볶지 않은 시리얼 플레이크 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Unroasted Cereal Flakes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1858809

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

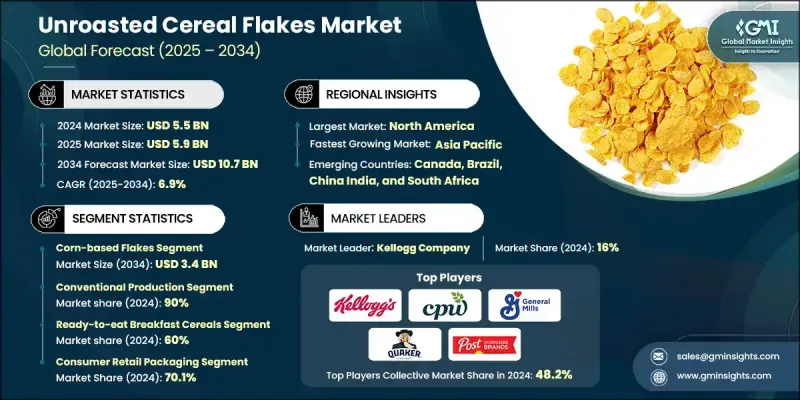

세계의 볶지 않은 시리얼 플레이크 시장은 2024년에는 55억 달러로 평가되었으며 CAGR 6.9%를 나타내 2034년에는 107억 달러에 이를 것으로 추정됩니다.

이 시장의 강력한 성장 전망은 진화하는 깨끗한 라벨과 영양의 투명성 기준에 따라 최소한의 가공을 한 전체 곡물 조식 제품에 대한 소비자 수요의 급증에 의해 지원되고 있습니다. FDA(미국 식품의약국)의 새로운 규제에 의해 「건강」의 정의가 갱신되고, 특정의 전곡 곡물의 최저량이 포함되는 한편, 첨가 당분, 포화 지방, 나트륨의 상한이 설정된 것은 볶지 않은 시리얼 플레이크의 포지셔닝을 강하게 추진하고 있습니다. 세계의 곡물 생산량은 항상 연간 30억 톤을 넘고 있으며, 곡물 산업은 안정적인 입력 공급 체인과 확장성으로 혜택을 누리며, 생산자는 전체 곡물의 조달과 투명성을 선호할 수 있습니다. 소비자들은 식이섬유와 전체 곡물을 중시하는 식생활 의식의 변화와 정부의 영양 권고의 갱신에 추진되어 원재료가 한정되어 가공 공정이 삭감된 시리얼 식품을 선호하게 되어 있습니다. 이로 인해 기능 강화와 영양 강화 등의 제품 혁신이 진행되어 편리성과 영양을 모두 요구하는 건강 지향의 쇼핑객에게 어필하고 있습니다. 식사 기준이 진화함에 따라 제조업체는 보건기구와 긴밀하게 협력하여 깨끗하고 단순하며 건강한 식품을 선택할 것으로 예상되는 제품을 제공합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

55억 달러

예측 금액

107억 달러

CAGR

6.9%

유기농 볶지 않은 시리얼 플레이크 분야는 합리화된 인증 프로세스와 대규모 곡물 생산과의 강한 결합에 힘입어 2034년까지 연평균 복합 성장률(CAGR) 8.9%를 나타낼 전망입니다. 재생농업도 CAGR 11%로 대두하고 있어, 이는 브랜드가 옹호단체와 협력해 농장 레벨의 이행 경로와 신뢰할 수 있는 검증 시스템을 확립하기 위해서입니다. 이와 같은 재생농업의 주장은 전문소매점에서의 지지를 모으고 있으며, 투입자재의 추적 가능성와 지속가능성의 문서화가 개선됨으로써 공급자가 보다 장기적인 계약을 확보하는데 도움이 되고 있습니다.

빨리 먹을 수 있는 로스팅되지 않은 플레이크 부문은 60%의 점유율을 차지하며, 2034년까지의 CAGR은 6.9%를 나타낼 것으로 예상됩니다. 이러한 시리얼은 편의성, 확립된 소비자 습관, 진화하는 선호도에 대응하는 지속적인 제품 혁신으로 인기가 높습니다. 이 제품은 영양가가 높고 요리가 쉬운 선택을 요구하는 바쁜 소비자층을 지원하며, 웰니스 지향 개인을 대상으로 하는 깨끗한 라벨과 기능성 표시로 프리미엄 부문을 타겟팅합니다.

북미의 볶지 않은 시리얼 플레이크 시장은 33%의 점유율을 차지했으며, 2024년에는 39억 달러를 창출했습니다. 이 지역의 성장은 전체 곡물의 이점에 대한 소비자의 광범위한 인식과 성숙한 소매 인프라에 밀려 있습니다. 미국의 라벨링 규제의 갱신과 시설 급식 프로그램에서의 설탕 감축의 의무화는 보다 깨끗한 프로파일을 가지는 시리얼에 유리한 조건을 만들어 내고 있습니다. 캐나다에서는 가공 시리얼 및 스낵바와의 경쟁은 여전히 치열하지만, 프리미엄 상품 선반이 확대되고 인증 프로세스가 보다 이용하기 쉬워지기 때문에 유기농 브랜드가 받아들여지고 있습니다. 브랜드는 소비자의 신뢰를 얻고 경쟁 시장에서 눈에 띄기 위해 지속 가능한 패키징과 검증 가능한 라벨 표시를 강조합니다.

볶지 않은 시리얼 플레이크 시장의 주요 기업은 Nature's Path Foods, Post Consumer Brands, Food For Life Baking, Maselis NV, Nestle(Cereal Partners Worldwide), Small Valley Milling, Bob's Red Mill, PepsiCo/Quaker Oats, Hearthside Food Baking, General Mills, Ritika's Global Grains, Kellogg Company, bio-familia(스위스)입니다. 대기업은 현대의 건강 기준과 식사 규정에 따라 클린 라벨, 유기농, 곡물 시리얼 등 제품 포트폴리오 확대에 주력하고 있습니다. 각 회사는 USDA(미국 농무부)의 유기농 인증을 채택하고 연방 정부의 환불을 활용하여 비용을 상쇄하고 프리미엄 부문에 진입을 가속화하고 있습니다. 많은 기업들은 재생 농업의 주장과 추적성을 지원하기 때문에 공급망 전체의 투명성을 높이고 장기적인 소매 파트너십을 구축하는 데 도움이 됩니다. 각 브랜드는 식이섬유, 단백질, 프로바이오틱스 등의 기능성 성분을 혁신적으로 사용하는 반면 첨가제의 사용을 줄이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

파괴적 혁신

업계에 미치는 영향요인

성장 촉진요인

건강 의식과 전립분 지도가 수요 촉진

갱신된 「헬시」기준, 가공도가 낮은 시리얼 선호

전자상거래와 현대무역이 접근성 확장

유기·재생농업의 확대

함정과 과제

유통기한의 제약이 패키징과 물류의 혁신을 촉진

가공식품과 고급 아침식사 옵션에 의한 경쟁압력

기존의 곡물에 비해 높은 제조 비용

기회

유기인증과 지속가능성의 프리미엄화

명확한 틀 안에서의 기능 강화와 기능성 표시

기능성 식품 강화

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품 형태별

향후 시장 동향

기술 혁신의 전망

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 대해서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 실천

폐기물 감축 전략

생산에 있어서 에너지 효율

환경 친화적인 노력

탄소발자국에의 배려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

파트너십

신제품 발표

확장 계획

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

주요 동향

옥수수 기반 플레이크

밀 기반 플레이크

귀리 기반 플레이크

쌀 기반 플레이크

보리 기반 플레이크

고대 곡물 플레이크

다곡물 혼합 제품

제6장 시장 추계·예측 : 농법별(2021-2034년)

주요 동향

일반 생산 방식

유기농 생산 방식

재생 농업 방식

특수 인증 방식

제7장 시장 추계·예측 : 포장 형태별(2021-2034년)

주요 동향

소비자용 소매 포장

대량/식품비스 포장

산업용 포장

지속가능한 포장

제8장 시장추계·예측 : 용도별(2021-2034년)

주요 동향

즉석 아침 시리얼

핫 시리얼/죽 베이스

식품서비스/대량 용도

산업용/원료 사용

그라놀라/뮤즐리 구성 요소

특수 식용

제9장 시장추계·예측 : 유통 채널별(2021-2034년)

주요 동향

현대 유통

슈퍼마켓

하이퍼마켓

기타

기존 유통

독립계 식료품점

기타

전자상거래

온라인 마켓플레이스(예 : amazon, flipkart)

식료품 배달 앱(예 : bigbasket)

기타

제10장 시장추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제11장 기업 프로파일

Kellogg Company

Nestle(Cereal Partners Worldwide)

General Mills

PepsiCo/Quaker Oats

Post Consumer Brands

Nature's Path Foods

Maselis NV

Bob's Red Mill

bio-familia(Swiss)

King Arthur Baking

Hearthside Food Solutions

Organic Milling

Small Valley Milling

Ritika's Global Grains

Food For Life Baking

KTH

영문 목차

영문목차

The Global Unroasted Cereal Flakes Market was valued at USD 5.5 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 10.7 billion by 2034.

This market's strong growth outlook is supported by a surge in consumer demand for minimally processed, whole-grain breakfast products that align with evolving clean-label and nutrition transparency standards. New FDA regulations have updated the definition of "healthy" to include specific whole-grain minimums while capping added sugars, saturated fats, and sodium, which strongly supports the positioning of unroasted cereal flakes. With global cereal grain output consistently exceeding 3 billion metric tons annually, the industry benefits from stable input supply chains and scalability, allowing producers to prioritize whole grain sourcing and transparency. Consumers are favoring cereals with recognizable, limited ingredients and reduced processing, driven by shifting dietary awareness and updated government nutrition recommendations that emphasize fiber and whole grains. This has led to increased product innovation that includes functional enhancements and nutrient fortification, appealing to health-conscious shoppers seeking both convenience and nutrition. As dietary standards evolve, manufacturers are aligning more closely with health agencies to ensure their offerings meet expectations for cleaner, simpler, and more wholesome food choices.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$5.5 Billion

Forecast Value

$10.7 Billion

CAGR

6.9%

The organic unroasted cereal flakes segment will grow at a CAGR of 8.9% through 2034, propelled by streamlined certification processes and strong links to large-scale cereal production. Regenerative agriculture is also emerging with an 11% CAGR, as brands work with advocacy groups to establish farm-level transition pathways and reliable verification systems. These regenerative claims are gaining traction in specialty retail settings, helping suppliers secure longer-term agreements due to improved input traceability and sustainability documentation.

The ready-to-eat unroasted flakes segment held 60% share and is expected to grow at a CAGR of 6.9% through 2034. These cereals are popular due to their convenience, well-established consumer habits, and continuous product innovations that address evolving preferences. They cater to a busy consumer base looking for nutritious and easy-to-prepare options, often targeting premium segments with clean-label and functional claims aimed at wellness-driven individuals.

North America Unroasted Cereal Flakes Market held a 33% share and generated USD 3.9 billion in 2024. Growth in this region is fueled by broad consumer awareness of whole grain benefits and a mature retail infrastructure. Updated U.S. labeling rules and reduced sugar mandates within institutional meal programs have created favorable conditions for cereals with cleaner profiles. In Canada, while competition from processed cereals and snack bars remains high, organic brands are seeing greater acceptance due to expanded premium shelf space and more accessible certification processes. Brands are placing greater focus on sustainable packaging and verifiable label claims to gain consumer trust and stand out in a competitive market.

Key companies in the Unroasted Cereal Flakes Market are Nature's Path Foods, Post Consumer Brands, Food For Life Baking, Maselis N.V., Nestle (Cereal Partners Worldwide), Small Valley Milling, Bob's Red Mill, PepsiCo/Quaker Oats, Hearthside Food Solutions, Organic Milling, King Arthur Baking, General Mills, Ritika's Global Grains, Kellogg Company, and bio-familia (Swiss). Leading players are focusing on expanding their product portfolios to include clean-label, organic, and whole-grain cereals to align with modern health standards and dietary regulations. Companies are adopting USDA organic certification and leveraging federal reimbursements to offset costs, accelerating entry into premium segments. Many are increasing transparency across their supply chains to support regenerative agriculture claims and traceability, which helps build long-term retail partnerships. Brands are innovative with functional ingredients like fiber, protein, and probiotics while using fewer additives.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Product type trends

2.2.2 Agricultural practice trends

2.2.3 Application trends

2.2.4 Packaging format trends

2.2.5 Distribution channel trends

2.2.6 Regional trends

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Drivers

3.2.1.1 Health awareness and whole-grain guidance elevate demand