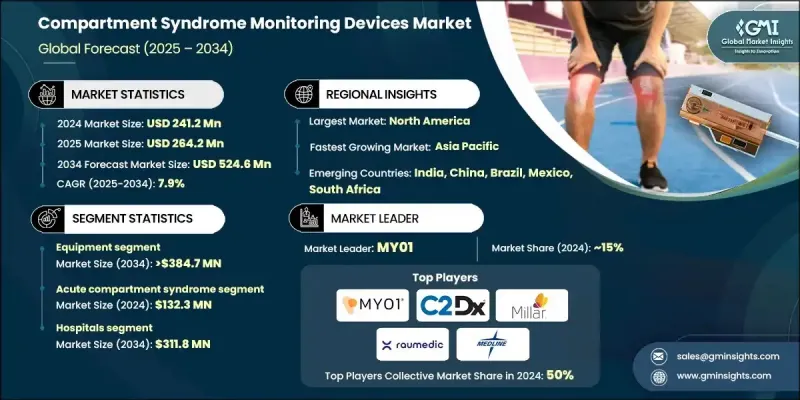

세계의 구획증후군 모니터링 기기 시장은 2024년 2억 4,120만 달러로 평가되었고 CAGR 7.9%로 성장하여 2034년까지 5억 2,460만 달러에 이를 것으로 예측되고 있습니다.

이러한 견고한 성장의 배경으로는 외상과 관련된 사례 증가, 조기 및 정확한 진단 필요성 증가, 압력 모니터링 시스템의 기술적 혁신, 건강 관리 인프라 확대 등이 있습니다. 구획증후군 모니터링 기기는 근육의 구획압을 측정하도록 설계되었으며 임상의가 급성 및 만성 증상을 발견하는 데 도움이 됩니다. 이 장비는 근육 구획 내의 혈류 제한으로 인한 돌이킬 수 없는 조직 손상을 예방하는 데 매우 중요합니다. 진단 정밀도의 향상이나 사용하기 쉬운 기기 설계와 함께 의료 관계자의 의식의 고조가 시장 확대에 기여하고 있습니다. 기존의 침습적인 방법에서 스마트하고 저침습적인 모니터링 시스템으로의 전환은 외상 치료 및 수술 현장에서 장비 채용을 촉진하는 데 중요한 역할을 합니다. 제조업체의 R&D 투자 증가는 소형, 무선 및 연속 모니터링 기술의 전개를 가능하게 하여 환자의 안전성과 임상 정확도 향상을 보장합니다. 신속한 진단과 환자별 치료 프로토콜이 중요해짐에 따라, 신뢰할 수 있는 모니터링 장비에 대한 수요는 세계의 의료 시스템 전반에 걸쳐 가속화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 2억 4,120만 달러 |

| 예측 금액 | 5억 2,460만 달러 |

| CAGR | 7.9% |

2024년 장비 부문의 점유율은 74.4%로 선진적인 병원 모니터링 시스템의 채용이 증가하고 지속적인 사용을 지원하는 일회용 키트에 대한 수요가 높아지고 있는 것이 배경에 있습니다. 의료시설은 임상 오류를 줄이고 환자의 결과를 개선하기 위해 일관되고 정확한 루멘 압력 측정을 제공하는 장비에 주목하고 있습니다. 의료 종사자들은 신뢰할 수 있는 측정을 제공하고 중요한 의사결정을 지원하는 능력으로 인해 수동 도구보다 전용 모니터링 시스템을 점점 더 선호합니다.

2024년에는 복부 구획증후군이 큰 점유율을 차지하고 2034년까지 연평균 복합 성장률(CAGR) 8.5%를 보일 것으로 예측됩니다. 외상 사례 증가, 수술 후 합병증의 발생 증가, ICU 입실 증가가 복강 내압 모니터링 솔루션 수요 증가에 기여하고 있습니다. 진단 지연의 위험성에 대한 인식이 높아짐에 따라 임상의사는 복압 상승을 조기에 감지하고 적시 개입을 유도할 수 있는 고급 모니터링 시스템에 대한 의존도를 높이고 있습니다. 이와 같이 조기 발견과 임상 효율이 중시되게 된 것이 이 부문의 성장을 뒷받침하고 있습니다.

북미 구획증후군 모니터링 기기 시장은 2024년 55.7%의 점유율을 차지했습니다. 이 지역의 우위성은 선도적인 제조업체의 존재감의 강도, 신기술의 급속한 채용, 견고한 유통망에 기인합니다. 고급 의료시설의 가용성, 외상 및 중증 환자에 대한 일관된 투자는 이 지역의 성장을 계속 지원합니다.

세계 구획증후군 모니터링 기기 시장에서 활약하는 주요 기업은 C2DX, Accuryn, Spiegelberg, RAUMEDIC, Sentinel Medical Technologies, Millar, Biometrix, MY01, Medline, DELTAMED, ConvaTec 등이 있습니다. 구획증후군 모니터링 기기 시장의 주요 기업은 차세대 모니터링 시스템을 출시하기 위해 지속적인 R&D 혁신을 우선시하고 있습니다. 많은 기업들은 실시간 데이터를 제공하고 조작성을 향상시킨 무선으로 낮은 침습 장비를 도입하고 있습니다. 시장 경쟁력을 유지하기 위해 제조업체는 병원, 외상 센터 및 의료 유통업체와의 전략적 제휴를 통해 프레즌스를 확대하고 있습니다. 또한 신흥 시장에서 장비의 저가격화와 접근성 향상을 도모하는 기업도 있습니다. 규제 당국의 승인, 임상시험 검증, 데이터 추적 및 연결성과 같은 디지털 건강 기능의 통합에 중점을 둔 노력은 시장 포지셔닝을 강화하는 데 도움이 됩니다. 게다가 기업은 마케팅 캠페인이나 의료 교육에 투자해 조기 발견 및 조기 진단에 대한 의식을 높이는 것으로, 시장에 대한 침투를 도모해, 헬스 케어 프로바이더의 채용률을 높이고 있습니다.

The Global Compartment Syndrome Monitoring Devices Market was valued at USD 241.2 million in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 524.6 million by 2034.

This robust growth is fueled by rising cases of trauma-related injuries, a growing push for early and accurate diagnosis, technological breakthroughs in pressure monitoring systems, and expanding healthcare infrastructure. Compartment syndrome monitoring devices are designed to measure intracompartmental pressure in muscles, helping clinicians detect both acute and chronic forms of the condition. These devices are crucial in preventing irreversible tissue damage caused by restricted blood flow within muscle compartments. Increasing awareness among medical professionals, coupled with improvements in diagnostic precision and user-friendly device design, is contributing to market expansion. The shift from traditional invasive methods to smart, minimally invasive monitoring systems also plays a significant role in driving device adoption across trauma care and surgical settings. Rising investment in R&D by manufacturers is further enabling the rollout of compact, wireless, and continuous monitoring technologies, ensuring better patient safety and clinical accuracy. With growing emphasis on faster diagnosis and patient-specific treatment protocols, the demand for reliable monitoring devices is accelerating across global healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $241.2 Million |

| Forecast Value | $524.6 Million |

| CAGR | 7.9% |

The equipment segment accounted for 74.4% share in 2024, driven by rising adoption of advanced hospital monitoring systems and increasing demand for disposable kits that support ongoing use. Healthcare facilities focus on equipment that offers consistent and accurate intracompartmental pressure measurement to reduce clinical errors and improve patient outcomes. Medical professionals increasingly prefer dedicated monitoring systems over manual tools for their ability to deliver reliable readings and support critical decision-making.

In 2024, the abdominal compartment syndrome accounted for a significant share and is projected to grow at a CAGR of 8.5% through 2034. An uptick in trauma cases, increased occurrence of post-surgical complications, and growing ICU admissions are contributing to higher demand for intra-abdominal pressure monitoring solutions. As awareness rises around the dangers of delayed diagnosis, clinicians are relying more heavily on advanced monitoring systems that can detect elevated pressure early and help guide timely intervention. This increasing focus on early detection and clinical efficiency is pushing the segment's growth.

North America Compartment Syndrome Monitoring Devices Market held a 55.7% share in 2024. The region's dominance can be attributed to the strong presence of major manufacturers, rapid adoption of new technologies, and robust distribution networks. The availability of advanced healthcare facilities, along with consistent investment in trauma and critical care services, continues to support regional growth.

Some of the key companies active in the Global Compartment Syndrome Monitoring Devices Market include C2DX, Accuryn, Spiegelberg, RAUMEDIC, Sentinel Medical Technologies, Millar, Biometrix, MY01, Medline, DELTAMED, and ConvaTec. Leading companies in the compartment syndrome monitoring devices market are prioritizing innovation through continuous R&D to launch next-generation monitoring systems. Many are introducing wireless and minimally invasive devices that offer real-time data and improved usability. To maintain market competitiveness, manufacturers are expanding their global presence through strategic partnerships with hospitals, trauma centers, and medical distributors. Some firms are also enhancing device affordability and increasing access in emerging markets. Focused efforts on regulatory approvals, clinical trial validation, and integrating digital health features like data tracking and connectivity are helping strengthen market positioning. Moreover, firms are investing in marketing campaigns and medical education to raise awareness about early detection and diagnosis, ensuring deeper market penetration and higher adoption rates among healthcare providers.