태계의 혜택을 누리고 있습니다. 과학연구 및 산업 개발의 강한 결합이 혁신을 뒷받침하고 있으며, 특히 보로펜이 주목받고 있는 일렉트로닉스 및 방위 기술 등의 분야에서 현저합니다.

세계의 보로펜 시장을 형성하는 주요 기업으로는 Nano Pro Ceramic, Veeco Instruments, Applied Materials, Eti Maden, Rio Tinto 등이 있습니다. 보로펜 시장의 기업은 시장에서의 지위를 확보 및 확장하기 위해 다방면에 걸치는 전략을 전개하고 있습니다. 대기업은 확장 가능한 생산 방법을 개발하고 고급 이용 사례를 위한 재료 품질을 향상시키기 위해 대규모 연구개발 투자를 선호합니다. 기술 공급자 및 학술 기관의 파트너십은 재료 혁신 및 상업화를 가속화하는 데 도움이 됩니다. 기업은 또한 보로펜 생산 능력을 기존 인프라와 통합하여 비용을 절감하고 시장 출시를 가속화하고 있습니다. 전략적 제휴, 합병 및 인수는 독자적인 기술을 획득하고 지적 재산 포트폴리오를 강화하기 위해 활용됩니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 위험 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

향후 시장 동향

기술 및 혁신의 전망

현재의 기술 동향

신흥 기술

특허사정

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 대해서만 제공됨)

주요 수입국

주요 수출국

지속가능성 및 환경 측면

지속가능한 관행

폐기물 감축 전략

생산에서의 에너지 효율

환경 친화적인 노력

탄소발자국

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

파트너십

신제품 발표

확장 계획

제5장 시장 규모 및 예측 : 합성 방법별(2021-2034년)

주요 동향

분자선 에피택시(MBE)

화학 기상 성장법(CVD)

액상 박리법

전기화학적 및 기계적 박리법

기타

제6장 시장 규모 및 예측 : 제품 형태별(2021-2034년)

주요 동향

기판지지 보로펜

자립막 및 전사막

관능기화 보로펜 유도체

복합재료 및 하이브리드 재료

보로펜 및 그래핀 헤테로 구조

폴리머 복합재료

세라믹 및 금속 매트릭스 복합재료

나노구조체

보로펜 양자점

보로펜 나노튜브 및 나노리본

3D 보로펜 구조체

제7장 시장 규모 및 예측 : 용도별(2021-2034년)

주요 동향

에너지 저장 및 변환

리튬 이온 배터리 음극

슈퍼커패시터 전극

수소 저장

연료전지 촉매

일렉트로닉스 및 옵토일렉트로닉스

플렉서블 일렉트로닉스 및 웨어러블 디바이스

광검출기 및 센서

메모리 디바이스 인테그레이션

투명 도체

촉매 및 화학 처리

수소 발생 반응(HER) 촉매

산소 발생 반응(OER)

CO2 삭감 및 환경 촉매

바이오메디컬 및 헬스케어

약물전달 시스템 통합

바이오 이미징 및 진단

암테라노스틱스 및 광열요법

환경 센서 및 용도

가스 센싱 기술 통합

수질 정화 및 환경 복구

바이오센서 개발 및 헬스케어 모니터링

제8장 시장 규모 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Rio Tinto

Eti Maden

Applied Materials

Veeco Instruments

Nano Pro Ceramic

Graphene Manufacturing Group

American Elements Corporation

Suzhou Graphene

AJY

영문 목차

영문목차

The Global Borophene Applications Market was valued at USD 20.1 million in 2024 and is estimated to grow at a CAGR of 43.2% to reach USD 725.9 million by 2034.

This extraordinary growth is driven by borophene's unique combination of electrical conductivity, flexibility, and directional properties, which outperform many traditional materials in advanced sectors. With rising global momentum around renewable energy and electric mobility, the demand for next-generation battery components is gaining traction. Borophene has emerged as a high-potential candidate due to its extremely high theoretical capacity in lithium-ion battery systems and suitability for use in supercapacitor electrodes. Although the material's commercial scalability remains a challenge because of its sensitive synthesis requirements, recent technological advancements have significantly improved production techniques. These include innovations in chemical processing and exfoliation technologies, which are making way for larger-scale deployment. Current studies indicate that borophene offers lithium storage potential far exceeding traditional graphite anodes, positioning it as a revolutionary option in future energy solutions. Its metallic characteristics, combined with tunable electronic behavior, offer transformative potential not just in storage systems but across electronics, sensors, and catalytic processes. The market's rapid acceleration reflects not only its performance capabilities but also rising investments into material innovation.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$20.1 Million

Forecast Value

$725.9 Million

CAGR

43.2%

The chemical vapor deposition (CVD) technology generated USD 5.2 million in 2024 to reach USD 184.3 million by 2034, driven by its ability to generate borophene films with consistent thickness, structure, and superior quality. CVD enables high reproducibility and precise control over synthesis variables, which is crucial for manufacturing borophene with specific traits suited for advanced use cases. This process seamlessly integrates with existing semiconductor fabrication platforms, enhancing its relevance for applications in the electronics space. Additionally, the emergence of plasma-assisted and low-temperature CVD approaches is making the process more commercially scalable while reducing production costs, further driving adoption.

The energy storage and conversion segment held a 42.2% share in 2024. This segment benefits greatly from borophene's superior conductivity, high theoretical energy capacity, and fast charge/discharge response attributes that are being actively researched for integration into lithium-ion batteries, hydrogen systems, and fuel cell components. Significant financial backing is being directed by global energy and battery technology players to accelerate R&D efforts that push borophene toward practical deployment in clean energy infrastructure.

North America Borophene Applications Market accounted for USD 5.6 million in 2024 and is expected to reach USD 187.7 million by 2034, growing at a CAGR of 42%. The region benefits from a well-established ecosystem of academic institutions, advanced materials startups, and supportive venture capital. Strong ties between scientific research and industrial development are propelling innovation, especially in fields like electronics and defense technologies, where borophene is gaining increased attention.

Key players shaping the Global Borophene Applications Market include Nano Pro Ceramic, Veeco Instruments, Applied Materials, Eti Maden, and Rio Tinto. Companies in the borophene applications market are deploying multi-pronged strategies to secure and expand their market positions. Major players are prioritizing heavy R&D investment to unlock scalable production methods and refine material quality for advanced use cases. Partnerships between technology providers and academic institutions are helping accelerate material innovation and commercialization. Firms are also integrating borophene production capabilities with existing infrastructure to lower costs and improve speed to market. Strategic alliances, mergers, and acquisitions are being leveraged to gain proprietary technologies and strengthen intellectual property portfolios.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Synthesis method

2.2.2 Product form

2.2.3 Application

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Synthesis Method, 2021-2034 (USD Million) (Kilo Tons)

5.1 Key trends

5.2 Molecular beam epitaxy (MBE)

5.3 Chemical vapor deposition (CVD)

5.4 Liquid-phase exfoliation methods

5.5 Electrochemical & mechanical exfoliation

5.6 Others

Chapter 6 Market Size and Forecast, By Product Form, 2021-2034 (USD Million) (Kilo Tons)

6.1 Key trends

6.2 Substrate-supported borophene

6.3 Free-standing & transferred films

6.4 Functionalized borophene derivatives

6.5 Composite & hybrid materials

6.5.1 Borophene-graphene heterostructures

6.5.2 Polymer composite integration

6.5.3 Ceramic & metal matrix composites

6.6 Nanostructured forms

6.6.1 Borophene quantum dots

6.6.2 Borophene nanotubes & nanoribbons

6.6.3 3D borophene structures

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

7.1 Key trends

7.2 Energy storage & conversion

7.2.1 Lithium-ion battery anodes

7.2.2 Supercapacitor electrode

7.2.3 Hydrogen storage

7.2.4 Fuel cell catalyst

7.3 Electronics & optoelectronics

7.3.1 Flexible electronics & wearable devices

7.3.2 Photodetector & sensor

7.3.3 Memory device integration

7.3.4 Transparent conductor

7.4 Catalysis & chemical processing

7.4.1 Hydrogen evolution reaction (HER) catalysts

7.4.2 Oxygen evolution reaction (OER)

7.4.3 Co2 reduction & environmental catalysis

7.5 Biomedical & healthcare

7.5.1 Drug delivery system integration

7.5.2 Bioimaging & diagnostic

7.5.3 Cancer theranostics & photothermal therapy

7.6 Environmental & sensor applications

7.6.1 Gas sensing technology integration

7.6.2 Water purification & environmental remediation

7.6.3 Biosensor development & healthcare monitoring

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 UK

8.3.2 Germany

8.3.3 France

8.3.4 Italy

8.3.5 Spain

8.3.6 Rest of Europe

8.4 Asia Pacific

8.4.1 China

8.4.2 India

8.4.3 Japan

8.4.4 South Korea

8.4.5 Australia

8.4.6 Rest of Asia Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.5.4 Rest of Latin America

8.6 Middle East & Africa

8.6.1 South Africa

8.6.2 Saudi Arabia

8.6.3 UAE

8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

9.1 Rio Tinto

9.2 Eti Maden

9.3 Applied Materials

9.4 Veeco Instruments

9.5 Nano Pro Ceramic

9.6 Graphene Manufacturing Group

9.7 American Elements Corporation

9.8 Suzhou Graphene

(주)글로벌인포메이션02-2025-2992kr-info@giikorea.co.kr ⓒ Copyright Global Information, Inc. All rights reserved.