우유 단백질 가수분해물 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Milk Protein Hydrolysate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1844362

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

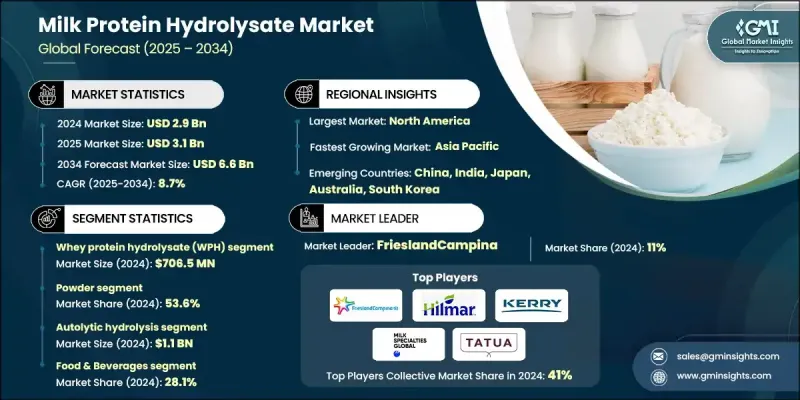

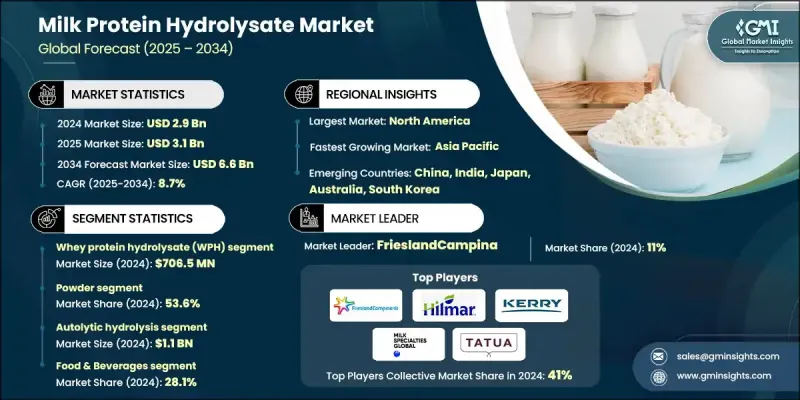

세계의 우유 단백질 가수분해물 시장은 2024년 29억 달러로 평가되었고 CAGR 8.7%로 성장해 2034년까지 66억 달러에 이를 것으로 추정되고 있습니다.

이 성장은 소화성이 높고 낮은 알레르겐 단백질 솔루션에 대한 소비자 수요 증가를 반영합니다. 우유 단백질 가수분해물은 우유 단백질을 더 작은 펩타이드와 아미노산으로 효소 분해하여 생성되어 소화성을 향상시키고 알레르겐 작용을 감소시킵니다. 특히 식품 불내증과 소화 친화적인 영양을 둘러싼 건강 의식의 고조가 시장의 기세에 박차를 가하고 있습니다. 이 제품의 주요 용도로는 우유 알레르기 어린이를 위해 조정된 유아용 준비 분유, 단백질의 신속한 흡수가 필요한 스포츠 보충제, 소화하기 쉬운 단백질 섭취가 필요한 환자를 위해 설계된 의료용 영양제 등이 있습니다. 효소 가수분해 및 여과 방법의 기술 혁신은 일관성, 맛, 영양 공급을 개선했습니다. 이러한 발전으로 생산자는 가수분해의 정도를 세밀하게 제어하고 초기 생활부터 임상 회복 지원에 이르기까지 다양한 요구에 맞게 제품을 조정할 수 있게 되었습니다. 영양과학과 소비자 수요가 진화함에 따라 제조업체는 생산 규모를 확대하고 다기능 변형을 도입하고 있습니다. 근육 회복, 면역 지원, 소화의 용이성 등의 이점을 뒷받침하는 임상 조사는 소비자의 건강 범주 전반에 걸쳐 제품 사용에 대한 신뢰를 계속 증가시키고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

29억 달러

예측 금액

66억 달러

CAGR

8.7%

2024년 유청 단백질 가수분해물 부문의 점유율은 24.5%였습니다. 흡수 속도가 빠르고 알레르기의 가능성을 최소화하고 생물학적 이용능력이 뛰어나 특수 영양 제품에는 빠뜨릴 수 없는 성분이 되고 있습니다. 운동 선수, 건강 지향적인 개인, 치료 식단을 섭취하는 환자는 아미노산의 신속한 공급과 근육 수리 및 건강 유지에 대한 역할에서 유청 단백질 가수분해물에 의존합니다. 이 부문 증가는 측정 가능한 건강 결과와 함께 성과에 중점을 둔 다이어트에 특화된 제품으로의 변화 증가를 반영합니다.

분말 기반 유형은 2024년에 53.6%의 점유율을 차지했습니다. 보존 기간이 길고 비용 효율적인 보관 및 운송이 가능하며 스포츠 영양 및 유아용 조제 분유에서 임상 식품까지 다양한 용도에 적합한 분말 가수분해물은 제조업체와 최종 사용자 모두에게 바람직한 형태가 되고 있습니다. 안정성과 다용도로 세계 시장에서 널리 채택되고 있습니다.

미국의 우유 단백질 가수분해물 시장은 2024년 8억 7,030만 달러를 창출해 북미의 유단백 가수분해물 분야에서 주도적 지위를 강화하였습니다. 확립된 유제품 인프라, 소화기계의 건강에 대한 관심 증가, 식품 과민증을 둘러싼 일반 시민의 의식 증가가 주요 시장 성장 촉진요인입니다. 고령화와 유아 인구의 높은 건강 관리 지출과 기능성 영양에 대한 강한 관심도 가수분해된 우유 단백질 제품에 대한 국가 수요 증가에 기여하고 있습니다.

우유 단백질 가수분해물 세계 시장을 견인하는 주요 기업으로는 Hilmar Ingredients, Arla Foods Ingredients Group, FrieslandCampina, Kerry Ingredients, AMCO Proteins, Glanbia Nutritionals, Havero Hoogwegt, Milk Specialties Global, A. Costantino & C., Agropur Cooperative, Lactalis Group, Armor Proteines, Tatua Co-operative Dairy Company 등이 있습니다. 이 분야의 기업은 생산능력을 확대하고 고도로 특이적이고 기능적인 가수분해물의 변이를 창출하기 위한 연구개발에 투자함으로써 그 지위를 강화하고 있습니다. 임상 영양 브랜드와 스포츠 보충 회사와의 전략적 제휴는 널리 사용되고 있으며, 타겟을 좁힌 제품 배치가 가능해지고 있습니다. FrieslandCampina와 Glanbia Nutritionals와 같은 제조업체는 소비자의 수용성을 높이기 위해 클린 라벨 주장과 풍미 프로파일 개선에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

저알레르기성 영양으로의 이행

클린 라벨 제품 수요

기능성 식품에 통합

유아 및 임상 영양 요구의 확대

업계의 잠재적 위험 및 과제

맛과 기호의 문제

치열한 시장 경쟁

시장 기회

스포츠 영양 수요 증가

개인화된 영양 성장

장의 건강과 면역에 대한 관심 증가

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

지역별

제품별

미래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 관행

폐기물 감축 전략

생산에서의 에너지 효율

환경 친화적인 노력

탄소발자국의 고려

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

주요 동향

유청 단백질 가수분해물(WPH)

카제인 가수분해물(CPH)

총 우유 단백질 가수분해물

락토페린 가수분해물

면역글로불린 가수분해물

α-락토알부민 가수분해물

β-락토글로불린 가수분해물

제6장 시장 추계 및 예측 : 형태별, 2021-2034년

주요 동향

분말

페이스트

제7장 시장 추계 및 예측 : 기술별, 2021-2034년

주요 동향

산 가수분해

효소 가수분해

미생물 발효

자가융해 가수분해

초음파 가수분해

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

주요 동향

식품 및 음료

단백질 보충제

유아 영양

스포츠 영양

베이커리 및 식품 원료

음료

기타

동물사료

가금

육계

산란계

돼지

소

양식업

연어

송어

새우

기타

말

PET

의약품

의약품 제제

임상영양학

기타

화장품 및 퍼스널케어

스킨케어

헤어케어

기타

기타

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 프로파일

Arla Foods Ingredients Group

AMCO Proteins

A. Costantino & C.

Armor Proteines

Agropur Cooperative

FrieslandCampina

Glanbia Nutritionals

Hilmar Ingredients

Havero Hoogwegt

Kerry Ingredients

Lactalis Group

Milk Specialties Global

Tatua Co-operative Dairy Company

Others

JHS

영문 목차

영문목차

The Global Milk Protein Hydrolysate Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 8.7% to reach USD 6.6 billion by 2034.

This growth reflects rising consumer demand for highly digestible and low-allergen protein solutions. Milk protein hydrolysate is created through the enzymatic breakdown of milk proteins into smaller peptides and amino acids, improving digestibility and reducing allergenic effects. Growing health awareness, especially around food intolerances and digestion-friendly nutrition, is fueling market momentum. The product's primary applications include infant formulas tailored for children with milk allergies, sports supplements requiring fast protein absorption, and medical nutrition designed for patients needing easily digestible protein intake. Technological innovations in enzymatic hydrolysis and filtration methods have improved consistency, taste, and nutrient delivery. These advancements allow producers to finely control the degree of hydrolysis and tailor products to different needs-from early life to clinical recovery support. With nutrition science and consumer demand evolving, manufacturers are scaling production and introducing multi-functional variants. Clinical research supporting benefits like muscle recovery, immune support, and ease of digestion continues to build confidence in the product's use across consumer health categories.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.9 Billion

Forecast Value

$6.6 Billion

CAGR

8.7%

The whey protein hydrolysate segment held a 24.5% share in 2024. Its fast absorption rate, minimal allergenic potential, and superior bioavailability have made it an essential ingredient in specialized nutritional products. Athletes, health-conscious individuals, and patients on therapeutic diets rely on whey protein hydrolysate for its quick delivery of amino acids and its role in muscle repair and wellness. This segment's rise reflects the growing shift toward performance-focused and dietary-specific products with measurable health outcomes.

The powder-based formats segment held 53.6% share in 2024. Their long shelf life, cost-effective storage and transport, and compatibility with diverse applications from sports nutrition and infant formulas to clinical foods have made powdered hydrolysates the preferred form for both manufacturers and end-users. Their stability and versatility further enable widespread adoption across global markets.

United States Milk Protein Hydrolysate Market generated USD 870.3 million in 2024, reinforcing its leadership position in North America's milk protein hydrolysate sector. A well-established dairy infrastructure, growing focus on digestive wellness, and heightened public awareness around food sensitivities are key market drivers. High healthcare spending and strong interest in functional nutrition among aging and infant populations also contribute to the country's increasing demand for hydrolyzed milk protein products.

Key players driving the Global Milk Protein Hydrolysate Market include Hilmar Ingredients, Arla Foods Ingredients Group, FrieslandCampina, Kerry Ingredients, AMCO Proteins, Glanbia Nutritionals, Havero Hoogwegt, Milk Specialties Global, A. Costantino & C., Agropur Cooperative, Lactalis Group, Armor Proteines, and Tatua Co-operative Dairy Company. Companies in this space are strengthening their positions by expanding production capacities and investing in R&D to create highly specific and functional hydrolysate variants. Strategic collaborations with clinical nutrition brands and sports supplement companies are becoming common, enabling targeted product placement. Manufacturers like FrieslandCampina and Glanbia Nutritionals focus on clean-label claims and improving flavor profiles to increase consumer acceptance.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Product trends

2.2.2 Form trends

2.2.3 Technology trends

2.2.4 End Use trends

2.2.5 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Shift to hypoallergenic nutrition

3.2.1.2 Demand for clean-label products

3.2.1.3 Integration into functional foods

3.2.1.4 Expansion of infant and clinical nutrition needs

3.2.2 Industry pitfalls and challenges

3.2.2.1 Flavor and palatability issues

3.2.2.2 Intense market competition

3.2.3 Market opportunities

3.2.3.1 Rising demand in sports nutrition

3.2.3.2 Growth in personalized nutrition

3.2.3.3 Rising interest in gut health and immunity

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product

3.9 Future market trends

3.10 Technology and innovation landscape

3.10.1 Current technological trends

3.10.2 Emerging technologies

3.11 Patent landscape

3.12 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.12.1 Major importing countries

3.12.2 Major exporting countries

3.13 Sustainability and environmental aspects

3.13.1 Sustainable practices

3.13.2 Waste reduction strategies

3.13.3 Energy efficiency in production

3.13.4 Eco-friendly initiatives

3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Whey protein hydrolysate (WPH)

5.3 Casein hydrolysate (CPH)

5.4 Total milk protein hydrolysate

5.5 Lactoferrin hydrolysate

5.6 Immunoglobulin hydrolysate

5.7 Alpha-lactalbumin hydrolysate

5.8 Beta-lactoglobulin hydrolysate

Chapter 6 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Powder

6.3 Paste

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Acid hydrolysis

7.3 Enzymatic hydrolysis

7.4 Microbial fermentation

7.5 Autolytic hydrolysis

7.6 Ultrasonic hydrolysis

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

8.1 Key trends

8.2 Food & beverages

8.2.1 Protein supplement

8.2.2 Infant nutrition

8.2.3 Sports nutrition

8.2.4 Bakery & food ingredients

8.2.5 Beverages

8.2.6 Others

8.3 Animal feed

8.3.1 Poultry

8.3.1.1 Broilers

8.3.1.2 Layers

8.3.2 Swine

8.3.3 Cattle

8.3.4 Aquaculture

8.3.4.1 Salmon

8.3.4.2 Trouts

8.3.4.3 Shrimps

8.3.4.4 Others

8.3.5 Equine

8.3.6 Pet

8.4 Pharmaceutical

8.4.1 Pharmaceutical formulations

8.4.2 Clinical nutrition

8.4.3 Others

8.5 Cosmetics & Personal Care

8.5.1 Skincare

8.5.2 Haircare

8.5.3 Others

8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)