소프트 로보틱스용 액정 엘라스토머 시장 : 시장 기회 및 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Liquid Crystal Elastomers for Soft Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1858864

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

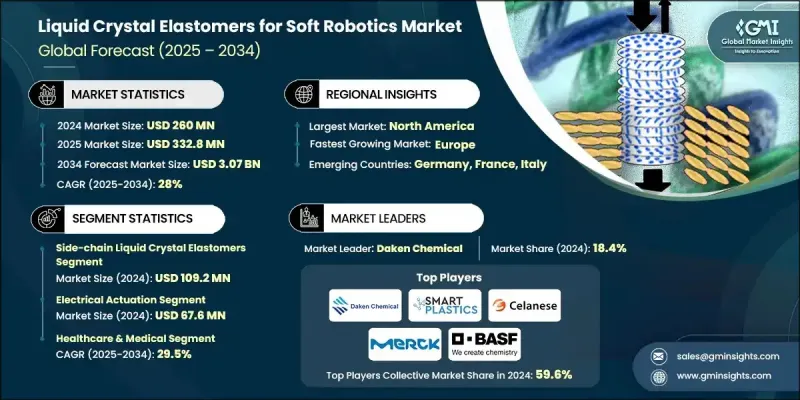

세계의 소프트 로보틱스용 액정 엘라스토머 시장 규모는 2024년에 2억 6,000만 달러로 평가되었고, CAGR 28%로 성장할 전망이며, 2034년에는 30억 7,000만 달러에 달할 것으로 예측되고 있습니다.

수요는 헬스케어, 소비자 기술, 자동화 등의 분야에서 기세를 늘리고 있으며, 성능과 통합의 진보가 중요한 역할을 하고 있습니다. 이 채용 곡선은 다른 파괴적 액추에이터 기술로 관찰된 동향을 반영한 것으로, 특히 LCE-textiles가 출력 밀도를 293W/kg, 작업 능력을 650J/kg에 도달시켜 천연 근육을 능가하기 시작합니다. 섬유 기반 및 직물 기반 시스템이 실제 부하 조건 하에서 일관되게 다기능 모션을 실현함에 따라 확장성 및 산업적 신뢰성에 대한 신뢰가 가속화되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

2억 6,000만 달러

예측 금액

30억 7,000만 달러

CAGR

28%

메소겐, 얼라인먼트층, 가교제를 조정할 필요가 있기 때문에 재료비는 전체의 약 35-40%를 차지하고, 정밀한 가교, 분자 얼라인먼트, 고정밀도의 기계 가공 등 기술적 요구에 의해 제조 비용은 한층 더 25-30%를 차지합니다. 그러나 이 비용 구조는 직접 잉크를 쓰는 방법이나 고급 섬유 압출 성형 등의 적층 제조법이 보급되어, 자본 요건이 삭감되고 설계의 자유도가 확대됨에 따라 진화하고 있습니다. 복잡한 형상과 부위에 특화된 재료 배열이 커스텀 금형 없이 가능하게 되어, 신속한 시제품 제작이나 최종 제품 라인의 다양화가 가능하게 되었습니다.

제조 서비스 부문의 2024년 점유율은 25%였으며, 이는 LCE의 완성 부품을 공급할 때 하이엔드 제조 기술의 역할을 반영하고 있습니다. 성능 중심의 구매가 재료 중심의 조달을 대체하고 있으며, 통합 시스템과 프로그래머블 액추에이션이 우선하게 되어 있습니다.

2024년에는 사이드 체인형 LCEs 부문이 1억 920만 달러를 차지했으며, 적응성, 비용 효율성 및 가공 용이성의 균형에서 압도적인 점유율을 획득했습니다. 측쇄형이 텍스타일 및 유연한 웨어러블에 뛰어난 한 편, 주쇄형이나 하이브리드 구조는 강도와 열안정성으로부터 항공우주, 로봇, 정밀 용도로 인기를 끌고 있습니다. 4D 프린팅 기술이 진화하여 다층 및 다소재를 높은 방향성으로 조형할 수 있게 되면 이러한 포맷 간 경쟁이 격화되고 포맷이 아닌 기능에 기반한 시장 세분화가 진행될 것으로 예측됩니다.

북미의 소프트 로보틱스용 액정 엘라스토머 시장은 2024년 45%의 점유율을 차지했습니다. 이 지역의 이점은 강력한 연구 생태계, 방위 주도 이니셔티브 및 의료 혁신에 의해 제공됩니다. 정부가 지원하는 연구개발은 금속화된 LCE 필름과 프로그램 가능한 열특성에 획기적인 혁신을 가져왔으며, 현재는 웨어러블 압축 시스템과 임상 등급의 인공 장비에 응용되고 있습니다. 미국 시장은 방위 및 헬스케어 수요로 확대되고 있으며 캐나다는 휴먼 머신 인터페이스용 소프트 액추에이션을 시험적으로 개발하는 대학의 로봇 공학 프로그램이 공헌하고 있습니다. 현재의 임상시험에서 20-60mmHg 사이에서 조절가능한 작동과 재사용 가능한 사이클이 입증되어 헬스케어 등급의 용도에 대한 신뢰가 강해지고 있습니다.

소프트 로보틱스용 액정 엘라스토머 주요 시장 진출기업은 Merck KGaA, BASF SE, Celanese Corporation, Beam Co, Daken Chemical, Smart-Plastics Ltd, Synton Chemicals, Wilshire Technologies, TCI America 등입니다. 소프트 로보틱스용 액정 엘라스토머 시장에서 경쟁하는 기업들은 장기적인 성장을 보장하기 위해 기술 혁신, 전략적 파트너십, 재료 엔지니어링을 활용하고 있습니다. LCE의 분자 설계, 내구성, 온도 안정성을 향상시키기 위해 중점적인 연구개발이 이루어지는 한편, 확장 가능한 포맷을 위한 합성 능력도 확대되고 있습니다. LCE 제조업체 각 회사는 맞춤형 형상 및 정렬 제어를 지원하기 위해 4D 프린팅 및 고급 압출 성형과 같은 정밀 제조 기술에 투자합니다. 학술기관 및 의료기기 개발 기업과의 협업은 의료, 항공우주, 웨어러블 기술에 대응하는 재료의 개발에 도움이 됩니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

자극 응답성 액추에이션 기능

적층 조형의 진보

자율 및 자립형 로봇 수요

스마트 텍스타일 및 웨어러블에 대한 통합

업계의 잠재적 위험 및 과제

느린 작동 속도

복잡한 제조 기술

한정된 전력 밀도

시장 기회

유연성과 정밀도를 높인 차세대 바이오 의료기기 개발 가능

스마트 웨어러블 및 반응형 텍스타일의 기술 혁신 촉진

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

향후 시장 동향

기술 혁신의 정세

현재의 기술 동향

신흥 기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 대해서만 제공됨)

주요 수입국

주요 수출국

지속가능성 및 환경 측면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경 친화적인 노력

탄소발자국

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

파트너십

신제품 발표

확장 계획

제5장 시장 추계 및 예측 : 재료 유형별(2021-2034년)

주요 동향

주쇄형 액정 엘라스토머

폴리실록산계 LCE

폴리아크릴레이트계 LCE

폴리에스테르 베이스 LCEs

폴리우레탄 베이스 LCE

측쇄형 액정 엘라스토머

엔드 온 사이드 체인 LCE

사이드 온 사이드 체인 LCE

라테랄 어태치드 LCE

이온성 액정 엘라스토머(iLCEs)

양이온성 iLCE

음이온성 iLCE

쌍성 이온성 iLCE

컴포지트 및 하이브리드 LCEs

탄소계 복합재료(CNT, 그래핀, GO)

금속 나노입자 복합재료(Au, Ag, Fe3O4)

액체 금속 매립 LCE

세라믹 충전 LCE

제6장 시장 추계 및 예측 : 작동 모드별(2021-2034년)

주요 동향

열 액추에이션

직접 열가열

줄 가열(전열)

유도 가열

광학 액추에이션

광화학(아조벤젠계)

광열(CNT, 금 나노입자)

근적외 응답성

가시광 응답

전기 액추에이션

유전 액추에이션

정전 액추에이션

이온 작동

자기장 액추에이션

마그네트 열

직접 자기 토크

멀티모달 액추에이션

열광학 복합

전기-열 복합

RF 제어 시스템

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

헬스케어 및 메디컬

의료기기 및 임플란트

의지 및 장구

약물전달 시스템

수술용 로봇

재활 장비

바이오메디컬 연구 툴

항공우주 및 방위

모핑 항공기 구조

적응 위장 시스템

전개 가능한 우주 구조물

자율형 군사 로봇

감시 및 정찰

미사일 및 로켓 부품

제조 및 산업 자동화

소프트 로봇 그리퍼

조립 라인 자동화

자재관리 시스템

품질관리 및 검사

패키징 및 가공

유지보수 및 수리 로봇

소비자용 전자기기 및 웨어러블

스마트 텍스타일 및 의류

웨어러블 헬스 모니터

촉각 피드백 장치

플렉서블 디스플레이

개인 지원 기기

게임 및 엔터테인먼트

자동차

어댑티브 좌석 시스템

액티브 에어로 다이나믹스

진동 감쇠

인테리어 컴포트 시스템

안전보호시스템

연구개발

학술연구기관

정부 연구소

재료 시험 및 특성 평가

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Smart-Plastics Ltd

Celanese Corporation

Merck KGaA

Synthon Chemicals

Beam Co

Wilshire Technologies

TCI America

BASF Corporation

Daken Chemical

AJY

영문 목차

영문목차

The Global Liquid Crystal Elastomers for Soft Robotics Market was valued at USD 260 million in 2024 and is estimated to grow at a CAGR of 28% to reach USD 3.07 billion by 2034.

The demand is gaining momentum across sectors like healthcare, consumer tech, and automation, with advancements in performance and integration playing a crucial role. The adoption curve mirrors trends observed in other disruptive actuator technologies, particularly as LCE fibers begin outperforming natural muscle with power density reaching 293 W/kg and work capacity up to 650 J/kg. As fiber-based and woven systems consistently deliver multifunctional motion under real load conditions, confidence in scalability and industrial reliability is accelerating.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$260 Million

Forecast Value

$3.07 Billion

CAGR

28%

Material costs account for approximately 35-40% of the total due to the need for tailored mesogens, alignment layers, and crosslinkers, while fabrication represents another 25-30% owing to technical demands like precise crosslinking, molecular alignment, and high-fidelity machining. However, this cost structure is evolving as additive manufacturing methods such as direct ink writing and advanced fiber extrusion gain traction, reducing capital requirements and expanding design freedom. Complex geometries and site-specific material alignment are now possible without custom molds, enabling quicker prototyping and diversified end-product lines.

The manufacturing services segment held 25% share in 2024, reflecting the role of high-end fabrication techniques in delivering finished LCE components. Performance-driven buying is increasingly replacing materials-focused procurement, with integrated systems and programmable actuation gaining priority.

In 2024, sidechain LCEs segment accounted for USD 109.2 million, capturing a dominant share due to their balance of adaptability, cost-efficiency, and ease of processing. While side-chain types excel in textiles and flexible wearables, main-chain and hybrid structures are gaining popularity in aerospace, robotics, and precision applications due to their strength and thermal stability. As 4D printing technologies evolve, allowing for multilayer, multimaterial builds with high directional control, the competitive edge between these formats is expected to tighten, leading to greater market segmentation based on function rather than format.

North America Liquid Crystal Elastomers for Soft Robotics Market held 45% share in 2024. The region's dominance is driven by strong research ecosystems, defense-led initiatives, and medical innovation. Government-backed R&D has led to breakthroughs in metallized LCE films and programmable thermal properties, which are now finding applications in wearable compression systems and clinical-grade prosthetics. The US market is expanding with defense and healthcare demand, while Canada's contribution is shaped by university-based robotics programs piloting soft actuation for human-machine interfaces. Current clinical pilots demonstrate adjustable actuation between 20-60 mmHg and reusable cycling, reinforcing confidence in healthcare-grade applications.

Key players active in the Liquid Crystal Elastomers for Soft Robotics Market include Merck KGaA, BASF SE, Celanese Corporation, Beam Co, Daken Chemical, Smart-Plastics Ltd, Synthon Chemicals, Wilshire Technologies, and TCI America. Companies competing in the Liquid Crystal Elastomers for Soft Robotics Market are leveraging innovation, strategic partnerships, and materials engineering to secure long-term growth. Focused R&D is being used to improve molecular design, durability, and temperature stability of LCEs while also expanding synthesis capabilities for scalable formats. Players are investing in precision manufacturing techniques such as 4D printing and advanced extrusion to support custom geometries and alignment control. Collaborations with academic institutions and medical device developers are helping firms tailor their materials to healthcare, aerospace, and wearable tech.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Admixtures

2.2.3 Application Methods

2.2.4 Application

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Stimuli-responsive actuation capabilities

3.2.1.2 Advancements in additive manufacturing

3.2.1.3 Demand for autonomous and self-sustained robotics

3.2.1.4 Integration into smart textiles and wearables

3.2.2 Industry pitfalls and challenges

3.2.2.1 Slow actuation speed

3.2.2.2 Complex fabrication techniques

3.2.2.3 Limited power density

3.2.3 Market opportunities

3.2.3.1 Enables development of next-gen biomedical devices with enhanced flexibility and precision

3.2.3.2 Facilitates innovation in smart wearables and responsive textiles

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation Landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and Innovation Landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Main-chain liquid crystal elastomers

5.2.1 Polysiloxane-based LCEs

5.2.2 Polyacrylate-based LCEs

5.2.3 Polyester-based LCEs

5.2.4 Polyurethane-based LCEs

5.3 Side-chain liquid crystal elastomers

5.3.1 End-on Sidechain LCEs

5.3.2 Side-on Sidechain LCEs

5.3.3 Laterally Attached LCEs

5.4 Ionic liquid crystal elastomers (iLCEs)

5.4.1 Cationic iLCEs

5.4.2 Anionic iLCEs

5.4.3 Zwitterionic iLCEs

5.5 Composite & hybrid LCEs

5.5.1 Carbon-based Composites (CNT, Graphene, GO)

5.5.2 Metal Nanoparticle Composites (Au, Ag, Fe3O4)

5.5.3 Liquid Metal Embedded LCEs

5.5.4 Ceramic-filled LCEs

Chapter 6 Market Estimates and Forecast, By Actuation Mode, 2021 - 2034 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Thermal actuation

6.2.1 Direct thermal heating

6.2.2 Joule heating (electrothermal)

6.2.3 Induction heating

6.3 Optical actuation

6.3.1 Photochemical (azobenzene-based)

6.3.2 Photothermal (CNT, gold nanoparticles)

6.3.3 Near-infrared responsive

6.3.4 Visible light responsive

6.4 Electrical actuation

6.4.1 Dielectric actuation

6.4.2 Electrostatic actuation

6.4.3 Ionic actuation

6.5 Magnetic field actuation

6.5.1 Magnetothermal

6.5.2 Direct magnetic torque

6.6 Multi-modal actuation

6.6.1 Thermal-optical combined

6.6.2 Electrical-thermal combined

6.6.3 Rf-controlled systems

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Healthcare & Medical

7.2.1 Medical devices & implants

7.2.2 Prosthetics & orthotics

7.2.3 Drug delivery systems

7.2.4 Surgical robotics

7.2.5 Rehabilitation equipment

7.2.6 Biomedical research tools

7.3 Aerospace & Defense

7.3.1 Morphing aircraft structures

7.3.2 Adaptive camouflage systems

7.3.3 Deployable space structures

7.3.4 Autonomous military robots

7.3.5 Surveillance & reconnaissance

7.3.6 Missile & rocket components

7.4 Manufacturing & Industrial Automation

7.4.1 Soft robotic grippers

7.4.2 Assembly line automation

7.4.3 Material handling systems

7.4.4 Quality control & inspection

7.4.5 Packaging & processing

7.4.6 Maintenance & repair robots

7.5 Consumer Electronics & Wearables

7.5.1 Smart textiles & clothing

7.5.2 Wearable health monitors

7.5.3 Haptic feedback devices

7.5.4 Flexible displays

7.5.5 Personal assistive devices

7.5.6 Gaming & entertainment

7.6 Automotive

7.6.1 Adaptive seating systems

7.6.2 Active aerodynamics

7.6.3 Vibration damping

7.6.4 Interior comfort systems

7.6.5 Safety & protection systems

7.7 Research & Development

7.7.1 Academic research institutions

7.7.2 Government research labs

7.7.3 Material testing & characterization

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)